|

|

Post by unlawflcombatnt on Dec 23, 2023 9:09:00 GMT -6

Here's a recent article listing allegedly US companies that are owned by foreign entities:

from the Pittsburgh Tribune

December 19, 2023

by Samantha DelouyaThese all-American brands aren’t actually American"US Steel was once the pride and joy of the United States and the most valuable company in the entire world. The 122-year-old company has agreed to be bought by Japanese firm Nippon Steel in a $14.1 billion deal. But this isn’t the first instance of an international company snapping up a classic American brand.... Here are some of the most notable examples: GE appliances.... The company was founded by legendary American inventor Thomas Edison. But Americans with a GE microwave or washing machine in their homes may not realize that General Electric’s century-old appliance division is owned by Haier Group, based in Qingdao, China. Haier bought the division from General Electric for $5.6 billion in 2016, as General Electric’s business stalled and it looked to raise cash to chip away at a mountain of debt. Haier is itself a major appliance seller in the United States, with its own products offered at US stores such as Home Depot and Lowe’s. Budweiser.... Budweiser’s brewer, named Anheuser-Busch after the company’s founders, was created in the United States in 1879 and helped pioneer pasteurization technology that allowed beers to be shipped across the country without spoiling, according to its website. But Budweiser’s parent company was acquired by European alcohol conglomerate InBev in 2008, forming a new company: AB InBev, based in Leuven, Belgium. AB InBev also owns other well-known beer brands like Corona and Stella Artois. Burger King The current home of the Whopper is Toronto, Canada — kind of. The seminal fast food chain, founded in Miami in 1954, has been part of Canadian conglomerate Restaurant Brands International for nearly a decade. RBI was formed in 2014 with a $12.5 billion merger between Burger King and Canada-based coffeehouse Tim Hortons. While RBI’s headquarters is in Toronto, Burger King’s functional headquarters remains in Miami. Since RBI’s creation, it has snapped up two more popular food brands: Popeye’s Louisiana Kitchen and Firehouse Subs. 7-Eleven.... More than 13,000 7-Eleven stores operate in the US, making it one of the largest convenience store chains in the country. But there are even more 7-Eleven stores in Japan, according to the company. That’s because the corner store, founded in 1927 in Texas, is owned by Seven & I Holdings, a Japanese retailer based in Tokyo. Seven & I officially became the sole owner of 7-Eleven in 2005, after Ito-Yokado, a unit of Seven & I, first bought a stake in the convenience store in 1991. Trader Joe’s California-based Trader Joe’s brands itself as a “national chain of neighborhood grocery stores.” But the grocery chain known for its private label goods and competitive prices is owned by the same German family that founded another well-known grocery store: Aldi. Aldi, which was founded by brothers Karl and Theo Albrecht in 1946, was cleaved in half in the 1960s. One half of the Albrecht family owns Aldi Nord, while the other half owns Aldi Sud. Trader Joe’s has been under Aldi Nord’s ownership since 1979, while Aldi-branded grocery stores in the US are owned by Aldi Sud, meaning the two chains have no business relationship. Jeep, Chrysler and Dodge cars The Jeep Wrangler was first introduced at the 1986 Chicago Auto Show, but its roots date back to World War II, when the US Army used an earlier version as a reconnaissance vehicle around battlefields, according to Jeep. The famed model, with its rugged design and off-road capabilities, has had enduring appeal in America. But Jeep and its siblings Chrysler and Dodge have belonged to European companies since 2014, when Italian company Fiat Group acquired 100% ownership of Chrysler Group. In 2021, Fiat Chrysler Automotive Group, as it was then called, merged with French manufacturer PSA Group, creating Stellantis. The Amsterdam-based auto giant is now the fourth-largest automaker in the world by volume and part of the Detroit “Big Three” automakers in the US. Frigidaire Refrigerator appliance company Frigidaire is responsible for a lot of firsts in America: According to the company, it is the inventor of the first self-contained refrigerator and the first-ever home freezer, which it originally called the “ice cream cabinet.” Frigidaire joins GE Appliances as a brand once owned by General Electric. The refrigerator maker was part of the Edison-founded conglomerate from 1919 to 1979. After brief ownership by White Consolidated Industries, Frigidaire was bought by Swedish multinational home appliance manufacturer Electrolux AB in 1986 — and it has remained in its ownership ever since. Ben & Jerry’s Ben & Jerry’s is best known for its quirky ice cream flavors with pun-filled names like “Cherry Garcia” and “Phish Food.” The ice cream company, which was founded in 1978 by school friends Ben Cohen and Jerry Greenfield in a converted Vermont gas station, was acquired by British conglomerate Unilever in 2000. That means the sweet treat shares a home with consumer goods like Axe Body Spray and Vaseline. One company that is American… While many brands with international owners may seek to highlight their American roots, at least one of Ben & Jerry’s competitors decided on a different route. Häagen-Dazs was cooked up by Polish immigrants Reuben and Rose Mattus in 1960 in the Bronx, New York. The couple invented a made-up Danish-sounding name for the brand, likely adding an air of mystery to the ice cream makers’ origins in the decades since."

|

|

|

|

Post by unlawflcombatnt on Oct 9, 2021 12:07:45 GMT -6

Dr. Jain in Santa Monica is the best Infertility doctor that I know about.

I don't have the exact address and number at hand, but I'll try to find it.

We now have a 4-year old son, thanks to Dr. Jain

|

|

|

|

Post by unlawflcombatnt on Jan 1, 2020 8:16:55 GMT -6

from USA Today www.usatoday.com/story/money/2019/10/07/ge-pension-freeze-reasons-defined-benefit-plans-are-dead/3898630002/4 reasons the corporate pension is on its deathbedby Nathan Bomey "GE on Monday announced that it would offer lump-sum pension buyouts to about 100,000 former U.S. employees who have not yet begun receiving their pensions. The company, which has been facing pressure to bolster its finances, also announced plans to freeze pension benefits for about 20,700 salaried pensioners at current levels. Taken together, the moves illustrate how corporate America has largely ditched pensions, which are swiftly becoming a thing of the past for active employees who don't work for the government..... Here are 4 key reasons why:

1. Pensions are seen as expensive, risky

Defined-benefit pension plans are viewed as expensive and risky to maintain: Corporations are making promises to pay out benefits for decades but may not be able to guarantee their own financial success for the same period of time. If they fall on hard times, pension promises can become burdensome. As a result, they have largely shifted investment risk to individual workers. Instead of managing investments on behalf of employees in the form of corporate pension funds, companies have formed defined-contribution plans like 401(k)s, which typically require tax-free withdrawals from people's paychecks. If the worker's money is invested successfully, the payoff can be lucrative. But if the investments sour or the market tanks, workers, not the company, are on the hook for finding additional income. "A pension is a promise to pay monthly benefits for as long as the employee lives after retirement," Munnell said. "For employers, a system where they bear all the costs and all the risks is not appealing." 2. Union power has diminishedAs private-sector unions have withered, so have private-sector pensions. Unions have historically championed defined-benefit pensions for their members. For example, the United Auto Workers union is currently bargaining for improved pension benefits.... But the percentage of American private-sector workers in a union was only 6.4% in 2018, compared with 33.9% in the public sector, according to the Department of Labor's Bureau of Labor Statistics. The nation's overall unionized rate of 10.5%, which includes public workers, is down from its all-time high of 20.1% in 1983, the 1st year comparable BLS figures are available.3. 401(k)s have been normalizedA series of tax law changes in recent decades has enabled the rise of defined-contribution plans like 401(k)s. Until the 1980s, this was not a normal employee benefit. Today it is. More than 100 million people have 401(k)-style benefits, according to the Department of Labor. Critics say it's not enough. The Economic Policy Institute says 401(k)s are a "poor substitute" for defined-benefit pensions, in part because many people simply aren't saving enough and small businesses are less likely than large companies to offer them. But advocates say the defined-contribution approach gives workers more control over their money and they point out that defined-benefit pensions are vulnerable to corporate bankruptcy, mismanagement, and corruption. Also, in the modern economy, many workers prize the ability to move from company to company, instead of accruing benefits at a single employer. That emphasis on mobility tends to favor 401(k)-style plans. "It’s really only the older companies that have residual defined-benefit plans," Munnell said. 4. Public companies are under pressure to reduce pension debtAs public companies face pressure to deliver positive quarterly earnings, one area they often seek to improve is their general liabilities. That can involve slashing debt to earn a better credit rating, which typically makes it cheaper to borrow or win over investors. When GE announced its pension moves Monday, analysts welcomed the plan. "This move shows that GE is looking to pull any and all levers to restore its financial health," CFRA Research stock analyst Jim Corridore said in a research note. The major ratings agencies often praise companies for reducing their pension liabilities. And despite the pivot away from defined-benefit plans, corporations still owe a lot. The top 100 private plans alone owe their workers $1.66 trillion, according to actuarial firm Milliman. In other words, while most active employees won't be getting a pension, the legacy of America's pension system will live on for decades." |

