|

|

Post by jeffolie on Apr 23, 2013 17:11:03 GMT -6

China death spiral, April 2013 Oligarchs 2017

RISE OF THE CHINESE OLIGARCHS 2017

I predict China will collapse when America declines into an economic and political bottom period by 2016, follow the USSR path into a 'democratic govt' featuring elections with the wealth ending up in the hands of 'oligarchs' similar to what happened in the sucessor Russia. China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016

Another source of China's decline continues to grow: higher labor costs and inflation

|

|

|

|

Post by jeffolie on May 1, 2013 15:56:31 GMT -6

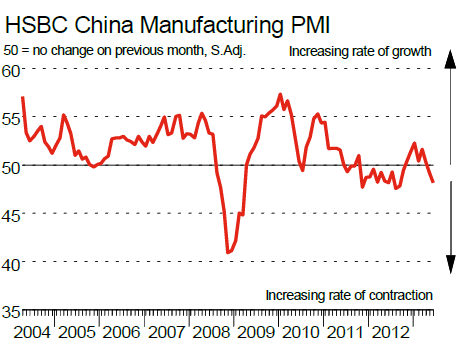

China Manufacturing Gauge Signals Slowdown Persisting: Economy By Bloomberg News - May 1, 2013 China’s manufacturing expanded at a weaker pace in April in a sign that the slowdown in the world’s second-largest economy is extending into the second quarter. The Purchasing Managers’ Index was at 50.6, the National Bureau of Statistics and China Federation of Logistics and Purchasing said today in Beijing. That compared with the 50.7 median forecast of 31 analysts in a Bloomberg News survey and a March reading of 50.9. Readings above 50 signal expansion. Australian stocks fell and copper declined as the report increased concern that demand from China for commodities will slow. The figures add to data showing growth in industrial companies’ profits decelerated in March and Aluminum Corp. of China Ltd., the nation’s biggest producer of the lightweight metal, having a sixth straight quarterly loss. “The debate about growth -- and just how much we should worry about this weak recovery -- is likely to build in Beijing,” said Stephen Green, head of Greater China research at Standard Chartered Plc in Hong Kong. Today’s number is “disappointing,” he said in an e-mail. A private survey of China manufacturing by HSBC Holdings Plc and Markit Economics had a preliminary reading of 50.5 for April, down from the final level of 51.6 for March, a report showed last month. The final figure will be released tomorrow. Signs of slowing expansion are spreading across Asia. Japanese and South Korean industrial output was less than estimates in March and Taiwan’s first-quarter growth was half the forecast pace as weakness in global demand limits recoveries in Asian economies, reports showed yesterday. Orders Slow A gauge of new orders in China manufacturing fell to 51.7 from 52.3 in March, while an index of new export orders dropped to 48.6 from 50.9 and the reading on inventories of finished goods declined to 47.7 from 50.2, according to today’s data, based on a survey of businesses. Chinese stocks fell to a four-month low before the three- day Labor Day holiday that ends today on concern that a slowdown will drag on earnings. Growth risks include weakness in export demand, property-market overheating, a surge in so-called shadow banking and the damping of consumption by President Xi Jinping’s campaign to rein in official spending. The benchmark Shanghai Composite Index (SHCOMP) is down 11 percent from this year’s Feb. 6 high. The MSCI Asia Pacific Index of stocks fell 0.5 percent at 5:42 p.m. in Tokyo. Australia’s S&P/ASX 200 Index dropped 0.5 percent at the close in Sydney, while copper for delivery in three months declined as much as 1.7 percent to $6,936.50 a metric ton on the London Metal Exchange and traded at $6,958.50 by 4:45 p.m. in Singapore. Sustain Recovery The decline in April’s index shows that the “foundation of an economic stabilization is still not solid,” Zhang Liqun, a researcher with the Development Research Center, an agency advising China’s cabinet, said in a statement. “The economic growth rate may fall slightly in the future, and China needs to stabilize domestic demand to make the economic recovery more sustainable.” The world’s second-biggest economy expanded 7.7 percent in the first quarter, less than analysts’ forecasts and below the 7.9 percent pace in the final three months of last year. Growth in industrial companies’ profits slowed in March, an April 27 report showed. The fourth quarter’s growth rebound “was an old fashioned one led by fast implementation of fiscal programs and accelerated investment,” said Liu Li-Gang, head of Greater China economics at Australia & New Zealand Banking Group Ltd. in Hong Kong. “Now the momentum has petered off as shown by recent slowing investment growth.” Loosen Controls China’s new government “must initiate a new round of reform programs to restart the sputtering economy” including plans for urbanization, reducing service-industry taxes and loosening controls on interest rates, Liu said in an e-mail. Separately today, South Korean exports rose less than forecast in April, climbing 0.4 percent from a year earlier, while imports declined 0.5 percent, government data showed. In Indonesia, inflation slowed to 5.57 percent in April from a year earlier. In the U.S., companies probably added 150,000 workers in April, less than the 158,000 recorded in March, economists forecast ahead of figures due today from the Roseland, New Jersey-based ADP Research Institute. In January, the Chinese federation increased the number of companies in its survey to 3,000 from 820 and reclassified the industries covered into 21 groups from 31. It hasn’t given a further breakdown of respondents. A purchasing managers’ index for large companies fell 0.4 point from March to 51, while a gauge for mid-sized enterprises rose 0.4 to 50.7 and a reading for small businesses dropped 1.7 to 47.6, according to the statistics bureau. “China needs to cement its domestic economic growth momentum and guard against potential risks in financial sectors,” the Politburo Standing Committee said in an April 25 statement. www.bloomberg.com/news/2013-05-01/china-manufacturing-expands-at-weaker-pace-after-economy-slows.html |

