|

|

Post by jeffolie on Oct 30, 2012 17:11:30 GMT -6

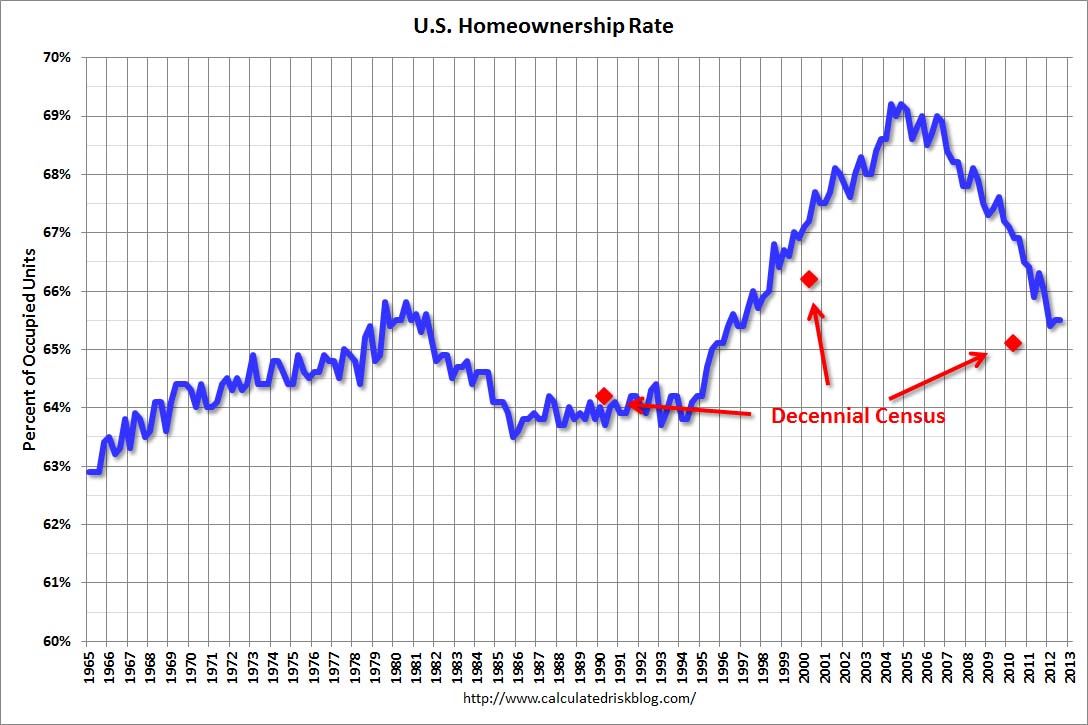

rental vacancy rate lowest level since 2001, Ownership rate bottom not reached yet matching 1990s " ... does suggest that the housing vacancy rates have declined sharply. my jeffolie view: renting demand rose, ownership demand fell as fewer marry and the birthrate trend declined mostly due to economic stress complicated with cultural shifts similar to Japan's long shift as well as in the EU. The coming 2016 economic and financial bottom will drop the Home Ownership rate down to the 1990s level along with lower Single Family Home prices. ==============================  4.bp.blogspot.com/-W-BmJkDYG_M/UJBDJyP-UGI/AAAAAAAAUKk/_UQbWdbWcAg/s1600/RentalVacancyQ32012.jpg 4.bp.blogspot.com/-W-BmJkDYG_M/UJBDJyP-UGI/AAAAAAAAUKk/_UQbWdbWcAg/s1600/RentalVacancyQ32012.jpgThe rental vacancy rate was unchanged from Q2 at 8.6%, and down from 9.8% in Q3 2011. I think the Reis quarterly survey (large apartment owners only in selected cities) is a much better measure of the overall trend in the rental vacancy rate - and Reis reported that the rental vacancy rate has fallen to the lowest level since 2001. The quarterly HVS is the most timely survey on households, but there are many questions about the accuracy of this survey. Unfortunately many analysts still use this survey to estimate the excess vacant supply. However this does suggest that the housing vacancy rates have declined sharply. Read more at www.calculatedriskblog.com/#COcP2Z5jQMesGKRV.99 ==========================  2.bp.blogspot.com/-i8Sc_WHrp1Y/UJBDIaLisAI/AAAAAAAAUKM/_o3NAJyJTuo/s1600/HomeownershipQ32012.jpg 2.bp.blogspot.com/-i8Sc_WHrp1Y/UJBDIaLisAI/AAAAAAAAUKM/_o3NAJyJTuo/s1600/HomeownershipQ32012.jpg" ... The Red dots are the decennial Census homeownership rates for April 1st 1990, 2000 and 2010. The HVS homeownership rate was unchanged from Q2 at 65.5%, and down from 66.3% in Q3 2011. I'd put more weight on the decennial Census numbers and that suggests the actual homeownership rate is probably in the 64% to 65% range. Read more at www.calculatedriskblog.com/#COcP2Z5jQMesGKRV.99 |

