|

|

Post by jeffolie on Jun 7, 2013 11:24:34 GMT -6

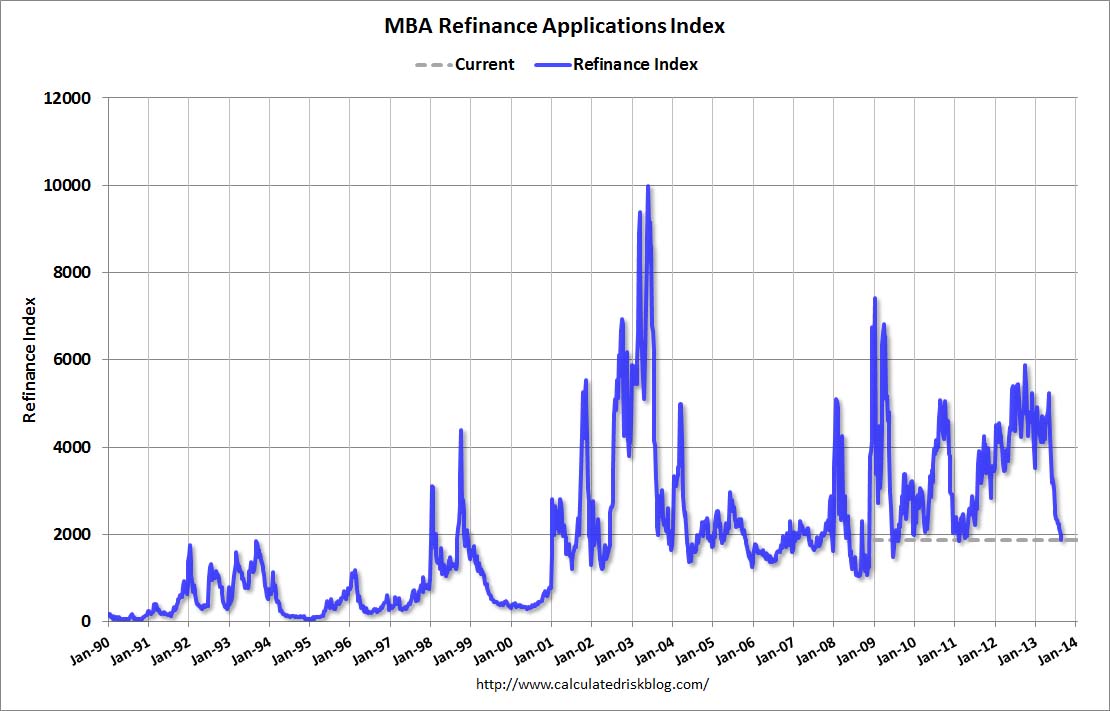

Destroying refinance spending, higher rates June 2013 " ... The refinancing index is down four straight weeks, and was down 12% the previous week. Refinance applications tends to be more sensitive to a rise in mortgage rates .... The MBA 30-year fixed mortgage rate climbed from 3.59% in the first week of May to 4.07% in the first week of June.

my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits]

===============================================

2013-06-07 — seattlepi.com

``This morning's MBA purchase applications showed that refinance index was down 15% for the May 31st week. The refinancing index is down four straight weeks, and was down 12% the previous week. Refinance applications tends to be more sensitive to a rise in mortgage rates.''

Refinance applications tends to be more sensitive to a rise in mortgage rates.

The MBA 30-year fixed mortgage rate climbed from 3.59% in the first week of May to 4.07% in the first week of June. The decline in refinance activity reflects the rise in mortgage rates, Ed Stansfield, chief housing economist at Capital Economics explained in an email interview.

There are three key reasons to watch this data.

First, despite the recent sharp rise, mortgage rates are still at low levels. So the impact on refinance activity shows that both the housing market and overall economic confidence are still "fragile" and the the recovery is dependent on the loose monetary policy.

Second, is the impact on consumer spending, which Stansfield doesn't think will be "large."

Third, for those with adjustable rate mortgages (ARM) the rising interest rates have been a bigger blow. "This could offset some of the benefits of falling unemployment on delinquency rates, though again I would not really expect this effect to be large based on the rise in mortgage rates seen so far."