|

|

|

Post by jeffolie on May 6, 2013 11:19:35 GMT -6

China death spiral, April 2013 Oligarchs 2017 RISE OF THE CHINESE OLIGARCHS 2017 my jeffolie view: China will collapse when America declines into an economic and political bottom period by 2016, follow the USSR path into a 'democratic govt' featuring elections with the wealth ending up in the hands of 'oligarchs' similar to what happened in the sucessor Russia. China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016 Another source of China's decline continues to grow: higher labor costs and inflation ======================== May 05, 2013 China Services PMI Slows to Marginal Rate of Growth Fresh on the heels of a report that shows China Manufacturing PMI barely Above Contraction comes news the Chinese service sector is following suit. The Markit China Composite PMI shows Activity growth eases across both the manufacturing and service sectors in April. Key Points •Composite data signals slower activity and new business growth in April •Total employment falls for first time since last October •Both input prices and output charges decline at the composite level HSBC China Composite PMI data (which covers both manufacturing and services) signalled an expansion of output for the eighth consecutive month in April. However, the HSBC China Composite Output Index signalled only a marginal rate of growth, posting at 51.1. This was down from 53.5 in March, suggesting that the rate of expansion was the weakest since last October. Behind the weaker expansion of total output was a slower rate of new order growth in April. Both the manufacturing and service sector posted modest rates of expansion that were weaker than in March. Overall, new order growth at the composite level was the slowest in seven months. Backlogs of work decreased at service providers, but rose at manufacturers in April. That said, the rates of change were marginal in both sectors. At the composite level, backlogs of work declined for the third month in a row, though only slightly. Employment levels decreased across both the manufacturing and service sectors in April. Although the rates of job shedding were only marginal in both cases, it was nonetheless the first time service providers had cut their staff numbers since January 2009 and was the first reduction in manufacturing payroll numbers since last November. Consequently, employment at the composite level fell slightly in April. Signs that the global economy has stalled, if not in outright recession (I believe the latter) continue to mount. Mike "Mish" Shedlock globaleconomicanalysis.blogspot.com/2013/05/china-services-pmi-slows-to-marginal.html |

|

|

|

Post by jeffolie on May 6, 2013 11:31:50 GMT -6

China services growth slows sharply, adds to recovery risk May 6, 2013 BEIJING (Reuters) - Growth in China's services sector slowed sharply in April to its lowest point since August 2011, a private sector survey showed on Monday - fresh evidence of rising risks to a revival in the world's No.2 economy. The HSBC services Purchasing Managers' Index (PMI) fell to 51.1 in April from 54.3 in March, with new order expansion the slowest in 20 months and staffing levels in the service sector decreasing for the first time since January 2009. Two separate PMIs last week had already shown that China's manufacturing sector growth slowed, With the weakness spreading to services, which make up almost half of gross domestic product, the risk to the recovery may be increasing. "The weak HSBC service PMI figure provides further evidence of a slowdown not only in the factory sector but also in the service sector," said Zhang Zhiwei, chief China economist at Nomura Securities in Hong Kong. "This confirms our worries about insufficient growth momentum in the economy, which we expect to slow to 7.5 percent in the second quarter." The HSBC services PMI follows a similar survey by China's National Bureau of Statistics, which found non-manufacturing activity eased to 54.5 from 55.6. The official PMI is more weighted towards large state-owned firms. Readings above 50 indicate activity in the sector is growing, while those below 50 indicate it is contracting. The HSBC survey showed that the sub-index measuring new business orders dropped sharply to a 20-month low of 51.5 in April, with only 15 percent of survey respondents reporting an increased volume of new orders that month, HSBC said. "This started to bite employment growth. All these are likely to add some risk to China's growth in 2Q, as there's still a bumpy road towards sustaining growth recovery," said HSBC's China chief economist Qu Hongbin. The employment sub-index decreased to 49.6 in April, the first net reduction in staff numbers since January 2009, although HSBC said job losses were marginal, partially caused by firms down-sizing and employee resignations. Employment is a decisive factor shaping government thinking because it is crucial for social stability. The services sector accounted for 46 percent of China's gross domestic product in 2012, as big as the country's better-known manufacturing industry. China's economic growth unexpectedly stumbled in the first quarter, slipping to 7.7 percent versus 7.9 percent in the previous three month period, as factory output and investment slowed. The government has set a 2013 growth target of 7.5 percent, a level Beijing deems sufficient for job creation while providing some room to reform to the economy. Any more weak data could spark a policy response. "The risk of slower growth is rising, the Chinese government will probably take actions after April data come out," said Jianguang Shen, chief China economist of Mizuho Securities Asia in Hong Kong. "I see an increasing possibility for China to cut interest rates, but not likely any time in the near future, as housing inflation is a constraint."However a Reuters poll last month found that China's central bank is expected to keep the benchmark one-year bank lending rate at 6 percent and the one-year bank deposit rate at 3 percent through 2013, as well as holding banks' reserve requirement ratios (RRR) steady. www.reuters.com/article/2013/05/06/us-china-economy-services-pmi-idUSBRE94501020130506