|

|

|

Post by unlawflcombatnt on Jan 1, 2020 7:50:43 GMT -6

www.yahoo.com/finance/news/really-over-corporate-pensions-head-050108115.html'It's really over': Corporate pensions head for extinctionfrom USA TODAY Dec 10, 2019 by Nathan Bomey "The practice of companies sending monthly retirement checks to their former workers is headed for extinction, and remaining pension funds are in tough financial shape. Nearly 2/3 of pension funds are considering dropping guaranteed benefits to new workers within the next 5 years, according to a human resources consulting firm that studied the matter. Despite gains in the stock market this year, U.S. pension plans are near their worst financial state in 2 years, according to the new report by Mercer, which casts a spotlight on the escalating cost of past promises to employees. Most U.S. companies no longer offer defined-benefit pensions, which typically provided guaranteed monthly payments to workers when they retired. But pension funds that still operate must gain in value to ensure they have enough to meet their obligations. By late 2019, the average pension fund had 85% of the funds necessary to meet its obligations over time due largely to low interest rates, according to Mercer's 2020 Defined Benefit Outlook. The firm also reported that 63% of companies with defined-benefit pensions "are considering termination" of the plan within half a decade. That would mean the pensions would be closed off to future participants. The report comes as corporate pensions continue to disappear. General Electric announced in October that it would offer lump-sum pension buyouts to about 100,000 former U.S. employees who have not yet begun receiving their pensions. The company, which has been facing pressure to bolster its finances, also announced plans to freeze pension benefits for about 20,700 salaried pensioners at current levels. "In the bigger picture, GE is just going the way that most of the private sector in the United States has gone," Alicia Munnell, director of the Center for Retirement Research at Boston College, said in a recent interview. "It’s really over in the private sector. The question is, just when does the last plan close down?" The number of pension plans offering defined benefits – which means the payouts are guaranteed – plummeted by about 73% from 1986 to 2016, according to the Department of Labor's Employee Benefits Security Administration. That's due to a mix of reasons, including risk, costs, declining union power and the rise of 401(k)-style defined-contribution plans, which require workers to kick in their own funds for retirement investments, often with a company match."

|

|

|

|

Post by unlawflcombatnt on Dec 24, 2019 9:31:06 GMT -6

Lukesjohn65,

I couldn't agree more.

Innocent people can, and do, go to prison because they couldn't afford attorneys.

|

|

|

|

Post by unlawflcombatnt on Apr 14, 2019 7:31:46 GMT -6

The Basic Facts of best bitcoin exchange Such a coin is going to be preferred by lots of people over the other ecoins in the marketplace. Rather than relying on miners to fix complex mathematical issues, proof-of-stake coins utilize the stakes themselves to secure the network. There are lots of coins in the cryptocurrency market which use proof-of-stake to guarantee the blockchain. Can you explain what "proof-of-stake" means? |

|

|

|

Post by unlawflcombatnt on Sept 22, 2018 7:19:51 GMT -6

from PaulCraigRoberts.org Freedom Where Did You Go? Sept 22, 2018 by Paul Craig Roberts "My Generation is the last one to have known privacy and to have lived out most of our lives in freedom. I remember when driving licenses did not have photos and most certainly not fingerprints. A driving license was issued on proof of birth date alone. Prior to the appearance of automobiles IDs did not exist in democratic nations. You were who you said you were. The intrusive questions that accost us every day, even when doing something simple as reporting a telephone or Internet connection being out or inquiring about a credit card charge, were impermissible. I remember when you could telephone a utility company, for example, have the telephone answered no later than the third ring with a real person on the line who could clear up the problem in a few minutes without having to know your Social Security number and your mother’s maiden name. Today, after half an hour with robot voices asking intrusive questions you might finally get a real person somewhere in Asia who is controlled by such a tight system of rules that the person is, in effect, a robot. The person is not permitted to use any judgment or discretion and you listen to advertisements for another half hour while you wait for a supervisor who promises to have the matter looked into. The minute you go online, you are subject to collection of information about yourself. You don’t even know it is being collected. According to reports, soon our stoves, refrigerators, and microwave ovens will be reporting on us. The new cars already do. When privacy disappears, there are no private persons. So what do people become? They become Big Brother’s subjects. We are at that point now. This interview witth Julian Assange is worth the 53 minutes: www.rt.com/news/438968-assange-last-interview-blackout/ Think about Assange for a minute. He has done nothing wrong. There are no charges against him. All charges have been dismissed. But he cannot walk out of the Ecuadoran Embassy in London without being seized by the British police and handed over to Washington whose prosecutorial apparatus intends to prosecute Assange for treason although he is not a US citizen but an Australian and Ecuadoran citizen. What did Assange do? Nothing but practice journalism. His problem, his only problem, is that his journalism embarrassed Washington, and Washington intends revenge. Law is nowhere in the picture. The UK is breaking all known laws including its own by the forced detention of Assange in the Ecuadoran Embassy. The US in its determination to get Assange has no law whatsoever on which to stand. It only has raw unbridled power that can operate without law. In other words, the Anglo-American world is totally lawless. Yet the Russian government holds firmly to its delusion that the US and Britain are countries with which agreementts can be made. The digital world makes Big Brother’s Memory Hole possible. No need to burn books. Just push a button and information disappears. As I write Google, Facebook, Twitter, Amazon, Apple, and so forth are all making non-approved information disappear. In a digital world, not only can our identities be stolen—indeed, it can be stolen multiple times so that there are many of you at the same time—but we can also be erased. Poof—push a button and there you go. This makes murder easy. You never existed. As I said before and will say again, the digital world and artificial intelligence are a far worse disaster for mankind than ever was the Black Plague. All the smart people busy at work creating the new world are destroying the human race." Article printed from PaulCraigRoberts.org: www.paulcraigroberts.org URL to article: www.paulcraigroberts.org/2018/09/22/freedom-where-did-you-go/ |