But how significant is it?

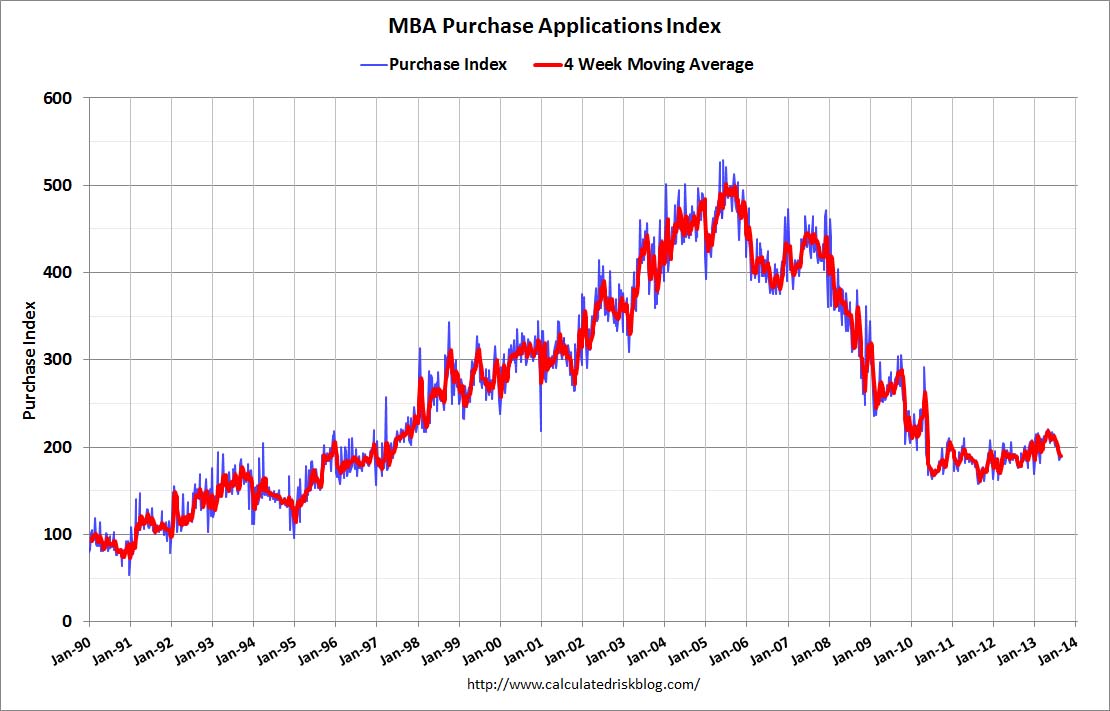

"In terms of its significance, in my view, it is less of a concern than if home purchase approvals had fallen to a similar degree – they have been softening too, but not by as much," Stansfield said. "After all, home purchase approvals are a better gauge of the strength of the demand for housing than the number of people who are switching from one mortgage deal to another."

Bottomline: Stansfield expects the housing market to continue to recover but says this data shows that the recovery "may not proceed in a straight line."

www.seattlepi.com/technology/businessinsider/article/Mortgage-Refinance-Applications-Are-Crumbling-4583847.php |

|

|

|

Post by jeffolie on Jun 10, 2013 7:49:07 GMT -6

Destroying refinance spending, higher rates June 2013 " ... The refinancing index is down four straight weeks, and was down 12% the previous week. Refinance applications tends to be more sensitive to a rise in mortgage rates .... The MBA 30-year fixed mortgage rate climbed from 3.59% in the first week of May to 4.07% in the first week of June.

my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits]