|

|

|

|

Post by jeffolie on May 23, 2013 7:19:52 GMT -6

China May Factory Output Contracts in Test for Premier: Economy By Bloomberg News - May 23, 2013 China’s manufacturing is contracting in May for the first time in seven months, adding to signs that economic growth is losing steam for a second quarter. The preliminary reading of 49.6 for a Purchasing Managers’ Index (EC11FLAS) released today by HSBC Holdings Plc and Markit Economics compares with a final 50.4 for April and the 50.4 median estimate in a Bloomberg News survey. A reading above 50 indicates expansion. A separate Markit index (SHCOMP) for euro-area services and factory output increased more than forecast. Asian stocks slumped after the data, which may test the new government’s commitment to tolerate slower growth after Premier Li Keqiang last week signaled reluctance to add stimulus. Investors soured on China’s outlook in a Bloomberg global poll this month, with the share of respondents who see the economy deteriorating doubling from January. “The slowdown is really bad,” said Ken Peng, a BNP Paribas SA economist based in Beijing. “It’s a big probability now that China’s GDP growth rate in the second quarter will be lower than in the first quarter,” he said, referring to gross domestic product. The MSCI Asia Pacific Index of stocks fell 3.2 percent as of 5:34 p.m. in Tokyo, headed for the biggest loss since November 2011, as Japan’s Topix Index closed down 6.9 percent, the most since the aftermath of the Fukushima disaster in March 2011. The Australian dollar and copper also declined. The benchmark Shanghai Composite Index of stocks fell 1.2 percent at the close, the largest drop in a month. Euro Recession A euro-area composite index based on a survey of purchasing managers in services and manufacturing rose to 47.7 from 46.9 in April, London-based Markit said today, adding to signs the currency union is beginning to emerge from its record-long recession. The manufacturing and services gauges improved to 47.8 and 47.5, respectively, both three-month highs. Still, the composite index has been below 50, indicating contraction, for 16 consecutive months. The European Central Bank, which cut its benchmark interest rate to a record low of 0.5 percent this month, forecasts the euro-area economy will shrink 0.5 percent in 2013. “The euro zone’s second recession in five years looks set to drag on into a seventh successive quarter,” Markit’s chief economist, Chris Williamson, said in today’s report. “The ECB’s quarter-point cut in interest rates seems to have done little to inspire confidence that the economy will start to pick up again.” U.S. Manufacturing Elsewhere in Europe, Britain’s economy resumed growth in the first quarter as companies built up stocks and consumer spending increased, offsetting a drop in exports. Gross domestic product rose 0.3 percent in the period. Markit’s U.S. manufacturing index probably fell to 51.2 in May from 52.1 a month earlier, according to the median of 13 economists’ estimates in a Bloomberg survey before a report later today. China’s growth unexpectedly slowed to 7.7 percent in the first quarter while remaining above the government’s full-year target of 7.5 percent. Data earlier this month on fixed-asset investment and factory production missed forecasts and gauges of manufacturing and service industries declined. The economy expanded 7.8 percent in 2012, the slowest pace in 13 years. Second-quarter growth was projected at 7.8 percent, based on the median estimate in a Bloomberg News survey conducted from May 16 to May 21, down from last month’s 8 percent forecast. ‘External Headwinds’ HSBC will release the final PMI reading on June 3. The National Bureau of Statistics and China Federation of Logistics and Purchasing will release their own PMI survey, with a bigger sample size, on June 1. The official PMI in April was 50.6, down from 50.9 in March. The preliminary, or flash PMI is based on about 85 percent to 90 percent of responses from more than 420 manufacturers. Today’s data reflect “slower domestic demand and ongoing external headwinds,” Qu Hongbin, HSBC’s Hong Kong-based chief China economist, said in a statement. Signs of labor-market slack “call for more policy support,” Qu said. “Beijing still has fiscal ammunition to do so.” A gauge of output showed a preliminary reading of 51 for May, down from 51.1 in April, according to HSBC. “We disagree with HSBC’s call for firing fiscal bullets” because it’s not in line with the new leadership’s policy, said Steve Wang, chief China economist in Hong Kong for Reorient Financial Markets Ltd. Output is still expanding and an index of export orders improved, Wang said. Subway Projects Previously released data showed industrial production rose 9.3 percent in April from a year earlier, below the median analyst estimate of 9.4 percent in a Bloomberg News survey. Fixed-asset investment excluding rural areas rose 20.6 percent in the first four months of the year, compared with forecasts for 21 percent. The National Development and Reform Commission, China’s top economic-planning agency, in April approved 54.6 billion yuan ($8.9 billion) of subway projects in four cities, according to statements posted on the commission’s website. UBS AG this week cut its economic-growth forecast to 7.7 percent from 8 percent for this year, joining Goldman Sachs Group Inc., Royal Bank of Scotland Group Plc and JPMorgan Chase & Co. in reducing estimates for 2013 expansion. At the same time, economists have forecast that the People’s Bank of China is more likely to raise interest rates than cut them in the coming year. Eight of 15 analysts surveyed by Bloomberg News earlier this month project an increase in the benchmark deposit rate by the end of June 2014, compared with two who see a reduction. ‘No Sign’ JPMorgan Chase & Co., among those projecting an interest-rate increase, said in a note today that “there is no sign that the new government will introduce new pro-growth measures in the very near term despite the weak economic data.” Iron ore slumped into a bear market last week on concern that slowing economic growth in China, the world’s biggest buyer, will hurt the outlook for demand. Prices will decline as supplies expand over the long term, Alan Chirgwin, general manager of iron ore marketing at Australia’s BHP Billiton Ltd. (BHP), the largest mining company, said May 8. www.bloomberg.com/news/2013-05-23/china-manufacturing-contracts-for-first-time-in-seven-months.html