|

|

|

Post by unlawflcombatnt on Aug 18, 2018 12:16:19 GMT -6

from Coalition for a Prosperous America August 13, 2018 By Jeff Ferry, CPA Research Director "It’s just six months since the first of the Trump administration’s tariffs went into effect and the job gains are already visible. Our CPA Tariff Job Creation Tracker (TJCT) shows over 11,000 jobs have been created or announced since February 1st and that includes only cases where companies announced specific job counts. Other companies have also said they intend to add jobs, but we will wait for numbers before adding them to the TJCT. In general, these are good, well-paying jobs, in strong, stable industries. The addition of high-paying jobs to any locality creates upward pressure on wages in the entire region. The process is just beginning. More tariffs, which were previously announced, are being finalized and implemented. The so-called “second tranche” of section 301 tariffs recently announced on 279 lines amounting to about $16 billion of Chinese imports will go into effect on August 23. Hearings will be held on August 20 by the US Trade Representative’s office relating to the proposal of 10% to 25% tariffs on an additional $200 billion of Chinese imports. As a result, we should expect to see more future job creation by domestic companies that make or can make products associated with those tariff lines. A good example of the job creation now underway is the expansion by Magnitude 7 Metals, in New Madrid, Missouri. Privately-owned American company Magnitude 7 bought the aluminum smelting facilities out of bankruptcy after previous owner Noranda failed, due largely to international competition which forced some 90% of US aluminum smelters out of business. In March, Missouri Governor Eric Greitens spoke at an event at Magnitude 7, praising the company for relaunching the smelter and creating jobs offering average annual pay of $64,000. “These jobs will improve the whole economy in the region. It means more money for the schools. It means more customers for the restaurants,” Governor Greitens told the crowd. n total, our tracker shows 2,899 jobs have been announced or created in the aluminum industry since February. In the steel sector, industry leaders Nucor and US Steel have announced expansions and re-openings of previously shuttered facilities. Nucor has also announced plans to build a new greenfield steel mill in Frostburg, Florida, creating 250 jobs at an average pay of $66,000 a year. Less well known is that smaller steel companies are expanding too. Big River Steel, a steel startup, is investing in its Arkansas mill to double production capacity to 3.3 million tons a year. Big River is also planning to open a second mill in Brownsville, Texas, which will employ 500 steelworkers. Our tracker shows a total of 4,960 new jobs planned in the steel industry. The solar panel industry was the first industry where the administration announced tariffs, back in January. Some doom-mongers predicted disaster for the industry. Instead, the solar industry is booming. Around 10 solar manufacturing companies have announced investment and job creation in solar manufacturing facilities, from Oregon to Florida. In April, First Solar Corp. announced a $400 million expansion at its Ohio plant, which will create 500 new jobs. First Solar’s innovative thin-film solar cells are not directly affected by the solar tariffs, but its ability to build a strong manufacturing capability depends on the existence of a robust solar supply chain and the required skills here in the US. The solar tariffs are designed to achieve exactly that. According to jobs website Glassdoor, a manufacturing operator at First Solar earns about $37,000 a year while a development engineer earns $97,000. Our tracker shows new solar jobs at 1,150 so far, and new jobs in the washing machine industry at 2,100. Add up those four categories and you get 11,100 new jobs. And that’s without counting jobs that will be created in the diverse industries and sectors where the administration is levying tariffs on Chinese imports worth $50 billion a year. It’s the Supply Chain The United States made a huge mistake in the 1990s and early 2000s when it allowed entire manufacturing supply chains to move to Asia. Manufacturing is too important for employment, wealth, and income creation to allow so much of it to move overseas. Further, manufacturing success is not about individual products or stages of production dispersed over different countries thousands of miles apart. Skills and knowledge tend to cluster together, and they grow and develop best in close proximity. So it’s especially good news to see growth in broader supply chains. A good example is the recent announcement by iron ore miner Cleveland Cliffs of a new facility to process ore in Toledo, Ohio. That facility is targeted to create 1,200 new jobs. Across the industrial world, there is growing awareness that local and in-country production is coming back into fashion. Another way to put it is that the corporate strategy of saving a few cents on every input by disaggregating production and siting it all over the world is going out of fashion. The change is not just the result of President Trump’s tariffs, or of China’s blatantly offensive IP theft, (such as the latest case of a Chinese Apple employee arrested by the FBI at San Jose Airport on July 7th, after allegedly walking out of an Apple lab with stolen circuit boards and heading for a job at a Chinese autonomous vehicle competitor). For example, inverters transform the voltage generated by solar cells into domestic AC current and are an essential part of every solar system. Inverter maker Chint Power Systems recently announced plans to increase inverter production at its Texas facility and said it’s actively seeking a second location for US manufacturing. Chint is partly motivated by the likely third round of Chinese tariffs under consideration, but the US manager of Chint has also said he also is seeking to work closely with “customers that plan projects closely with us.” Similarly, Giant, the Taiwan-based bicycle market leader that made 4.4 million bikes last year, mainly in China, recently told the Financial Times that it is investing in production in eastern Europe as there is a global trend to reduce dependence on Chinese production. The European Union recently enacted anti-dumping tariffs on Chinese electric bikes. Supported by tariffs on both sides of the Atlantic, the business community is actively seeking to diversify out of China and find new locations in Asia, the US, and Europe. It’s the beginnings of a new world manufacturing order. US Public Companies Need to Wake Up and Diversify Their Manufacturing But there is one group of companies dragging their feet: American companies, and particularly publicly quoted American companies. In solar inverters, there are three large players, two Chinese and one American. Chint, one of the Chinese manufacturers, is seeking to expand US production. The sole American producer, Enphase, still produces all its inverters in China. Like many tech companies, it has a contentious relationship with its Wall Street investors. The stock is under attack from a hedge fund. Enphase CEO Badri Kothandaraman recently said: “We are laser focused on our number one priority: improve profitability quarter on quarter and creating further shareholder value.” It is this short-term obsession that prevents US tech companies from seeing the bigger picture and seeking to build a business for the long term, which would include global manufacturing. There is also a herd mentality in which tech company executives believe investors will only support manufacturing in the cheapest markets. That’s part of the reason Apple has not lived up to vague suggestions by Tim Cook that it would build US manufacturing—while its Taiwan-based supplier, Foxconn, is going ahead with a large Wisconsin manufacturing facility. US government action is needed to change this dynamic. Downstream Industry Impact While many companies are benefiting from the tariffs, there are also some companies that pay higher prices for the tariffed products. Those companies either pass the price increase along, reduce their profit, or lay off workers depending upon the nature of their market. The administration should follow up the existing tariffs with tariffs to protect downstream industries. More generalized tariff coverage causes fewer distortions than targeted tariffs. It is already doing so, with its “second tranche” of tariffs against $16 billion of Chinese imports and the upcoming third tranche. But more may need to be done. Free traders wrongly focus only upon alleged “efficiency gains” of trade. But they incorrectly assume that displaced workers quickly find jobs of equal quality. That assumption has now been proven untrue. Large numbers of those who lose their jobs due to import competition either leave the workforce or find jobs at significantly lower pay. Their current and future earnings are severely reduced. Marginal efficiency gains are dwarfed by the aggregate wage reduction. It is also important to note that future innovation and productive capacity from lost industries, often high tech industries, are forfeited forever. Tariffs present a strong initial solution to the job and industry losses caused by foreign subsidies, dumping, and China’s acts, policies and practices of commercial espionage, technology theft, and weaponized incoming investment." |