===============================================

June 10, 2013 ... at the morning opening the rates are higher10-Year Bond 2.2% +0.133 +6.51%my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits] ======================================================= June 10, 2013 Q1 2013: Mortgage Equity Withdrawal Strongly Negative by Bill McBride on 6/10/2013 Note: This is not Mortgage Equity Withdrawal (MEW) data from the Fed. The last MEW data from Fed economist Dr. Kennedy was for Q4 2008. The following data is calculated from the Fed's Flow of Funds data and the BEA supplement data on single family structure investment. This is an aggregate number, and is a combination of homeowners extracting equity - hence the name "MEW", but there is little MEW right now - and normal principal payments and debt cancellation. For Q1 2013, the Net Equity Extraction was minus $85 billion, or a negative 2.8% of Disposable Personal Income (DPI).  1.bp.blogspot.com/-CZKfTlG5_6Q/UbXUavlc2GI/AAAAAAAAapI/vPRAAGqSNQ0/s1600/MEWQ12013.jpg 1.bp.blogspot.com/-CZKfTlG5_6Q/UbXUavlc2GI/AAAAAAAAapI/vPRAAGqSNQ0/s1600/MEWQ12013.jpgThis graph shows the net equity extraction, or mortgage equity withdrawal (MEW), results, using the Flow of Funds (and BEA data) compared to the Kennedy-Greenspan method. There are smaller seasonal swings right now, perhaps because there is a little actual MEW (this is heavily impacted by debt cancellation right now). The Fed's Flow of Funds report showed that the amount of mortgage debt outstanding declined further in Q1. Mortgage debt has declined by almost $1.3 trillion since the peak. This decline is mostly because of debt cancellation per foreclosures and short sales, and some from modifications. There has also been some reduction in mortgage debt as homeowners paid down their mortgages so they could refinance. With residential investment increasing, and a slower rate of debt cancellation, it is possible that MEW will turn positive again in the next year or two. www.calculatedriskblog.com/2013/06/q1-2013-mortgage-equity-withdrawal.html |

|

|

|

Post by jeffolie on Jun 10, 2013 10:35:03 GMT -6

Destroying refinance spending, higher rates June 2013 " ... The refinancing index is down four straight weeks, and was down 12% the previous week. Refinance applications tends to be more sensitive to a rise in mortgage rates .... The MBA 30-year fixed mortgage rate climbed from 3.59% in the first week of May to 4.07% in the first week of June.

my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits]