|

|

|

|

Post by jeffolie on May 25, 2013 17:58:52 GMT -6

Scottish economic history cycles Hugh Hendry: God is dead, China will followHugh Hendry 21 minutes 2000 to 2003 stock market crash … mean reversion mid point 2002 started gold hedge fund , 2:30 minutes into the video: 3:26 historic 2003 … mean reversion mid point … existentialist: No rules now … god is dead … 4:05 positions self outside the system, creates his own idea looking a trends 2003 the real economy stopped going down from the tech crash, creating an oasis in the real economy and 4:58 he bought copper refinery in Desseldorf to play China from the real economy no longer going down Hugh Hendry’s hedge fund make 50% on it’s gold 5:35 2006, Became a Treasury bond advocate, bug because gold could not reach very high levels as thought … 6:55 CB policy makers in 2006 would want to avoid high inflation … 7:30 to avoid hyperinflation 7:35 required a Lehman shock in order to take FED rates down to zero generating 3 $ Trillion of money printing … 7:54 minutes: Hugh Hendry’s hedge fund make 50% on it’s Treasury bonds 8:15 minutes: Hugh Hendry’s view now on creditor nations … going well now as a point 8:41 ‘ death spiral of mercantilism ’ the Asian nations Achilles' heel as shorting their currencies 9:29 their claim to fame is being cheap, cheap labor, cheap currencies, using foreign exchange interventions 9:46 creating the ‘short’ China has $3T plus Japan’s non Yen assets as 55% are another $3T leading to Hugh Hendry’s fear 10:00 is a ‘short squeeze’ … 10:36 perhaps the Yen goes to 50-60 to the Dollar then what happens? Hugh Hendry’s view that $3T has not yet triggered inflation, a fiquire that might do it, inflation, 11:18 … 12:20 Japan on the verge, Sharp verge of bankruptcy ,,, if move into the 12:31 50’s 60’s then Japan would be bust, revolution but the paradox is something profoundly bad must happen 12:47 then you want to be SHORT JBDs you do not survive the journey 12:53 13:23 China ‘had to beat the number’ like star stocks on wall street, … 13:55 hitting 10% GDP growth with assisted building of empty buildings, airports, etc … 14:50 China will bridge the garden variety recession by going forward even if at the end China is flagging, tried, 15:00 even if China gets a degree of inflation, that is OK, it might pass the batton, 15:23 China will again take over the world with export prowess idea is being challenged with the 15:30 absence of a sustained recovery … the bet the 15:50 Chinese made in 2009 could become unstuck … China now operationally and financially over leveraged for 16:00 unproductive investments now 16:06 having ‘double jeopardy’ if you will without a world recovery then Hugh Hendry fearful of the events that could become the Chinese 16:18 … don’t tell me they will sell their US Treasuries, they are not an asset 16:23 if sell then the Chinese renminbi goes higher, higher, higher, the little companies that export go bust … 16:45 the poison that would extenuate further … the1920s UK roadmap: 8% GGDP fall, US fell 23%, … 17:21 China might contract 23% 18:00 Can China shift to a demand driven economy …. : Hugh Hendry’s view that is no easy solution because Japan changed over 20 years of zero growth … 19:00 : Hugh Hendry’s view gold idea he owns 19:13 gold along with short the GOLD MINING equities 19:55 there is no rational for gold mining, it is as close as you get for insanity … : Hugh Hendry’s view: no prediction on gold prices …. Agnostic www.ritholtz.com/blog/Hugh Hendry: Investing Amidst Crashes, China & Speculators by Barry Ritholtz - May 25th, 2013, 6:00am Hugh Hendry, of Eclectica Asset Management, takes the long view on investing at The Economist’s Buttonwood Gathering on October 25th 2012. He was interviewed by The Economist’s Philip Coggan. Listen to his comments at the end to regarding uncertainty: Hugh Hendry: God is dead, China will followwww.ritholtz.com/blog/2013/05/hugh-hendry-investing-amidst-crashes-china-speculators/! |

|

|

|

Post by jeffolie on Jun 26, 2013 6:23:22 GMT -6

collapse will start within 1.6 years my jeffolie view: collapse will start within 1.6 years, take upto 3 years ... reach BOTTOM AREA about 2016-7 ... Trickle Down will fail ... a new Great Depression will start China has tightened, the FED will tighten as 'tapering'... mortgage rates jumped ... housing bust coming" ... Since the beginning of June, the Shanghai stock index is down about 15%. Since the February high of 2443, the market is down nearly 20%. Intraday, the market was down over 25% from the year's high. ... In the past few week, China intraday lending rates as measured by SHIBOR got as high as 25% ... sent the Shanghai stock market index down about 6% ... the People’s Bank of China on Tuesday was the clearest attempt yet by the government to calm the turmoil that has shaken global markets over the past week and fuelled concerns that the world’s second-biggest economy could be on the verge of a credit crisis .... highly unlikely to work. The structural problems are immense: 1.China's shadow banking system is a mess