|

|

|

Post by unlawflcombatnt on Aug 5, 2018 11:07:26 GMT -6

TARIFFS: Did Tariffs Make America Great?by Pat Buchanan buchanan.org/blog/did-tariffs-make-america-great-129752" "Make America Great Again!" will, given the astonishing victory it produced for Donald Trump, be recorded among the most successful slogans in political history. Yet it raises a question: How did America first become the world's greatest economic power? In 1998, in "The Great Betrayal: How American Sovereignty and Social Justice Are Being Sacrificed to the Gods of the Global Economy," this writer sought to explain. However, as the blazing issue of that day was Monica Lewinsky and Bill Clinton, it was no easy task to steer interviewers around to the McKinley Tariff. Free trade propaganda aside, what is the historical truth? The Great Betrayal As our Revolution was about political independence, the first words and acts of our constitutional republic were about ensuring America's economic independence. "A free people should promote such manufactures as tend to render them independent on others for essentials, especially military supplies," said President Washington in his first message to Congress. The first major bill passed by Congress was the Tariff Act of 1789. Weeks later, Washington imposed tonnage taxes all foreign shipping. The U.S. Merchant Marine was born. In 1791, Treasury Secretary Alexander Hamilton wrote in his famous Report on Manufactures: "The wealth ... independence, and security of a Country, appear to be materially connected with the prosperity of manufactures. Every nation ... ought to endeavor to possess within itself all the essentials of national supply. These compromise the means of subsistence, habitation, clothing, and defence." During the War of 1812, British merchants lost their American markets. When peace came, flotillas of British ships arrived at U.S. ports to dump underpriced goods and to recapture the markets the Brits had lost. Have something to say about this column? Visit Pat's FaceBook page and post your comments.... Henry Clay and John Calhoun backed James Madison's Tariff of 1816, as did ex-free traders Jefferson and John Adams. It worked. In 1816, the U.S. produced 840 thousand yards of cloth. By 1820, it was 13,874 thousand yards. America had become self-sufficient. Financing "internal improvements" with tariffs on foreign goods would become known abroad as "The American System." Said Daniel Webster, "Protection of our own labor against the cheaper, ill-paid, half-fed, and pauper labor of Europe, is ... a duty which the country owes to its own citizens." This is economic patriotism, a conservatism of the heart. Globalists, cosmopolites and one-worlders recoil at phrases like "America First." Campaigning for Henry Clay, "The Father of the American System," in 1844, Abe Lincoln issued an impassioned plea, "Give us a protective tariff and we will have the greatest nation on earth." Battling free trade in the Polk presidency, Congressman Lincoln said, "Abandonment of the protective policy by the American Government must result in the increase of both useless labor and idleness and ... must produce want and ruin among our people." In our time, the abandonment of economic patriotism produced in Middle America what Lincoln predicted, and what got Trump elected. From the Civil War to the 20th century, U.S. economic policy was grounded in the Morrill Tariffs, named for Vermont Congressman and Senator Justin Morrill who, as early as 1857, had declared: "I am for ruling America for the benefit, first, of Americans, and, for the 'rest of mankind' afterwards." To Morrill, free trade was treason: "Free trade abjures patriotism and boasts of cosmopolitanism. It regards the labor of our own people with no more favor than that of the barbarian on the Danube or the cooly on the Ganges." William McKinley, the veteran of Antietam who gave his name to the McKinley Tariff, declared, four years before being elected president: "Free trade results in our giving our money ... our manufactures and our markets to other nations. ... It will bring widespread discontent. It will revolutionize our values." Campaigning in 1892, McKinley said, "Open competition between high-paid American labor and poorly paid European labor will either drive out of existence American industry or lower American wages." Substitute "Asian labor" for "European labor" and is this not a fair description of what free trade did to U.S. manufacturing these last 25 years? Some $12 trillion in trade deficits, arrested wages for our workers, six million manufacturing jobs lost, 55,000 factories and plants shut down. McKinley's future Vice President Teddy Roosevelt agreed with him, "Thank God I am not a free trader." What did the Protectionists produce? From 1869 to 1900, GDP quadrupled. Budget surpluses were run for 27 straight years. The U.S. debt was cut two-thirds to 7 percent of GDP. Commodity prices fell 58 percent. U.S. population doubled, but real wages rose 53 percent. Economic growth averaged 4 percent a year. And the United States, which began this era with half of Britain's production, ended it with twice Britain's production. Under Warren Harding, Cal Coolidge and the Fordney-McCumber Tariff, GDP growth from 1922 to 1927 hit 7 percent, an all-time record. Economic patriotism put America first, and made America first. Of GOP free traders, the steel magnate Joseph Wharton, whose name graces the college Trump attended, said it well: "Republicans who are shaky on protection are shaky all over." "

|

|

|

|

Post by unlawflcombatnt on Mar 18, 2018 8:27:32 GMT -6

buchanan.org/blog/gop-terrified-tariffs-128840March 2018 By Patrick J. Buchanan "From Lincoln to William McKinley to Theodore Roosevelt, and from Warren Harding through Calvin Coolidge, the Republican Party erected the most awesome manufacturing machine the world had ever seen. And, as the party of high tariffs through those seven decades, the GOP was rewarded by becoming America’s Party. Thirteen Republican presidents served from 1860 to 1930, and only two Democrats. And Grover Cleveland and Woodrow Wilson were elected only because the Republicans had split. Why, then, this terror of tariffs that grips the GOP? Consider. On hearing that President Trump might impose tariffs on aluminum and steel, Sen. Lindsey Graham was beside himself: “Please reconsider,” he implored the president, “you’re making a huge mistake.” Twenty-four hours earlier, Graham had confidently assured us that war with a nuclear-armed North Korea is “worth it.” “All the damage that would come from a war would be worth it in terms of long-term stability and national security,” said Graham. A steel tariff terrifies Graham. A new Korean war does not? “Trade wars are not won, only lost,” warns Sen. Jeff Flake. But this is ahistorical nonsense. The U.S. relied on tariffs to convert from an agricultural economy in 1800 to the mightiest manufacturing power on earth by 1900. Bismarck’s Germany, born in 1871, followed the U.S. example, and swept past free trade Britain before World War I. Does Senator Flake think Japan rose to post-war preeminence through free trade, as Tokyo kept U.S. products out, while dumping cars, radios, TVs and motorcycles here to kill the industries of the nation that was defending them. Both Nixon and Reagan had to devalue the dollar to counter the predatory trade policies of Japan. Since Bush I, we have run $12 trillion in trade deficits, and, in the first decade in this century, we lost 55,000 factories and 6,000,000 manufacturing jobs. Does Flake see no correlation between America’s decline, China’s rise, and the $4 trillion in trade surpluses Beijing has run up at the expense of his own country? The hysteria that greeted Trump’s idea of a 25 percent tariff on steel and 10 percent tariff on aluminum suggest that restoring this nation’s economic independence is going to be a rocky road. In 2017, the U.S. ran a trade deficit in goods of almost $800 billion, $375 billion of that with China, a trade surplus that easily covered Xi Jinping’s entire defense budget. If we are to turn our $800 billion trade deficit in goods into an $800 billion surplus, and stop the looting of America’s industrial base and the gutting of our cities and towns, sacrifices will have to be made. But if we are not up to it, we will lose our independence, as the countries of the EU have lost theirs. Specifically, we need to shift taxes off goods produced in the USA, and impose taxes on goods imported into the USA. As we import nearly $2.5 trillion in goods, a tariff on imported goods, rising gradually to 20 percent, would initially produce $500 billion in revenue. All that tariff revenue could be used to eliminate and replace all taxes on production inside the USA. As the price of foreign goods rose, U.S. products would replace foreign-made products. There’s nothing in the world that we cannot produce here. And if it can be made in America, it should be made in America. Consider. Assume a Lexus cost $50,000 in the U.S., and a 20 percent tariff were imposed, raising the price to $60,000. What would the Japanese producers of Lexus do? They could accept the loss in sales in the world’s greatest market, the USA. They could cut their prices to hold their U.S. market share. Or they could shift production to the United States, building their cars here and keeping their market. How have EU nations run up endless trade surpluses with America? By imposing a value-added tax, or VAT, on imports from the U.S., while rebating the VAT on exports to the USA. Works just like a tariff. The principles behind a policy of economic nationalism, to turn our trade deficits, which subtract from GDP, into trade surpluses, which add to GDP, are these: Production comes before consumption. Who consumes the apples is less important than who owns the orchard. We should depend more upon each other and less upon foreign lands. We should tax foreign-made goods and use the revenue, dollar for dollar, to cut taxes on domestic production. The idea is not to keep foreign goods out, but to induce foreign companies to move production here. We have a strategic asset no one else can match. We control access to the largest richest market on earth, the USA. And just as states charge higher tuition on out-of state students at their top universities, we should charge a price of admission for foreign producers to get into America’s markets. And — someone get a hold of Sen. Graham — it’s called a tariff."