===============================================

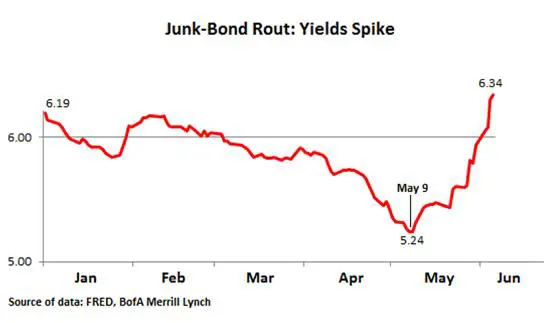

June 10, 2013 ... at the morning opening the rates are higher10-Year Bond 2.2% +0.133 +6.51%my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits] ======================================================= June 10, 2013 Q1 2013: Mortgage Equity Withdrawal Strongly Negative .... minus $85 billion, or a negative 2.8% of Disposable Personal Income (DPI). 1.bp.blogspot.com/-CZKfTlG5_6Q/UbXUavlc2GI/AAAAAAAAapI/vPRAAGqSNQ0/s1600/MEWQ12013.jpg10 Year T-Note Yield 2.222% +0.61 Monday June 10, 2013, 12:24 my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits] ======================================================================= The Number That Matters by John Rubino on June 10, 2013 Friday was one of those days when so many markets move so dramatically that it’s hard to know what to focus on. But in this case the headline numbers – US stocks way up, gold way down, foreign markets all over the place — matter less than the interest rate on 10-year Treasuries, which spiked:  dollarcollapse.com/wp-content/uploads/2013/06/10-year-treasury-june-13.jpg dollarcollapse.com/wp-content/uploads/2013/06/10-year-treasury-june-13.jpgThe reason this number matters is that a return to “normal” times of high employment and fast growth also means a return to normal interest rates, which would be about twice current levels. This creates one or two little problems for a society with trillions of dollars of debt to roll over each year. Already, with the 10-year moving just from 1.7% to 2.2%, the junk bond market is suffering: The Day The Big Fat Junk-Bond Bubble Blew Up My friends in the corporate restructuring industry aren’t breaking out the bubbly just yet. But with one eye, they’re gazing wistfully into the distant horizon where they’re seeing the first signs of a glimmer of hope. And with the other eye, they’re gazing at the screens of their smartphones and computers where they’re seeing brutal junk bond rout. Junk bonds had a phenomenal run. With each truckload of free money that the Fed and other central banks delivered to the markets, junk-bond valuations soared and yields plunged. The St. Louis Fed’s BofA Merrill Lynch junk-bond yield index, which was deep into the double digits during the financial crisis, hit a low on May 9 of 5.24%, down from 6.19% at the start of the year. Yields on some of the least bad junk in the index were well below 5%. Before these crazy times that the financial crisis brought, you could buy an essentially risk-free 1-year FDIC-insured CD with an interest rate of 5%. But recently, desperate investors, mauled by the Fed’s zero-interest-rate policy and losing ground to inflation, were furiously grabbing yield wherever they could, taking on risks no questions asked, any risks no matter how large, to get to that 5% yield. A feeding frenzy for junk. Companies took advantage of this Fed-induced desperation and bamboozled investors into gobbling up $187 billion in junk bonds so far in 2013, a record! One of the losers of the Fed’s policies was the corporate restructuring industry. With endless amounts of nearly free money available, even teetering companies with too much debt and money-losing operations could borrow more to cover up any holes. So my friends and their restructuring outfits branched out into performance-improvement consulting and financial advisory, and some have left the business altogether. Bubbles balloon to an absurd magnitude. But one day the feeding frenzy dies down, and gradually, or sometimes suddenly, the risks, the silliness, the illogic, the whole nonsensical nature of the bubble move into the foreground for all to see, and more and more people open their eyes and see it. Some of them will try to get out somehow, quietly at first, by looking for the greater fool. And there are plenty of them, for a while. But new investors want to be compensated for the risks they’re now seeing, and they’ll demand higher yields in return for taking on those risks. That day might have been May 9 – when the air started hissing out of the junk bond bubble. What came afterward was a rout. And a spike in yields:  dollarcollapse.com/wp-content/uploads/2013/06/Junk-bonds-June-13.jpg dollarcollapse.com/wp-content/uploads/2013/06/Junk-bonds-June-13.jpgAnd mortgage refinancing is drying up: Refinancing Activity Continues to Shrink as Rates Jump to Recent Highs There was another substantial drop in mortgage applications during the week ended May 31 as rates increased, in some cases to 13 month highs. The Mortgage Bankers Association (MBA) said results of its Weekly Mortgage Applications Survey showed an 11.5 percent decrease in its Market Composite Index, a measure of mortgage volume, on a seasonally adjusted basis from the week ended May 24. The Composite was down 20 percent on a non seasonally adjusted basis. Rates for the conforming 30-year fixed-rate mortgage (FRM) had the biggest single-week increase since July 2011, jumping from 3.90 percent to 4.07 percent, the highest rate since April 2012. Points decreased to 0.35 from 0.39.

The average rate for 30-year jumbo FRMs (loan balances greater than $417,500) increased by 13 basis points to 4.20 percent, the highest rate since May 2012. Points increased to 0.28 from 0.27.

FHA-backed 30-year FRMs also increased to the highest level since May 2012, 3.76 percent, from 3.62 percent the previous week. Points increased to 0.32 from 0.27. The rate for 15-year FRMs reached the highest level since June 2012, increasing to 3.23 percent with 0.38 point from 3.10 percent with 0.30 point.

The Bottom line: Even a small rise in long-term interest rates translates into a lot less credit available for marginal borrowers. Homeowners trying to get a lower rate on their mortgage to free up cash for college loans or to put gas in the car will see that window close. Weak, highly-leveraged companies will have to get by with internally-generated cash – which many of them don’t have. The government, meanwhile, will have to roll over its debt at ever-higher rates or ever-shorter duration, leading to a rising deficit in the first case and increased exposure to future interest rate changes in the second. Either way, the system gets more instead of less fragile. The fact that a highly-leveraged economy can’t cope with rising rates is the modern world’s Catch-22: Rates have to rise if the economy keeps growing, but the economy can’t grow if rates rise.dollarcollapse.com/interest-rates-2/the-number-that-matters/ |