|

|

|

Post by jeffolie on Jan 8, 2013 12:00:09 GMT -6

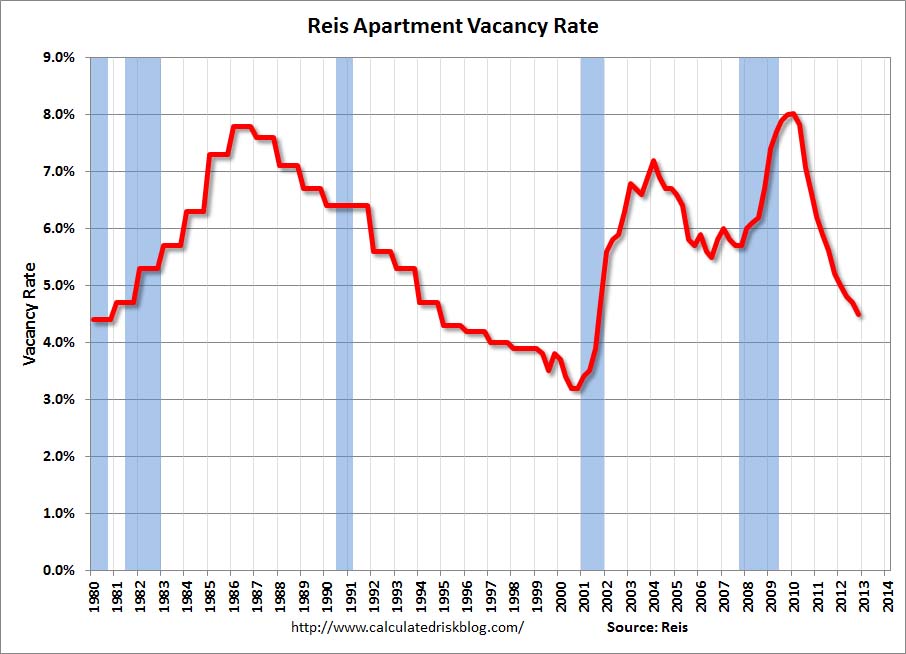

4.bp.blogspot.com/-4sZ0B-7uLGU/UOwdM1RerPI/AAAAAAAAXao/MAGW05mo3Vw/s1600/ReisApartmentQ42012.jpg 4.bp.blogspot.com/-4sZ0B-7uLGU/UOwdM1RerPI/AAAAAAAAXao/MAGW05mo3Vw/s1600/ReisApartmentQ42012.jpgJanuary 08, 2013 Reis: Apartment Vacancy Rate declined to 4.5% in Q4 by Bill McBride on 1/08/2013 Reis reported that the apartment vacancy rate fell to 4.5% in Q4, down from 4.7% in Q3 2012. The vacancy rate was at 5.2% in Q4 2011 and peaked at 8.0% at the end of 2009. Some data and comments from Reis Senior Economist Ryan Severino: Vacancy declined by another 20 bps during the fourth quarter to 4.5%. This exceeded performance during the third quarter when vacancy declined by 10 bps. On a year-over-year basis, the vacancy rate declined by 70 bps. There was a bit of a resurgence in demand for apartment units during the fourth quarter when 45,162 units were absorbed. This represents an increase versus the 24,951 units that were absorbed during the third quarter but a slight decrease versus the 47,396 units that were absorbed during the fourth quarter of 2011. Net absorption has been consistently positive since the second quarter of 2009. For the calendar year 2012, 138,155 units were absorbed. This is a decline from the 172,707 units that were absorbed during calendar year 2011.This decline is not surprising. The market has tightened considerably over the last few years and at this point in the cycle a slight slowing should be anticipated. New construction also increased during the quarter. 24,614 units were delivered during the fourth quarter, versus 17,378 units during the third quarter. This is also an increase compared to the 10,145 units that were delivered during the fourth quarter of 2011. This is the third consecutive quarter of construction increases and the highest level of quarterly completions since the second quarter of 2010. For calendar year 2012, 66,846 units were completed. This is an increase versus the 42,290 that were completed during 2011. Asking and effective rents both grew by 0.6% during the fourth quarter. This was below the third quarter performance when asking and effective rents grew by 0.8% and 0.9%, respectively. Both asking and effective rents have consistently increased since the first quarter of 2010. However, this was the weakest performance since the fourth quarter of 2011. Nonetheless, taking a longer©\term view, on a year©\over©\year basis rent growth continues to accelerate. Nationally, asking and effective rents hit another all©\time high during the fourth quarter, propelled by strong demand, limited new supply growth, and a still weak for©\sale housing market. ... The outlook for 2013 remains stout. Although new completions are expected to accelerate substantially during 