|

|

|

|

Post by unlawflcombatnt on Mar 11, 2018 11:17:24 GMT -6

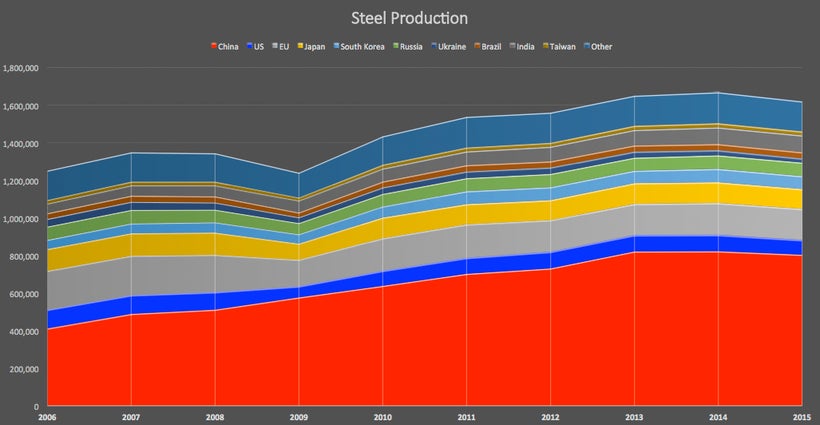

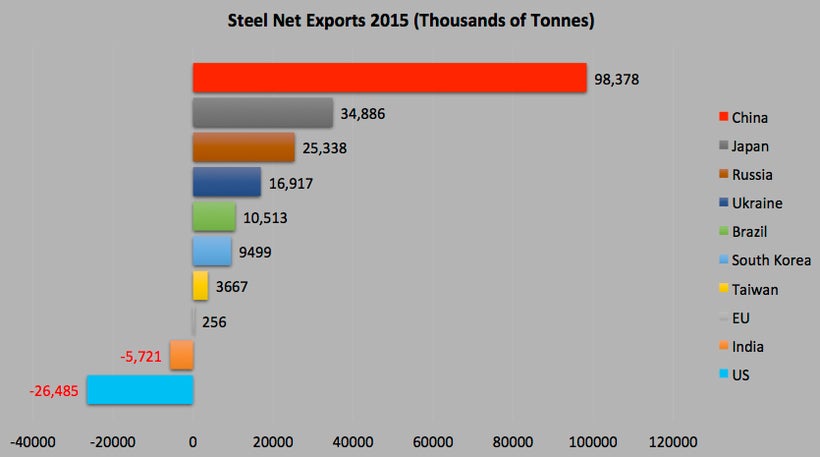

from prosperousamerica.org WORLD STEEL MARKETS BY THE NUMBERSBy Jeff Ferry, CPA Research Director Feb 28, 2018 "The pundits who declare ominously that we are on the brink of a trade war have it wrong. In fact, we are in the midst of a war for domination of the world steel market. And as a quick look at the numbers makes clear, so far we are losing. The World Steel Organization does a great job of assembling data for the worldwide steel industry. A quick look at recent steel history makes it clear to what extent China is dominating the industry and creating problems for other producers. The core problem for the steel industry is overproduction: the world is producing about 1,600 million tons of steel a year and only consumes about 1,100. As Figure 1 shows, the overproduction problem is entirely due to China’s huge increase in production. China’s 2016 steel production of 808 million tons is up 65% on its 2007 total. In fact, the Chinese government officially and publicly recognized that it was overproducing back in 2007, and has called on its own industry to begin cutting back production and retiring steel plants, especially the older, heavily polluting ones. Despite the fact that the Chinese government and related agencies support the industry with billions of dollars in subsidies, the Chinese industry did not heed the call. Instead, production continued to rise. Today, China produces more steel than the next nine steel-producing nations combined.  Figure 1: China now accounts for 50% of world steel production. As Figure 2 shows, many of the other top ten steel producers have reacted to the oversupply of steel by reducing production. Only India shows a large increase in recent years, and India consumes virtually all of its steel internally. The US has cut production by 20%, the largest production cut in this group (other than the Ukraine, which suffered invasion by Russia during the period). South Korea has raised production by 33% in the period, reflecting an economic strategy (neo-mercantilism) that is in some ways similar to that of China.  Figure 2: The rest of the top ten steel producers have mostly held production flat in this era of oversupply. US production fell by 20%. Figure 3 looks at the top countries in terms of net exports and net imports in 2016. Net exports is the total of exports minus the total of imports in that year. Because steel is so critical to so many other industries, most advanced nations want to ensure that their net imports do not get very high, so they always have the capability to meet their own needs, even in times of crisis. Some nations, especially the neo-mercantilists, want to build up large export businesses in steel. As Figure 3 shows, Japan, Russia, and the Ukraine all export more steel as a share of their domestic production than China. However all these countries have responded to the overproduction crisis (and the weak steel prices) by cutting back production in these years. Japan’s 2016 production was 13% below its 2007 level. China’s net exports of 94.5 million tons are more than the other four major net exporters combined. And China has not cut back production. On the contrary, China’s steel production has increased, and with a slump in its previously-booming construction industry, there is nowhere for the excess production to go but into the export market. Meanwhile, on the import side, there is only one advanced nation willing to accept a large volume of steel imports—the United States. The net importers just below the US on this list have little or no steel industries of their own and must import to meet the needs of their domestic industries. Vietnam has ambitious plans to build up its own steel industry, which is likely to remove it from the list of large steel importers. The major steel producers within the European Union—Germany, France, and Italy—all manage their markets carefully to keep net imports at very low levels. Size and success in the steel industry has little to do with comparative advantage, to use the concept often invoked by “free trade” economists with near-religious fervor. The main raw materials used to make steel are iron ore, coking coal, and scrap metal. China has no natural comparative advantage in any of these and must import them all. Labor costs are small in steel: 1 to 2 man-hours per ton—no more than 10% of the cost of a ton of steel. The “advantage” China has is a government willing to spend billions to support the growth of its steel industry. The disadvantage the US has is a government that takes a short-term view and seeks the cheapest price today and encourages its domestic industries to do the same, without regard for the long-term consequences of allowing its military and civilian economies to become dependent on foreign suppliers who cannot be counted on for either price or availability in the longer term. Figure 3: China leads the net exporters and the US the net importers. Source: Data from World Steel Organization. Calculations by CPA." |