|

|

|

Post by jeffolie on Jun 10, 2013 11:06:43 GMT -6

" ... 'normalizing' rates here will crush the economy as interest expense surges (think Japan...) 30 Year T-Bond Yield 3.368% +0.44 Monday June 10, 2013, 12:55 my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending from HELOCS [home equity line of credits] =================================================== Treasury Yields Spike To New 14 Month Highs 06/10/2013 30Y rates are up 4bps and 10Y rates up 5bps as a combination of MBS convexity hedging, Taper chatter, and growth hopiness flutter across the bond market. This has backed 10Y and 30Y rates up to their highest since April 2012 - getting close to some significant support/resistance from the last few years. Mortgage spreads have stabilized up here at their highest since July (around 83bps) but just as a delicate reminder, the last time bond yields spiked to this degree, equities began to wonder just what was going on? With so much of the investing public having bought bond-like-stocks at the behest of every talking head and asset-gatherer under-the-sun, we wonder at what point do the arguments about a great rotation from bonds to stocks (since gosh, 10Y bond prices are down 3% in the last month) turn to a rotation from bond-like-stocks to bond-like-bonds...  www.zerohedge.com/sites/default/files/images/user3303/imageroot/2013/06/20130610_30Y.jpg www.zerohedge.com/sites/default/files/images/user3303/imageroot/2013/06/20130610_30Y.jpg Or more simply, the market's (or the Fed's) realization that 'normalizing' rates here will crush the economy as interest expense surges (think Japan...) www.zerohedge.com/news/2013-06-10/treasury-yields-spike-new-14-month-highs |