2013, demand should remain tight. With demand outpacing new completions, vacancy is expected to continue to decrease, but the rate of decline will slow as the market digests all of the new units coming online. However, given that tightness in the market will persist, rent growth will continue to accelerate ¨C having shorn concessions landlords now feel empowered to raise face©\level asking rents in a more pronounced fashion. The majority of the market will continue to perform well in 2013 as their tenants will have no choice but to continue paying record©\level rents. The greatest risk likely resides in the highest©\quality properties with the most expensive rents, typically class A and above properties. Rents in these high©\quality properties are prohibitively expensive and tenants have already countenanced large annual rent increases. With housing prices remaining relatively low and mortgage rates hovering near record©\low levels, an increasing number of these class A/A+ tenants, who boast high incomes, ample savings, and good credit ratings, will do the math and decide that it is finally time to purchase a home. Click on graph for larger image. This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Reis is just for large cities. This was another strong quarter for apartments with the vacancy rate falling and rents rising. With more supply coming online in 2013, the decline in the vacancy rate should slow - but the market is still tight, and Reis expects rents to continue to increase. www.calculatedriskblog.com/2013/01/reis-apartment-vacancy-rate-declined-to.html |

|

|

|

Post by unlawflcombatnt on Jan 8, 2013 13:03:48 GMT -6

|

|

|

|

Post by jeffolie on Jan 8, 2013 13:20:19 GMT -6

I agree ... Blackrock Group, et al buys and rehab huge quantities of low end houses to flip or sell as investment vehicles to get rental income above the near zero yields on 'safe' investments...essentially increasing single family houses as a category of rentals rather than owner-occupied |

|

|

|

Post by unlawflcombatnt on Jan 9, 2013 1:02:06 GMT -6

I agree ... Blackrock Group, et al buys and rehab huge quantities of low end houses to flip or sell as investment vehicles to get rental income above the near zero yields on 'safe' investments...essentially increasing single family houses as a category of rentals rather than owner-occupied So this mean that the there are even less "owner-occupied" homes than previously. Homes have ceased to be primarily a place of residence, and have instead become primarily a revenue stream for Wall Street. And all this with the help of Bernanke, Obama, Geithner, and their ilk, who've bent over backwards to save banks at the expense of everyone else. Homes have not become more affordable. Rather, home ownership has become more profitable for those who can afford to own them. |