|

|

|

Post by unlawflcombatnt on Mar 11, 2018 11:11:13 GMT -6

from prosperousamerica.org WHY WE NEED STEEL TARIFFSFebruary 28, 2018 By Jeff Ferry, CPA Research Director "The Department of Commerce report on steel imports and national security asks Americans a fundamental question: Are we going to defend the US steel industry from the decline caused by the growth of uneconomic foreign competition? Or, are we going to allow the industry to fade away and become dependent on other countries for this ubiquitous product, vital to our military and civilian economy? We believe the answer has to be an effort in favor of defending America’s steel industry. Too much is at stake. America’s national security depends on a reliable supply of steel. America’s infrastructure, much of it urgently in need of renewal, depends on steel. Great American industries, including automobiles, aerospace, and many others, depend on a reliable supply of high-quality, low-cost steel. Thousands of jobs also depend on the steel industry. Equally important, the international rule of law depends on the US taking a strong stand today. In the last nine years, China has increased its steel production 65% and now accounts for 50% of world production and 23% of world steel exports. Some believe it is the Chinese government’s deliberate intention to weaken the US steel industry; others say they are simply subsidizing their loss-making steel industry with billions of dollars of government money as a huge employment program, and taking advantage of the US market as the only major nation willing to accept large-scale imports. National Security The January report from the Commerce Department explains that the US military depends on steel for weapon systems, ships, planes, and land vehicles. Although critics have argued that only 3% of US steel production is required for defense needs, this ignores the broad range of types of steel needed by the military and the way a complex industry really works. As Commerce spells out in its report, the military needs not just thousands of tons of common steel plate, it also needs specialty steels including high-carbon forged steel, high-tensile strength steel, high-carbon steel laminate, steel forgings, and other steel alloys that deliver greater strength at lower weight than ordinary steel. All these steel variations can only be produced by a healthy commercial industry deriving the majority of its revenue from civilian customers. The report cites (Appendix H, pg. 3) two cases where the Defense Department (i.e. the US taxpayer) has had to provide funds to the industry to ensure a supply of specific steel variations: one for the high-purity, low-alloy, iron-based steel used in MRAP vehicles widely deployed in war zones to protect troops from mines, and another steel variation for Navy-grade, heavy-alloy steel plate used in submarines, helicopter landing decks, and other military vehicles. A robust steel industry is required to meet these needs. Yet despite the economic recovery since 2009, US steel production has declined, down 12% since 2012 to 78.5 million tons in 2016. The US has lost 11,000 steel jobs since 2012 to reach a new low of 81,400 employees, according to BLS data. Continued decline of the industry threatens our defense needs, including our ability to respond quickly in times of crisis. As the Commerce report (pg. 26) puts it: “A continued loss of viable commercial production capabilities and related skilled workforce will jeopardize the US steel industry’s ability to meet the full spectrum of defense requirements.” A healthy industry is also important for the civilian economy. Steel is one of the most widely used materials in the world. Innovations in steel capability often play a substantial role in new opportunities and the competitiveness of industries like automobile and aerospace production. The view that steel is a mature, unchanging, dirty “old” industry is a facile presumption of those who don’t understand modern manufacturing. Research and development plays a role in every manufacturing industry. Steel and steel alloys evolve and change. As the World Steel Association points out, 75% of the steels in use today did not exist 20 years ago. Thanks to technological progress, the Golden Gate Bridge, which required 83,000 tons of steel when it was built in 1937, could today be built with only half that amount of steel. Our largest steel company, Nucor, has developed an innovative technique, known as Castrip, to use rollers to produce steel sheet as thin as 1 millimeter directly from the steelmaking furnace. The process is cheaper, more space-efficient, and more energy-efficient. Imports and China Capacity (or plant) utilization is the most important barometer of the health of our steel industry. At 80% or higher plant utilization, the industry is healthy. Below that level, it struggles. Between 1990 and 2008, the industry was healthy, with utilization rates averaging around 85%. However, around the year 2000, China embarked on its monumental drive for economic growth. Chinese steel production has increased six-fold since 2000, rising from 127 million tons to last year’s 808 million tons. China now accounts for 50% of global production. Industry experts agree that global demand is only about 1,100-1,200 million tons, so some 400 million tons needs to be removed from the market to restore the world industry to health. China has recognized that it is overproducing. According to the Commerce report (Appendix L, pg. 4), the Chinese government has been urging its steelmakers to cut capacity at least since 2006, with little result. In a 2016 Reuters article, Shiheng Special Steel Group CEO Zhang Wuzong said the government’s plan to cut capacity by around 100 million tons was insufficient. “Getting rid of 100 million or 150 million isn’t any good—300 million or 400 million is more appropriate,” he told Reuters. Unusually outspoken for a Chinese executive, he went onto criticize the government’s planned $15 billion fund to take care of layoffs and debt write-offs for so-called “zombie” steel companies as insufficient to solve the problem. Speaking in early 2016, he forecast that Chinese steel production would fall by 40 million tons a year. Instead, in 2016, it rose by 4.5 million tons. China now produces more steel than the US, Japan, Russia, and the European Union combined. This excess supply has led to a surge of imports into the US. In spite of over 100 individual tariffs on specific types of steel from specific countries, imports took 33.8% of US consumption last year according to Commerce Department estimates, up from an average of 30% over the preceding five years. Excess supply depresses prices in the US market, causing the industry to shrink. According to the Commerce Department report (pgs. 33-34), 10 steelmaking facilities have closed since 2000, in Ohio, Indiana, West Virginia, Delaware, Maryland, South Carolina, Alabama, and Oklahoma. Last year, ArcelorMittal announced the closure of a steel mill in Conshohocken, Pennsylvania. That list does not include other steel mills that have been “temporarily” closed while awaiting an upturn in the market—which may or may not come. The net result for American steelmakers can be seen in Figure 1. The industry has been unable to earn a decent profit since 2008. The fundamentals of a capital-intensive business like steel require companies to earn a return well in excess of their cost of capital; otherwise they are not creating value and shareholders will not provide the funds necessary to maintain and renew the heavy capital investment required. A Coalition for a Prosperous America (CPA) analysis of the last nine years of steel industry financial data shows that the industry’s return on invested capital (the broadest measure of profitability) ranged from 5.65% for industry leader Nucor to a negative 11.76% for the struggling industry laggard US Steel. Yet the cost of capital for these companies ranged from 11.27% for Nucor to 22.37% for US Steel. Despite an uptick in profits in 2017 (partly driven by anticipation of tariffs), these companies are not generating enough profit to attract the capital they need to invest in their own businesses. Further shrinkage and decline would be inevitable without a remedy. Figure 1: US steel companies have suffered losses or negligible profits since 2009. The Commerce Department has recommended three possible remedies to President Trump (see pg. 8). •“Alternative 1A” calls for an import quota requiring a 37% reduction on 2017 levels for shipments into the US for each country sending steel. •“Alternative 1B” calls for a global 24% tariff on all steel imports into the US. •“Alternative 2” is for a 53% tariff on steel from those nations that are not close allies of the US, including Brazil, China, South Korea, Russia, Vietnam, and several others. Canada and the European Union are notably absent from this list. All three alternatives are aimed at restoring the US steel industry to plant utilization levels of 80%. Alternative 2 has been designed to meet international considerations. In its Feb. 23rd memo to Commerce Secretary Wilbur Ross, the Defense Department said it agreed that steel imports were endangering national security but added that it was concerned about the impact of action against steel from our allies. It asked Commerce to “create incentives for trade partners to work with the US on addressing the underlying issue of Chinese transshipment.” The idea of imposing steep tariffs only on certain nations could create an incentive for nations to resist Chinese transshipment. It also could mark a start for building an international coalition to pressure China to cut back on its production and exports. International conflict over steel can only be resolved if China is convinced that it cannot export its overproduction to the rest of the world. Our allies need to move away from the view that they can be unharmed bystanders as the bulk of overproduction ends up in the US. The entire international community has a shared interest in compelling China to act as a good global citizen instead of a rogue nation that pays lip service to “free trade” while relentlessly expanding its civilian and military capabilities. The Commerce Department’s tariff recommendations have been criticized by many “free trade” economists. They claim that tariffs will raise prices, hit consumers, and reduce American gross domestic product. They fail to recognize that American consumers are also American producers. While a tariff on steel will lead to small price increases in steel-using goods, it will also lead to more jobs and economic growth in the steel industry. Over time, that growth will spread to other industries. We know from bitter experience that the majority of folks pushed out of manufacturing jobs end up working in service industries with lower pay and worse benefits. That’s if they can find any work at all. With its critical importance to so much of the military and civilian economy, steel is an excellent place to begin a major pushback in favor of good jobs, US productive capacity, economic rebuilding, and the struggle for a more realistic international dialogue on economic relations." |