|

|

|

Post by jeffolie on Jun 13, 2013 14:51:37 GMT -6

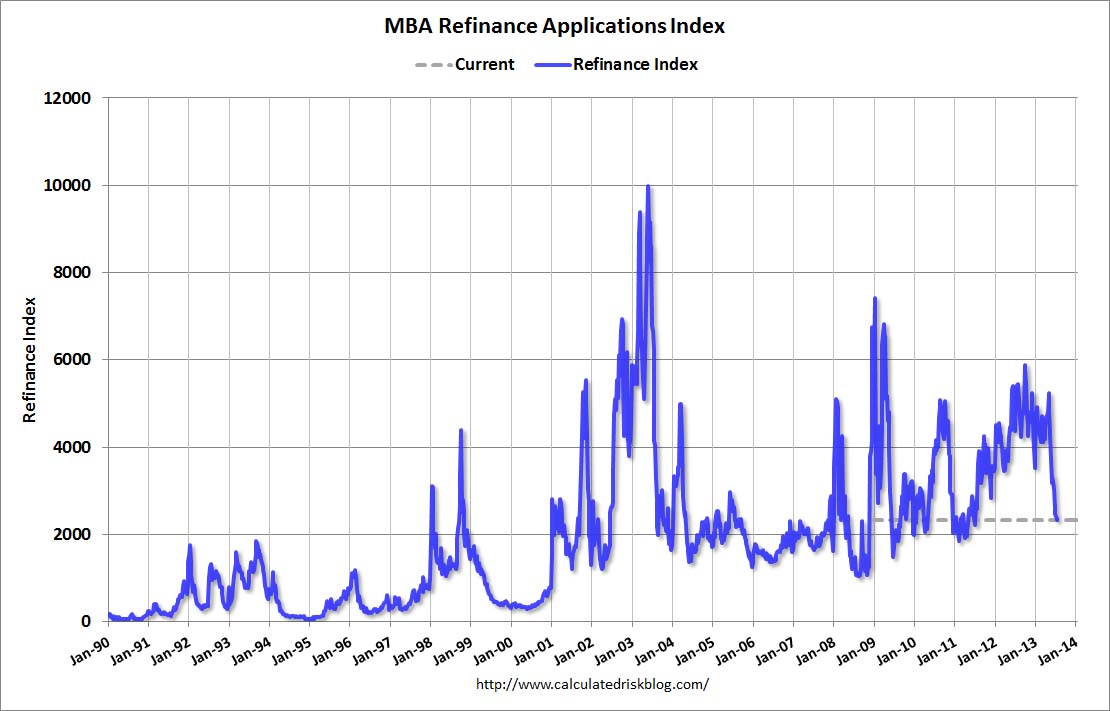

" .... "Mortgage Rates on Six Week Streak Higher" ... The refinance index has dropped sharply recently (down almost 36% over the last 5 weeks) and will probably decline significantly if rates stay at this level. Destroying refinance spending, higher rates June 2013 ============================================================ June 13, 2013 Freddie Mac: "Mortgage Rates on Six Week Streak Higher" by Bill McBride on 6/13/2013 From Freddie Mac today: Mortgage Rates on Six Week Streak Higher Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing fixed mortgage rates climbing higher amid a solid employment report for May. Since beginning their climb last month, the 30-year fixed-rate mortgage has increased over half a percentage point. ... 30-year fixed-rate mortgage (FRM) averaged 3.98 percent with an average 0.7 point for the week ending June 13, 2013, up from last week when it averaged 3.91 percent. Last year at this time, the 30-year FRM averaged 3.71 percent. 15-year FRM this week averaged 3.10 percent with an average 0.7 point, up from last week when it averaged 3.03 percent. A year ago at this time, the 15-year FRM averaged 2.98 percent. This graph shows the relationship between the monthly 10 year Treasury Yield and 30 year mortgage rates from the Freddie Mac survey.  3.bp.blogspot.com/-JttIH0gpWdc/UaUvtX0-vpI/AAAAAAAAae0/PTqdd0cf_lE/s1600/MortgageRatesTenYear.jpg 3.bp.blogspot.com/-JttIH0gpWdc/UaUvtX0-vpI/AAAAAAAAae0/PTqdd0cf_lE/s1600/MortgageRatesTenYear.jpg Currently the 10 year Treasury yield is 2.18% and 30 year mortgage rates are at 3.98% (according to Freddie Mac). Based on the relationship from the graph, if the ten year yield stays in this range, 30 year mortgage rates might move up to 4.1% or so in the Freddie Mac survey. Note: The yellow markers are for the last three years with the ten year yield below 3%. A trend line through the yellow markers only is a little lower, but still close to 4% at the current 10 year Treasury yield.  1.bp.blogspot.com/-LafZpgZXIy8/UbnyqFq8i0I/AAAAAAAAasY/twFu6DZ_QFM/s1600/RefiRatesJune132013.jpg 1.bp.blogspot.com/-LafZpgZXIy8/UbnyqFq8i0I/AAAAAAAAasY/twFu6DZ_QFM/s1600/RefiRatesJune132013.jpgThe second graph shows the 30 year fixed rate mortgage interest rate from the Freddie Mac Primary Mortgage Market Survey compared to the MBA refinance index. The refinance index has dropped sharply recently (down almost 36% over the last 5 weeks) and will probably decline significantly if rates stay at this level. www.calculatedriskblog.com/2013/06/freddie-mac-mortgage-rates-on-six-week.html |

|

|

|

Post by jeffolie on Jun 19, 2013 11:17:18 GMT -6

June 19, 2013 MBA: Mortgage Applications Decrease, Mortgage Rates Increase by Bill McBride on 6/19/2013 From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey The Refinance Index decreased 3 percent from the previous week. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. ... The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) increased to 4.17 percent, the highest rate since March 2012, from 4.15 percent, with points decreasing to 0.41 from 0.48 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. This is the sixth straight weekly increase for this rate. ... The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.30 percent from 3.32 percent, with points increasing to 0.39 from 0.38 (including the origination fee) for 80 percent LTV loans.  2.bp.blogspot.com/-zhyfEoGsbrE/UcGpum_8seI/AAAAAAAAavs/Z-kg7BiZ8MQ/s1600/MBARefiJune192013.jpg 2.bp.blogspot.com/-zhyfEoGsbrE/UcGpum_8seI/AAAAAAAAavs/Z-kg7BiZ8MQ/s1600/MBARefiJune192013.jpg The first graph shows the refinance index. With 30 year mortgage rates above 4%, refinance activity has fallen sharply, decreasing in 5 of the last 6 weeks. This index is down 38% over the last six weeks.  2.bp.blogspot.com/-ptuO7Ilmgng/UbhkUi4u8kI/AAAAAAAAaqY/nNR4og9THQU/s1600/MBAJune122013.jpg 2.bp.blogspot.com/-ptuO7Ilmgng/UbhkUi4u8kI/AAAAAAAAaqY/nNR4og9THQU/s1600/MBAJune122013.jpg The second graph shows the MBA mortgage purchase index. The 4-week average of the purchase index has generally been trending up over the last year, and the 4-week average of the purchase index is up almost 10% from a year ago. www.calculatedriskblog.com/2013/06/mba-mortgage-applications-decrease.html |