2.Property bubbles are immense

3.Infrastructure malinvestment is unprecedented

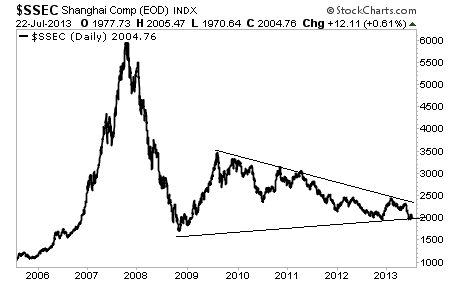

4.Rolling over of loans of State Owned Enterprises (SOEs) is going to be very problematic with any increase in interest rates======================================================== June 25, 2013 China Acts to Calm Markets; Stock Market Rebounds From 6% Plunge After Central Bank Pledges More Liquidity; Wet Nurse Action In the past few week, China intraday lending rates as measured by SHIBOR got as high as 25% (See China Cash Crunch: 1-Day Interest Rate Spikes to Record High 25%). With rates spiking, global stock markets plunged. On Monday China insisted banks had significant liquidity sending a message that banks need to manage their own risks. A translated message by the People's Bank of China on liquidity states "Commercial banks should concentrate storage for taxes and statutory reserve deposit and other factors impact on liquidity in advance to arrange sufficient positions to maintain adequate levels of reserve ratio, to ensure the normal settlement" while warning "expansion of credit and other assets too fast may lead to liquidity risk". That message sent the Shanghai stock market index down about 6% as shown in the following chart. Shanghai Composite Intraday Chart  2.bp.blogspot.com/-5jkHz4e_Y1Q/UcnMWfZtPlI/AAAAAAAAWNE/rShb1R2FKrg/s1600/China+Intraday.png 2.bp.blogspot.com/-5jkHz4e_Y1Q/UcnMWfZtPlI/AAAAAAAAWNE/rShb1R2FKrg/s1600/China+Intraday.pngThe horizontal line represents a split shift when the stock market is open. $SSEC Shanghai Daily Chart  3.bp.blogspot.com/-LNWVn5YSFsY/UcnRcMKhr2I/AAAAAAAAWNU/X-LjIwfC4Wg/s1600/$SSEC+Daily.pngSince the beginning of June, the Shanghai stock index is down about 15%. Since the February high of 2443, the market is down nearly 20%. Intraday, the market was down over 25% from the year's high. 3.bp.blogspot.com/-LNWVn5YSFsY/UcnRcMKhr2I/AAAAAAAAWNU/X-LjIwfC4Wg/s1600/$SSEC+Daily.pngSince the beginning of June, the Shanghai stock index is down about 15%. Since the February high of 2443, the market is down nearly 20%. Intraday, the market was down over 25% from the year's high.Mid-day, Tuesday, the China central bank decided it could take no more, and that's when the market rally took place, erasing nearly all of the 6% intraday drop shown in the first chart. China Acts to Calm Markets The Financial Times reports China in fresh effort to calm shaken markets. China has pledged to backstop banks suffering from cash shortfalls, giving rattled investors hope the country’s money squeeze could be nearing an end. The statement by the People’s Bank of China on Tuesday was the clearest attempt yet by the government to calm the turmoil that has shaken global markets over the past week and fuelled concerns that the world’s second-biggest economy could be on the verge of a credit crisis. “If banks have temporary shortages in their planned funding, the central bank will give them liquidity support,” it said in the statement. “If institutions have problems in managing their liquidity, the central bank will apply appropriate measures under the circumstances to maintain the overall stability of money markets.” In its latest statement, the central bank said money markets were already on the mend after interbank rates spiked to double digits last week. It noted that the overnight bond repurchase rate had fallen to 5.83 per cent, more than half what they were last week, though still about twice as high as normal. “Several strong banks have already started to play an important role in providing funds to the market and stabilising interest rates,” it said. A commentary earlier on Tuesday in the People’s Daily, official newspaper of the Communist party, called on authorities to continue an unyielding stance. “The central bank is not a wet nurse to the stock market. If it saves the stock market, it will in fact be harming it,” the paper wrote. Wet Nurse Action The central bank efforts to provide liquidity are highly unlikely to work. The structural problems are immense: 1.China's shadow banking system is a mess 2.Property bubbles are immense 3.Infrastructure malinvestment is unprecedented 4.Rolling over of loans of State Owned Enterprises (SOEs) is going to be very problematic with any increase in interest rates For further reading, please see ... •Cash Squeeze in China, Interest Rate Swaps Rise Most in 22 Months; China's Credit Bubble About to Pop; Shadow Banking Crackdown •Pettis on China, Europe, Japan: Bad News for Those Looking for Growth •Epic Glut of Graduates Depresses Wages; Fake Job Offers Taint Hiring Statistics In theory the central bank could paper over this mess with massive amounts of liquidity, but in practice, such action will either further fuel China's immense structural problems, or more likely, the credit bubble in China has gotten as big as it is going to get, no matter what the Central bank does. The world is not remotely prepared for a major slowdown in China. Yet, China's credit bubble has popped, and growth going forward will plunge as China rebalances. globaleconomicanalysis.blogspot.com/2013/06/china-acts-to-calm-markets-stock-market.html |