|

|

|

Post by unlawflcombatnt on Mar 11, 2018 10:07:31 GMT -6

from freedomsphoenix.com www.freedomsphoenix.com/Opinion/236239-2018-03-11-11-nations-sign-tpp-deal.htm11 Nations Sign TPP DealMarch 11, 2018 by Stephen Lendman "Signatory countries include Australia, Brunei, Canada, Chile, Japan, Malaysia, New Zealand, Peru, Singapore and Vietnam - America withdrew, China excluded. The Electronic Frontier Foundation earlier called TPP "a secretive, multinational trade agreement that threatened to extend restrictive intellectual property (IP) laws across the globe and rewrite international rules on its enforcement." It's NAFTA on steroids, a stealth corporate coup d'etat, a giveaway to corporate predators, a neoliberal ripoff, a freedom and ecosystem destroying nightmare. Corporate predators and lobbyists representing them wrote the agreement, exclusively benefitting business interests at the expense of public health and welfare. On Thursday in Santiago, Chile, 11 nations signed the renamed Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). Provisions lobbied for by Big Pharma were excluded from the deal, subject to possible later inclusion. Americans at least temporarily were saved from a deeply flawed deal, grievously harming consumers in all signatory countries. CPTPP revisions leave most of its harmful provisions intact - including the infamous investor-state dispute settlement ( ISDS) system. It lets corporate predators sue governments before a rigged panel of 3 corporate lawyers for virtually unlimited compensation from taxpayers on what they claim violates their rights - including alleged loss of "expected future profits." Rulings in their favor can be gotten by claiming laws protecting public health or ecosanity violate their trade agreement rights. Rulings are not subject to appeal. If a nation refuses to pay, the suing corporation can seize its assets to obtain compensation. ISDS amounts to extrajudicial rigging, occurring outside of a nation's courts. It incentivizes offshoring of jobs by providing special privileges and rights for firms relocating operations abroad.A global race to the bottom is facilitated. Signing on to CPTPP would have greatly increased US exposure to ISDS attacks - by empowering corporate predators in all signatory countries. Why any nation would agree to abandon consumer rights, ecosanity, and greatly increased vulnerability to ISDS attacks is incomprehensible. To its credit, the Trump administration wants ISDS rolled back in ongoing NAFTA renegotiations. Corporate lobbyists are going all-out to block this proposal - aided by 11 CPTPP nations agreeing to include it in their agreement. In America, unions, consumer and environmental groups, Nobel laureate economist Joseph Stiglitz, even Supreme Court Chief Justice John Roberts oppose ISDS. The most significant provisions of CPTPP, NAFTA and similar deals are investment rules, not trade-related ones. They're about maximizing corporate profits at the expense of public health, safety and ecosanity." |