|

|

|

Post by jeffolie on Apr 3, 2013 17:00:40 GMT -6

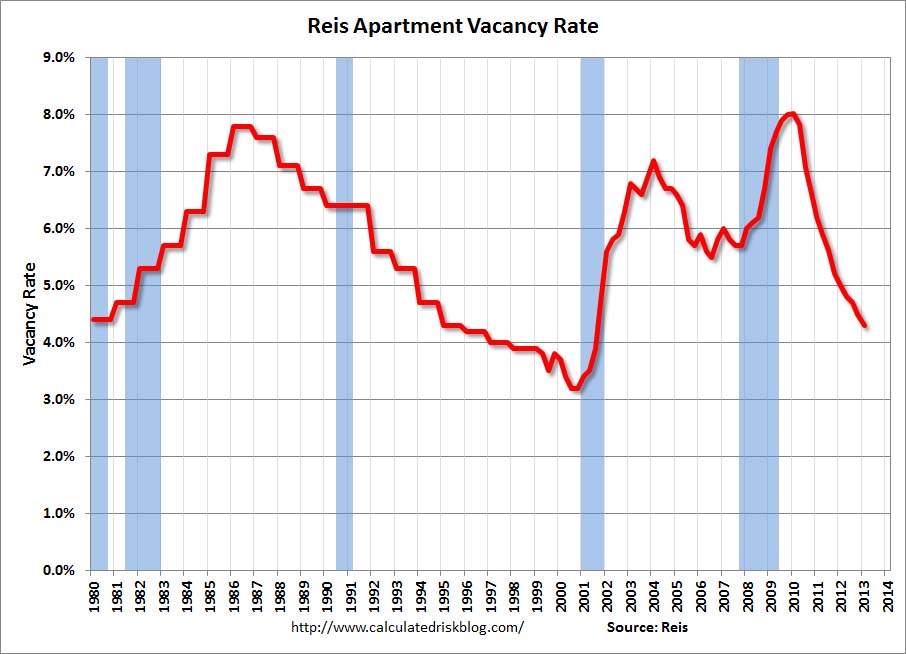

3.bp.blogspot.com/-sgjm4STrv64/UVxYUUCtHwI/AAAAAAAAZr8/3UZIF6I91IE/s1600/ReisApartQ12013.jpg 3.bp.blogspot.com/-sgjm4STrv64/UVxYUUCtHwI/AAAAAAAAZr8/3UZIF6I91IE/s1600/ReisApartQ12013.jpgReis: Apartment Vacancy Rate declined to 4.3% in Q1 2013 by Bill McBride on 4/03/2013 Reis reported that the apartment vacancy rate fell to 4.3% in Q1, down from 4.5% in Q4 2012. The vacancy rate was at 5.0% in Q1 2012 and peaked at 8.0% at the end of 2009. Some data and comments from Reis VP of Research Victor Calanog: Vacancy fell by 20 basis points in the first quarter, dipping to 4.3%. Over the last four quarters, national vacancies have declined by 70 basis points, a far faster pace than any other sector in commercial real estate. The vacancy rate has now fallen by 370 basis points since the cyclical peak of 8.0% observed right after the recession winded down in late 2009. By contrast, office sector vacancies have only fallen by a paltry 60 basis points since fundamentals began recovering five quarters ago. The sector absorbed over 36,000 units in the first quarter, a relatively healthy rate comparable to the rise in occupied stock from one year ago (in 2012Q1). Deliveries have remained modest at 13,706 units, representing roughly the same pace of inventory growth as previous first quarter periods over the last two years. Apartment landlords have another quarter or two to enjoy tight supply growth before a large number of new properties come online. Over 100,000 units are expected to enter the market, most scheduled to open their doors in the latter half of the year. With home prices recovering and mortgage rates staying low, it remains to be seen whether demand for apartments will continue to push vacancies down once inventory growth ramps up. Asking and effective rents both grew by 0.5% during the first quarter. This is the slowest rate of growth for both asking and effective rents since the fourth quarter of 2011; every single quarterly data point in 2012 showed stronger asking and effective rent growth versus what was observed in the current quarter. What does this mean? Optimists will point out that the first quarter tends to be weak, as most households move during the second and third quarters and bolster leasing activity and rent increases. The seasonal waxing and waning in rent growth was evident in the prior year, when the strongest periods centered around the second and third quarters. However, given how tight vacancies have become, rent growth ought to be stronger (for perspective, in prior periods when vacancies were in the low to mid]4s, annual rent growth was well above 4%). Analysts have wondered how rents could keep climbing when jobs are being created at a sluggish rate and wage growth has been relatively stagnant: all of Reis's major markets now boast rent levels well beyond peaks achieved prior to the recession. One answer is that the moribund housing market left households with little choice but to absorb rent hikes, but with the housing market now recovering, does that mean the tide is turning against landlords? The next few quarters will test the robustness of apartment fundamentals in the face of rising supply growth and rent levels that may have climbed to unsustainable levels. Click on graph for larger image. This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Reis is just for large cities. This was another strong quarter for apartments with the vacancy rate falling and rents rising. With more supply coming online later this year, the decline in the vacancy rate should slow www.calculatedriskblog.com/2013/04/reis-apartment-vacancy-rate-declined-to.html |