|

|

|

Post by jeffolie on Jul 17, 2013 7:52:04 GMT -6

Refinance Applications Decline in Latest Weekly Survey by Bill McBride on 7/17/2013 The Refinance Index decreased 4 percent from the previous week and is at its lowest level since July 2011. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The refinance share of mortgage activity decreased to 63 percent of total applications from 64 percent the previous week and is at its lowest level since April 2011. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) was unchanged at 4.68 percent, with points decreasing to 0.42 from 0.46 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.  4.bp.blogspot.com/-iX1QIYpFM8U/UeYpI0qDpCI/AAAAAAAAbG0/B85uE46SmpU/s1600/MBARefiJuly172013.jpg 4.bp.blogspot.com/-iX1QIYpFM8U/UeYpI0qDpCI/AAAAAAAAbG0/B85uE46SmpU/s1600/MBARefiJuly172013.jpgThe first graph shows the refinance index. With 30 year mortgage rates above 4.5%, refinance activity has fallen sharply, decreasing in 9 of the last 10 weeks.

This index is down 55% over the last ten weeks.

www.calculatedriskblog.com/2013/07/mba-mortgage-purchase-applications.html

|

|

|

|

Post by jeffolie on Jul 24, 2013 13:38:27 GMT -6

7/24/2013 From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey The Refinance Index decreased 1 percent from the previous week driven by a 12 percent drop in the Government Refinance index while the Conventional Refinance index rose by 2 percent. The Refinance Index is at the lowest level since July 2011. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The refinance share of mortgage activity remained unchanged at 63 percent of total applications. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) decreased to 4.58 percent from 4.68 percent, with points decreasing to 0.40 from 0.42 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. emphasis added  3.bp.blogspot.com/-Ea6zS-Fpios/Ue9dmH7642I/AAAAAAAAbMQ/Alg5_CWZ-So/s1600/MBARefiJuly232013.jpg 3.bp.blogspot.com/-Ea6zS-Fpios/Ue9dmH7642I/AAAAAAAAbMQ/Alg5_CWZ-So/s1600/MBARefiJuly232013.jpgThe first graph shows the refinance index. With 30 year mortgage rates above 4.5%, refinance activity has fallen sharply, decreasing in 10 of the last 11 weeks.

This index is down 55% over the last eleven weeks. 2.bp.blogspot.com/-Jd_bMRLKCO4/Ue9diJjYj8I/AAAAAAAAbMI/GFiz6oRIs_0/s1600/MBAJuly2232013.jpg 2.bp.blogspot.com/-Jd_bMRLKCO4/Ue9diJjYj8I/AAAAAAAAbMI/GFiz6oRIs_0/s1600/MBAJuly2232013.jpg The second graph shows the MBA mortgage purchase index. The 4-week average of the purchase index has generally been trending up over the last year (but down over the last several weeks), and the 4-week average of the purchase index is up about 6% from a year ago. www.calculatedriskblog.com/ |