|

|

|

Post by unlawflcombatnt on Mar 10, 2018 13:03:46 GMT -6

from David Stockman's Contra Corner davidstockmanscontracorner.com/its-not-bad-trade-deals-its-bad-money-part-2/It's Not Bad Trade Deals--It's Bad Money, Part 2March 6, 2018 By David Stockman "In Part 1 we made it clear that the Donald is right about the horrific results of US trade since the 1970s, and that the Keynesian "free traders" of both the saltwater (Harvard) and freshwater (Chicago) schools of monetary central planning have their heads buried far deeper in the sand than does even the orange comb-over with his bombastic affection for 17th century mercantilism. The fact is, you do not get an $810 billion trade deficit and a 66% ratio of exports ($1.55 trillion) to imports ($2.36 trillion), as the US did in 2017, on a level playing field. And most especially, an honest free market would never generate an unbroken and deepening string of trade deficits over the last 43 years running, which cumulate to the staggering sum of $15 trillion. Better than anything else, those baleful trade numbers explain why industrial America has been hollowed-out and off-shored, and why vast stretches of Flyover America have been left to flounder in economic malaise and decline. But two things are absolutely clear about the "why" of this $15 trillion calamity. To wit, it was not caused by some mysterious loss of capitalist enterprise and energy on America's main street economy since 1975. Nor was it caused---c0ntrary to the Donald's simple-minded blather---by bad trade deals and stupid people at the USTR and Commerce Department. After all, American capitalism produced modest trade surpluses every year between 1895 and 1975. Yet it has not lost its mojo during the 43 years of massive trade deficits since then. In fact, the explosion of technological advance in Silicon Valley and on-line business enterprise from coast-to-coast suggests more nearly the opposite. Likewise, the basic framework of global commerce and trade deals under the WTO and other multi-lateral arrangements was established in the immediate post-war years and was well embedded when the US ran trade surpluses in the 1950s and 1960s. Those healthy post-war US trade surpluses, in fact, were consistent with the historical scheme of things during the golden era of industrial growth between 1870 and 1914. During that era of gold standard-based global commerce, Great Britain, France and the US (after the mid-1890s) tended to run trade surpluses owing to their advanced technology, industry and productivity, while exporting capital to less developed economies around the world. That's also what the US did during the halcyon economic times of the 1950s and 1960s. What changed dramatically after 1975, however, is the monetary regime, and with it the regulator of both central bank policy and the resulting expansion rate of global credit. In a word, Tricky Dick's ash-canning of the Bretton Woods gold exchange standard removed the essential flywheel that kept global trade balanced and sustainable. Thus, without a disciplinary mechanism independent of and external to the central banks, trade and current account imbalances among countries never needed to be "settled" via gains and losses in the reserve asset (gold or gold-linked dollars). Stated differently, the destruction of Bretton Woods allowed domestic monetary policies to escape the financial discipline that automatically resulted from reserve asset movements. That is, trade deficits caused the loss of gold, domestic deflation and an eventual rebalancing of trade. At the same time, the prolonged accumulation of reserve assets owing to persistent current account surpluses generated the opposite---- domestic credit expansion, price and wage inflation and an eventual reduction in those surpluses. Needless to say, as the issuer of the gold-linked "reserve currency" under Bretton Woods, the Fed was the first to break jail when it was deep-sixed in 1971-1973. At the time, the freshwater Keynesians led by Milton Friedman and his errand boy in the Nixon/Ford White House, labor economics professor George Schultz, said there was nothing to sweat over. That's because the free market would purportedly generate the "correct" exchange rate between the dollar and D-mark, franc, yen etc; and then these market-determined FX rates, in turn, would regulate the flow of trade and capital. Very simple. Adam Smith's unseen hand all over again. In fact, not in a million years! The giant skunk in the woodpile actually smelled of state monetary emissions or what was called the "Dirty Float". The latter threw everything into a cocked hat because unlike under Bretton Woods or the classic pre-1914 gold standard, the new regime of unanchored money allowed governments to hijack their central banks and to use them as instruments of mercantilist trade promotion and Keynesian domestic macro-economic management. To be sure, it took some time for traditional central bankers to realize that they had been unshackled. For example, during the final years of his tenure (1970-1978) Arthur Burns caused a pretty nasty recession in 1975 trying to reclaim his reputation for monetary probity after meekly capitulating to Nixon in fueling the 1972 election year boom that finally destroyed the remnants of Bretton Woods entirely. At length, however, Alan Greenspan inaugurated the era of Bubble Finance in 1987, and the die was cast. During his 19-years at the helm of the Fed, Greenspan massively inflated the Fed's balance sheet (from $200 billion to $700 billion) and the cost structure of the US economy at a time when the mobilization of cheap labor from the rice paddies of China and east Asia demanded exactly the opposite policy. That is, a policy of Fed balance sheet shrinkage and domestic deflation. Accordingly, a destructive pattern of reciprocating monetary inflation within the global convoy of central banks was set in motion: The Fed inflated and they inflated in a continuous loop. So doing, the central banks of the world locked-in a permanent condition of unbalanced trade. The latter originated in the Fed's flood of excess dollars into the international financial system in the 1990s and thereafter. This, in turn, caused central banks in Asia, much of the EM, the petro-states and sometimes Europe, too, to buy dollars and sequester them in US treasury paper (and GSE securities). This Dirty Float was undertaken, of course, to stop exchange rate appreciation and to further mercantilist trade and export-based domestic economic policies in China, South Korea, Japan and elsewhere. But what is also did was enable a sustained debt-based consumption boom in the US that was not earned by current production. The excess of US consumption over production, which showed up in the continuous US current account deficits, was effectively borrowed from central banks (and often their domestic investors). That happened because these central banks, in effect, were willing to swap the labor of their people and the endowments of their natural resources for US debt paper rather than face rising exchange rates and temporary headwinds to their mercantilist growth policies. In short, the $15 trillion plague of US trade deficits since 1975 is the bastard step-child of the Dirty Float maintained in Asia and elsewhere as a defense against the Fed's profligate money printing. Over time, it morphed into a back-door form of de facto export subsidies that would otherwise be illegal under the current WTO rules of global trade. So when the Donald declaims that pointy-head bureaucrats are the culprits behind the US trade disaster, the part he gets wrong is the names. To wit, the real malefactors of trade stupidity are named Alan (Greenspan), Ben (Bernanke) and the Two Janets (Yellen and Powell). America is losing it shirt in trade owing to their bad money, not bad deals cut at the Commerce Department or Foggy Bottom (State). As we indicated in Part 1, Keynesian monetary central planning has it upside down. It seeks to inflate domestic prices, wages and costs at 2% per year (or more if correctly measured) in a world teeming with cheap labor---when a regime of honest money would have generated deflationary adjustments designed to keep American industry competitive. So doing, it would have denied much of the incentive for and rationalization of the Dirty Float. Indeed, had the US maintained a regime of high interest rates, low consumption and enhanced levels of savings and investments in order to maintain sustainable equilibrium with the rest of the world after 1990, it is doubtful that the Dirty Float would have become massive, near-universal and quasi-permanent. That's because in a world of hard dollars, money-printing, low-interest rate central banks would have caused soaring domestic inflation and destructive capital flight. The People's Printing Press of China, for example, would have been caught short decades ago. Indeed, in a world of hard money, the egregious 9X expansion of its balance sheet, which fueled the Red Ponzi's runaway capital spending mania, could never have happened. China Central Bank Balance Sheet Needless to say, China was not the only Dirty Float malefactor. The Japanese have been far worse. Since 1990 the balance sheet of the BOJ has expanded by 20X, thereby insuring that the yen exchange rate versus the dollar remained uneconomically low, and that Japan's egregiously mercantilist trade policy would remain undisturbed by honest yen selling prices for its goods sold on the international markets. Japan Central Bank Balance Sheet The story is much the same throughout the lands of cheap labor and/or Dirty Floats. As we pointed out in Part 1, Mexico's exchange rate has fallen from 4:1 at the time of NAFTA's inception to 19:1 at present. Therefore, it wasn't a bad trade deal that caused the current $71 billion US trade deficit with Mexico; it was bad money. After all, about the only thing more profligate than the Fed's 20X balance sheet growth since 1990, is the 40X expansion by the Mexican central bank. Mexico Central Bank Balance Sheet Not surprisingly, it turns out that the land of Dirty Floats accounts for the 90% of the $810 billion trade deficit incurred by the US last year. That's right. The overall trade problem is that the US exported only $1.55 trillion of goods, materials and energy last year, or just 66% of the $2.36 trillion of merchandise that it imported. Yet just 10 countries account for nearly all of that huge imbalance. These countries are China, Vietnam, Mexico, Japan, Germany, South Korea, Taiwan, Malaysia, Thailand and India. As a group, these countries bought just $627 billion of US exports, while sending $1.35 trillion of imports to the US. Accordingly, the combined deficit was $725 billion, representing 90% of the total US trade deficit. Moreover, the US export-to-import ratio was just 46% for the 10 countries as a whole, and far worse among the most egregious Dirty Floaters. Thus, China's $130 billion of exports from the US represented just 26% of its $506 billion of imports to the US. In the case of Vietnam, the export ratio was only 17% ($8 billion of US exports versus $46 billion of imports to the US). In Part 3 we will explain why the massive trade deficit with these 10 countries is largely a product of the Eccles Building and the Dirty Floats it has fostered among these mercantilist countries. And that's true even in the case of Germany, which sent $118 billion of goods to the US last year compared to US exports to Germany of just $53 billion. The latter amounted to only 45% of imports from Germany, and resulted in a staggering $65 billion trade deficit with the US. Were Germany not a part of the EU, the exchange rate for the D-mark would be far higher than the euro's, and Germany's trade surplus with the US (and the rest of the world) would be far smaller. In effect, the mad money printer, Mario Draghi, has actually effected a hidden Dirty Float that has been a tremendous windfall to German industry. Euro Area Central Bank Balance Sheet By contrast, the US trade accounts are functionally in balance with the entire rest of the world. As we showed in Part 1, for instance, US exports to Canada are 95% of imports from our giant trading partner to the north. Indeed, for the rest-of-the-world as a whole, the trade numbers are quite striking and sustainable. Overall US exports to these destinations amounted to $924 billion during 2017 compared to $1.0 trillion of imports from these suppliers. Accordingly, exports amounted to 92% of imports, and the total $85 billion deficit at just 4% of two-way trade (nearly $2 trillion) was close enough to zero for big picture purposes. Needless to say, dumb trade negotiators did not produce a healthy balance within half of the $3.9 trillion of total US two-way trade, and a massive, disastrous deficit within the other half among the top ten Dirty Float countries itemized above. As we said, we are dealing here with bad money, but, alas, neither the protectionist inside the White House nor the free traders shouting at the front gate have explained that to the Donald. Ironically, the only way out of the Donald's crude protectionism is a return to sound money. Yet that's the last thing the Wall Street and Fortune 500 "free-traders" are about to embrace, as we will elaborate in Part 3. In effect, they wish to perpetuate a regime that swaps American labor and living standard in Flyover America for massively inflated financial asset prices on Wall Street. That is, for unspeakable windfalls to the top 1% and 10% which own 45% and 85% of financial assets, respectively. No wonder the people out there in Rust Belt America are mad!" And it's also no wonder they put a mad man in the Oval Office to attack a system that truly is "rigged" against them." |

|

|

|

Post by unlawflcombatnt on Mar 10, 2018 12:56:20 GMT -6