|

|

|

Post by jeffolie on Jun 28, 2013 5:56:15 GMT -6

China death spiral, April 2013 Oligarchs 2017 RISE OF THE CHINESE OLIGARCHS 2017 I predict China will collapse when America declines into an economic and political bottom period by 2016, follow the USSR path into a 'democratic govt' featuring elections with the wealth ending up in the hands of 'oligarchs' similar to what happened in the sucessor Russia. China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016 Another source of China's decline continues to grow: higher labor costs and inflation POLITICS MATTER IN CHINA ... CHANGE IN LEADERS The new leaders have presented little significant change from its situation of " ... China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail ..." " ... the surge in receivables indicates growing liquidity problems in Corporate China. A lot of companies aren't generating enough cash to meet their financial obligations, ====================================================== barronsJUNE 22, 2013 Where Will It End? By JONATHAN R. LAING China's credit growth to back lavish construction and infrastructure projects is similar to that of the U.S. and Japan before they faced financial calamities. Of all the global economic powers, China would seem the most immune to the threat of a financial crisis. It sailed through the post-2008 global credit implosion largely unscathed, by pumping up housing construction and infrastructure spending to compensate for slackening exports. First-quarter 2013 growth in gross domestic product, although the weakest in more than two years, rose at a rate the rest of the world would envy, 7.7%. Bad debts inside the Chinese banking system stand at a negligible 1%, compared with 3.4% in the U.S. and double-digit figures in much of the euro zone. And Beijing seemingly has plenty of additional resources to employ to spur growth. China's economy boasts a debt-to-GDP ratio reckoned conservatively at about 30%, less than half the national debt rate of the U.S. In his recent summit talks with President Barack Obama, China's President Xi Jinping pointedly expressed his satisfaction with the Chinese economy. But appearances can be deceiving, especially in China. Skeptics always have insisted that China's economic numbers paint too rosy a picture. Now those statistics show a worrisome downshift in growth for both exports and industrial production. Signs of trouble abound. A post-2008 credit bubble in China seems to be yielding increasingly limp GDP growth, as spending on gaudy new infrastructure projects and housing no longer packs the same punch. Miles upon miles of empty apartment buildings rim hundreds of Chinese cities; industries suffer from rampant over-capacity; and largely empty new highways, bridges, shopping malls, railroad stations, and airports more than hint at problems. A number of observers, including some former China bulls, see the country headed for a potentially serious economic downturn, or possibly a Japanese-style purgatory of anemic growth, with all the baleful side effects. These could include collapsing prices for assets like real estate (stocks already sell at big discounts), diminishing wealth, and, in extremis, frenzied capital flight by rich Chinese. "I would say that China is now roughly at the stage [of indiscriminate credit growth] the U.S. was in March 2008, when Bear Stearns had to be rescued and the subprime market was unraveling," says David Cui, Bank of America Merrill Lynch China strategist, working out of Shanghai. "What will tip the scale will likely be a major event in China similar to Lehman's bankruptcy six months after the fall of Bear Stearns, which will be some bailout of a major player that Beijing will do everything it can to disguise so as not to shake confidence." Echoes George Magnus, a London-based economist and independent advisor to UBS who has written extensively about China: "The financial situation in China has become quite alarming. Cracks are appearing all through its financial structure as a result of debt-fueled overinvestment in infrastructure, industrial capacity, housing, and commercial construction. There's likely to be big trouble coming in the next year or two." Moreover, a major cash crunch has erupted this month that could be a tell of systemic liquidity problems. Overnight rates in the key interbank credit markets soared last Thursday to more than 13% from under 8% the day before and less than 4% in May. A medium-size state-owned bank, China Everbright, recently defaulted on a six-billion yuan ($980 million) loan from another bank. Some commentators dismiss the cash crunch as Beijing's attempt to drain liquidity from the system to slow the runaway growth in lending. A flight of foreign capital out of China has also strapped the banking system. But the crunch could be a sign of ebbing confidence in loan quality in the Chinese financial system, similar to what occurred in the U.S. and elsewhere in the fall of 2008 when Libor soared and the credit system froze up. THE PRIMARY FAULT LINE in the Chinese economy that worries many has been the explosion in the credit-to-GDP ratio since the onset of the 2008 global financial crisis and economic slowdown, as China sought to stimulate its economy in the face of a lag in its longtime growth engine, exports. This total societal debt load has followed a similar growth trajectory to that of the U.S. and British economies in the six years leading up to the 2008 crisis; Japan's credit orgy from 1985 to 1990, a prelude to two decades of stagnant growth punctuated by bouts of deflation, or Korea prior to the Asian financial crisis (see charts below). According to a report from analysts at Fitch, China's recent credit bubble has topped them all with total debt (a broad measure which includes business, household and local government debt but not central government debt) rising from 130% of GDP in 2007 to 210% in the first quarter of this year. In Japan, by comparison, during the fateful six-year credit bubble, the jump in the ratio was just 45 percentage points, from about 150% to just over 195%. SUCH RAPID CREDIT booms tend to come to sorrow because of slipshod analysis and misallocation of resources. The quality of China's credit-fueled investment boom in the past four-and-a-half years has been suspect. The obvious low-hanging fruit of projects had already been plucked. Smart investment is far tougher as economies like China move up the value chain. Likewise, gobs of new liquidity tend to spawn asset bubbles, which can dull the appreciation of risk. With prices of, say, houses in the U.S. levitating upward in the years before the bust, investors become emboldened and lenders confident in the strength of the collateral underlying their loans. Xi's cockiness in his talks with Obama is understandable. China has enjoyed more than three decades of extraordinary economic gains spurred by the internal migration of workers from the countryside to the city and heavy spending on industrialization and infrastructure improvements. Build it, and they will come. Economic growth can trump mistakes and excesses. The Chinese credit explosion, however, has sluiced funds into sectors that hold much peril. For example, money has been lavished on giant state-owned enterprises that dominate such key basic industries as steel, cement, electrolytic aluminum, plate glass, coking coal, solar panels, and wind-turbine production. This has created severe overcapacity in these industries that, ominously, has sent China's producer price index into negative territory in the last 12 months, slipping another 2.9% in May, and sharply curtailed corporate profitability.