|

|

|

Post by jeffolie on Jul 31, 2013 16:33:33 GMT -6

|

|

|

|

Post by jeffolie on Aug 14, 2013 8:06:34 GMT -6

Destroying refinance spending, higher higher rates June 2013 " ... The refinancing index is down 59% over the last 3 months ... decreased 4 percent from the previous week .... my jeffolie view: refinancing promotes middle class spending from home equity, higher rates have destroyed what remains of middle class spending HELOCS [home equity line of credits] =============================================== August 14, 2013 MBA: Mortgage Applications decrease in Latest Weekly Survey by Bill McBride on 8/14/2013 From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey Mortgage applications decreased 4.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 9, 2013. ... The Refinance Index decreased 4 percent from the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. ... The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) decreased to 4.56 percent from 4.61 percent, with points decreasing to 0.39 from 0.42 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. ... The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.60 percent from 3.66 percent, with points decreasing to 0.35 from 0.43 (including the origination fee) for 80 percent LTV loans. Mortgage Refinance Index  3.bp.blogspot.com/-OosCzw3d4rM/UgrU9JZrZoI/AAAAAAAAbfM/Z2aY8EpU5iE/s1600/MBARefiAug142013.jpg 3.bp.blogspot.com/-OosCzw3d4rM/UgrU9JZrZoI/AAAAAAAAbfM/Z2aY8EpU5iE/s1600/MBARefiAug142013.jpg The first graph shows the refinance index. With 30 year mortgage rates up over the last 3 months, refinance activity has fallen sharply, decreasing in 12 of the last 14 weeks. This index is down 59% over the last 3 months. The last time the index declined this far was in late 2010 and early 2011 when mortgage increased sharply with the Ten Year Treasury rising from 2.5% to 3.5%. We've seen a similar increase over the last few months with the Ten Year Treasury yield up from 1.6% to over 2.7% today. Mortgage Purchase Index The second graph shows the MBA mortgage purchase index. The 4-week average of the purchase index has generally been trending up over the last year (but down over the couple of months), and the 4-week average of the purchase index is up about 7% from a year ago.  1.bp.blogspot.com/-rHkeHB0Km-o/UgrVFPmdGWI/AAAAAAAAbfU/8r6uxeIp0ng/s1600/MBAAug142013.jpgwww.calculatedriskblog.com/ 1.bp.blogspot.com/-rHkeHB0Km-o/UgrVFPmdGWI/AAAAAAAAbfU/8r6uxeIp0ng/s1600/MBAAug142013.jpgwww.calculatedriskblog.com/

|

|

|

|

Post by jeffolie on Aug 28, 2013 11:15:03 GMT -6

|

|

|

|

Post by jeffolie on Sept 4, 2013 7:31:48 GMT -6

|

|

|

|

Post by jeffolie on Sept 11, 2013 7:53:08 GMT -6

MBA: Mortgage Refinance Activity at Lowest Level since 2009 by Bill McBride on 9/11/2013 From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey Mortgage applications decreased 13.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 6, 2013. This week’s results included an adjustment for the Labor Day holiday. ... The Refinance Index decreased 20 percent from the previous week. The Refinance Index has fallen 71 percent from its recent peak the week of May 3, 2013 and is at the lowest level since June 2009. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. ... The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.80 percent from 4.73 percent, with points increasing to 0.46 from 0.33 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. Mortgage Refinance Index  1.bp.blogspot.com/-F9jCY0wHZMw/Ui-lVW4m2YI/AAAAAAAAb7Q/FwLhqavJiE8/s1600/MBARefiSept112013.jpg 1.bp.blogspot.com/-F9jCY0wHZMw/Ui-lVW4m2YI/AAAAAAAAb7Q/FwLhqavJiE8/s1600/MBARefiSept112013.jpg The first graph shows the refinance index. The refinance index is down 71% since early May. The last time the index declined like this was in late 2010 and early 2011 when mortgage increased sharply with the Ten Year Treasury rising from 2.5% to 3.5%. We've seen an even larger increase over the last few months with the Ten Year Treasury yield up from 1.6% to over 2.96% today. We will probably see the refinance index back to 2000 levels soon. Mortgage Purchase Index The second graph shows the MBA mortgage purchase index. The 4-week average of the purchase index  3.bp.blogspot.com/-zfEDhkSU2ik/Ui-lR6pEFVI/AAAAAAAAb7I/1hRILFwA_ew/s1600/MBASept112013.jpgwww.calculatedriskblog.com/ 3.bp.blogspot.com/-zfEDhkSU2ik/Ui-lR6pEFVI/AAAAAAAAb7I/1hRILFwA_ew/s1600/MBASept112013.jpgwww.calculatedriskblog.com/ |

|