|

|

|

Post by jeffolie on Jul 30, 2013 12:30:58 GMT -6

|

|

|

|

Post by jeffolie on Oct 1, 2013 7:33:01 GMT -6

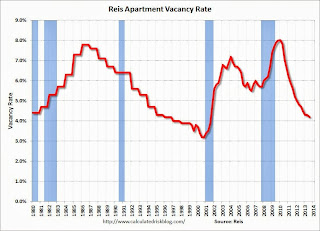

New American Dream renting unmarrieds, not buying my jeffolie view: New American Dream features twenty somethings saving in order to move out from their parents home into renting from Blackstone's newly converted into rentals ... the American Dream of home ownership died ... the American family now are a majority not married and are unmarried ... rental demand rises and vacancy rate declines with the new normal, the new New American Dream renting unmarrieds, not buying ============================================================== October 01, 2013 Reis: Apartment Vacancy Rate declined to 4.2% in Q3 2013 by Bill McBride on 10/01/2013 Reis reported that the apartment vacancy rate declined in Q3 to 4.2% from 4.3% in Q2. In Q3 2012 (a year ago) the vacancy rate was at 4.7%, and the rate peaked at 8.0% at the end of 2009. Some data and comments from Reis Senior Economist Ryan Severino: Vacancy declined by 10 basis points during third quarter to 4.2%. Although vacancy compression has clearly slowed over the last few years, the decline of 10 basis points is an improvement versus last quarter when vacancy was unchanged. Over the last four quarters national vacancies have declined by 50 basis points, on par with last quarter's year‐over‐year decline in vacancy. More so than the magnitude of the vacancy compression, the simple fact that vacancy continues to compress despite such low vacancy rates speaks volumes about the ongoing demand for apartments. The national vacancy rate now stands 380 basis points below the cyclical peak of 8.0% observed right after the recession concluded in late 2009.

Almost four years removed from the advent of the apartment market recovery, demand for apartment units remains robust. The sector absorbed 40,392 units in the third quarter, well outpacing absorption from one year ago during 3Q2012 and up from the 33,634 units that were absorbed during the second quarter of 2013. Year to date, the sector has absorbed more units in 2013 than were absorbed through this point in 2012, but is well below the pace of net absorption during the early stages of the recovery in 2010 and 2011. Conversely, construction activity continues to increase. Completions during the third quarter were 34,834 units, an increase relative to last quarter's 28,891 units and the 21,237 units that were delivered during the third quarter of 2012. This is the highest level of quarterly completions since the fourth quarter of 2009. As we mentioned last quarter, it appears as if we are on the precipice of the relatively large surge in new supply that the market has been anticipating (though not seeing) for the last few years. ... Nonetheless, despite the increase in construction activity, robust demand continues to outpace new completions, intimating that most new units are being rapidly absorbed.

Asking and effective rents both by 0.9% and 1.0%, respectively, during the third quarter. ... Accelerating supply growth is not yet much of a factor in restraining rent growth, but that could change as construction activity surges over the next year. Nevertheless, even with tepid rent growth during the recovery period, national asking and effective rents once again reached all‐time high levels, at least on a nominal basis.

...

Despite supply growth accelerating, we do not expect there to be much change in the national vacancy rate during the fourth quarter due to continued strong demand. However, we anticipate that vacancy will slowly drift upward beginning in 2014, eventually reaching 4.9% by the end of 2017. This primarily should be a function of increased construction activity, not a fall off in demand, which should remain fairly robust.

Apartment Vacancy Rate  This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Reis is just for large cities. New supply is finally coming on the market and the decline in the vacancy rate has slowed. Apartment vacancy data courtesy of Reis. www.calculatedriskblog.com/ |

|