There has also been a huge surge in infrastructure spending since 2008, primarily on the part of local-government financial vehicles, which are special investment platforms. Many of the projects -- roads, bridges, international ports, and airports -- don't seem to have a good economic rationale. A number of projects have produced allegations of graft, often against party operatives who sometimes demonstrate more interest in getting rich than serving the public. In any event, many recent, debt-financed projects won't generate cash flow for years, if ever. They were merely big, splashy projects that temporarily boosted employment and economic growth during their construction phase before sinking into a moribund state. The New South China Mall, twice the size of the U.S.'s Mall of America in Minnesota, has been 99% vacant since its 2005 opening. In fact, a recent working paper by the International Monetary Fund concluded after a cross-country survey that excessive investment on infrastructure and industrial projects, amounting to about 10% of GDP, or about CNY5 trillion, would have "little impact on future growth" or long-term "favorable spillover into household income or consumer spending." BUT NO CHINA CREDIT STORY would be complete without mention of the real-estate construction boom that has pumped up perhaps the biggest bubble of all. For example, nine times the commercial space sold last year is under construction now. Residential construction has been in a white heat for some time and has attracted much notice in the financial press and elsewhere. Stories about the "ghost city" of Ordos in Inner Mongolia have become a staple, showing the eerie empty streets and deserted modern, high-rise apartment buildings, stores, and public buildings of a megapolis expected to attract more than one million people. It has been empty for the six years since its construction. Stories abound about similar projects in other cities either still under construction or sitting vacant. Word came last month that Broad Group, a Chinese maker of central air-conditioning systems, had been green-lighted to break ground this month on the tallest building in the world, near the unprepossessing capital of Hunan Province, Changsha. Sky City, as the project has been dubbed, will include a hospital, school, hotel, and retail and office space in addition to living quarters. And new modular construction techniques pioneered by Broad will enable the company to build the project in just months. Yet even with the overbuilding, market prices of apartments haven't cracked, at least according to government reports. Developers can still borrow money for new projects even while trying to roll over and carry debt on their inventory of unsold apartments. Faith remains undiminished that continued migration from the countryside to the cities will cure all housing oversupply. Besides, apartment purchasing has become the No. 1 investment game in China after the stock market crapped out in 2007, with the Shanghai Index falling nearly 70% since. Apartments are now more than living space -- they have become a store of value and an insurance policy against penury in old age. Living in them or even renting them out is deemed to diminish property value should someone ever show up to lease one. So they remain vacant. Press reports recently said a party official was busted for, among other things, secretly owning some 50 apartments. A collapse in the Chinese real-estate market would require only a slight shift in investor psychology. And once prices start to crumble, the results to the credit system and, ultimately, the general economy promise to be severe and widespread. Likewise, buildings and land are bedrock collateral supporting many corporate and local government loans. GONE ARE THE DAYS when the central government exercised tight control over credit through the Chinese banking system, in which it held a roughly 95% stake. The past five years has seen the explosion of China's shadow banking system that largely operates in a regulatory realm outside the direct control of Beijing, and yet last year was estimated to have accounted for more than 45% of China's credit creation. This burgeoning nonbank channel comprises a crazy quilt of institutions and investing instruments that extends from off-balance-sheet offerings of wealth-management products from traditional banks to the credit wares of brokerage houses, pawn shops, and credit-guarantee loan paper. Even the fast-growing Chinese bond market can be chaotic, with four regulators, poor disclosure, and credit-rating inflation. The popularity of shadow-banking products is easy to grasp. Chinese consumers are starved for investment yield with official deposit rates set so low. Many private firms lack access to bank lending, either because of government policy or the favoritism enjoyed by state-owned enterprises. But a number of products offered are reminiscent of the worst structured investment vehicles and collateralized debt obligations issued in the U.S. prior to 2008. Their structures are opaque, with debt maturities mismatched with underlying assets, and disclosure is risible. A credit crisis would likely begin somewhere in the shadow banking system with a large credit default or the bankruptcy of a major player, observes Charlene Chu, Fitch's senior banking analyst in Beijing. "In China, trouble starts on the fringes of the system and then moves into the core," she says. Signs of financial trouble abound even in China's official numbers, which many say are designed to obscure problems. The post-2008 credit surge, for example, seems to be losing its ability to generate actual growth. During the boom period of 2005 up to early 2008, statistics show that one yuan of credit yielded nearly one yuan of GDP growth. But no more. Last year, it took four yuan to generate just a single yuan of increased GDP, according to government-based figures. This collapse in capital efficiency indicates several things to China watchers. Much of the money was being wasted, going into projects that weren't generating sufficient ongoing revenues or, possibly, any revenues at all. Likewise, many suspect that much of the new credit went to "evergreen," or roll over, old loans gone bad, or at least coverage of the debt service and operating expenses of debtors with cash-flow problems. Debt is building up with particular speed in the corporate sector just as revenue growth is flagging. According to GK Dragonomics researcher Andrew Batson, corporate debt jumped from 108% of GDP to 122% just between 2011 and 2012. Much of that rise is occurring in accounts receivable, or unpaid bills by customers, that reside on the asset side of corporate balance sheets. Official numbers put that total at CNY8.5 trillion in April, up 13% from a year ago. Yet many private estimates claim that the increase may be as high as 20% or more. Zoomlion, China's biggest heavy-construction-equipment maker, has seen its accounts receivable leap to CNY2.7 billion in 2012 from CNY912 million the year before and just CNY106 million in 2008. At a minimum, the surge in receivables indicates growing liquidity problems in Corporate China. A lot of companies aren't generating enough cash to meet their financial obligations, no matter the degree to which uncollectible receivables might artificially inflate corporate revenues and profits on paper. Many of the receivables are turned into cash when banks purchase or "accept" them on a discounted basis. These acceptances, in turn, show up as supposedly safe money-market instruments in all manner of investment products sold to households, such as wealth-management investments. Thus, any surge in defaults on China's pile of corporate receivables, if unchecked, would cascade through the financial system, hurting households, banks, local governments, manufacturers, and the chain of suppliers. How much debt will go bad is anybody's guess, but the total is much higher than the 1% that Beijing officially reports in the Chinese banking system. Some estimate the eventual total, including sources outside the banks, could be as high as 20% of 2012 year-end total debt of about CNY100 trillion. Losses of just CNY6-7 trillion would wipe out the capital of the state banking system. BEIJING HAS WEAPONS to fight off a financial crisis, either by directly or indirectly papering over shortfalls, Chu concedes. It could unleash some of the CNY19 trillion that its central bank holds as loan reserves, or deploy the $3.38 trillion (CNY20.7 trillion) in foreign-currency reserves, though much of that has already been committed. Beijing also could sell part of its interests in its state-owned enterprises, though Chu reasons that the central government would be reluctant to dump such assets at "fire-sale prices." As a last resort, China could also print money, adding to the rapid monetary growth of recent years. China doesn't have to look too far for a cautionary tale. Japan in the late '80s and early '90s faced a similar slowdown in economic growth. Like China today, it sought to compensate by first unleashing a flood of credit, creating a real-estate bubble, and then engaging in infrastructure spending on the proverbial bridges to nowhere. "But it didn't work, despite the fact that Japan, like China today, boasted a high savings rate, plenty of fiscal capacity, and little foreign debt," says Patrick Chovanec, who spent a decade doing private-equity deals in China and teaching business at Tsinghua University in Beijing, before becoming a strategist at Silvercrest Asset Management, a New York money manager. "The flaw is that sometimes it takes so much capital to fill an existing hole that there's not enough money left to promote growth." That could be the case for China and its flawed economic model. It is fast running out of effective responses to the iron law of diminishing returns. online.barrons.com/article/SB50001424052748704878904578541251070413678.html?mod=BOL_GoogleNews&google_editors_picks=true#articleTabs_article%3D1 |

|

|

|

Post by jeffolie on Jul 1, 2013 7:54:47 GMT -6

China PMI Drops To Lowest In 9 Months; Schrodinger's Economy Continues 06/30/2013 Following South Korea's dip back into contractionary mode (PMI sub-50 for first time in six months - prompting JPY strength and NKY weakness, on implicit KRW weakness retaliation), it appears China's government-sanctioned PMI (printed at 50.1 relative to 50.8 prior and 50.1 expectations) is converging down to the nation's HSBC PMI (whose Flash print was 48.3 - final due at 2145ET). This is the equal lowest print in 9 months but provides just enough cover to the current administration to maintain its tight policy stance - even if it was the biggest MoM drop in 10 months. On a side-note, all PMI sub-indices also fell MoM. The market's response is modest AUD strength and Nikkei weakness which suggests investors were hoping for a little weaker data to push China a litte closer to folding on their bubble-popping position.  www.zerohedge.com/sites/default/files/images/user3303/imageroot/2013/06-2/20130630_china.jpg www.zerohedge.com/news/2013-06-30/china-pmi-drops-lowest-9-months-schrodingers-economy-continues www.zerohedge.com/sites/default/files/images/user3303/imageroot/2013/06-2/20130630_china.jpg www.zerohedge.com/news/2013-06-30/china-pmi-drops-lowest-9-months-schrodingers-economy-continues

|

|

|

|

Post by jeffolie on Jul 1, 2013 15:41:54 GMT -6

Selling to America & EU will destroy China's political system & economy as exports are now declining. ============================================ June 30, 2013 China Manufacturing Conditions Deteriorate, New Export Orders Fall at Fastest Rate Since March 2009 In what should be no surprise to Mish readers, the HSBC China Manufacturing PMI™ shows Operating conditions deteriorate at quickest pace since last September, and new export orders plunge. Key points Output contracts for first time since last October New export orders fall at the joint-fastest rate since March 2009 Job shedding intensifiedManufacturing PMI After adjusting for seasonal factors, the HSBC Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – posted at 48.2 in June, down from 49.2 in May, signalling a modest deterioration of business conditions. Operating conditions have now worsened for two successive months. Chinese manufacturers signalled a first reduction of output for eight months in June. The rate of contraction was modest, and generally attributed to weaker client demand, as total new orders declined for the second month in a row. New business from abroad also fell in June, with the rate of contraction the fastest since last September, and the joint-sharpest in over four years. Anecdotal evidence suggested that reduced client demand, particularly from Europe and the US, led to fewer new export orders.  4.bp.blogspot.com/-GNtU7xEuSPE/UdDwi8ciIsI/AAAAAAAAWR8/aMhangKxubU/s458/Markit++China+Manufacturing+2013-07-01.png 4.bp.blogspot.com/-GNtU7xEuSPE/UdDwi8ciIsI/AAAAAAAAWR8/aMhangKxubU/s458/Markit++China+Manufacturing+2013-07-01.pngComment Commenting on the China Manufacturing PMI™ survey, Hongbin Qu, Chief Economist, China & Co-Head of Asian Economic Research at HSBC said: “Falling orders and rising inventories added pressure to Chinese manufacturers in June. And the recent cash crunch in the interbank market is likely to slow expansion of off-balance sheet lending, further exacerbating funding conditions for SMEs. As Beijing refrains from using stimulus, the ongoing growth slowdown is likely to continue in the coming months.” I frequently disagree with Markit economic comments but these comments from Hongbin Qu are spot on. Mike "Mish" Shedlock Read more at globaleconomicanalysis.blogspot.com/2013/06/china-manufacturing-conditions.html#u86FLWF4L84D257m.99 |

|

|

|

Post by jeffolie on Jul 3, 2013 16:55:45 GMT -6

China death spiral, April 2013 Oligarchs 2017 RISE OF THE CHINESE OLIGARCHS 2017 I predict China will collapse when America declines into an economic and political bottom period by 2016, follow the USSR path into a 'democratic govt' featuring elections with the wealth ending up in the hands of 'oligarchs' similar to what happened in the sucessor Russia. China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016 Another source of China's decline continues to grow: higher labor costs and inflation " ... collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016 ... Another source of China's decline continues to grow: higher labor costs and inflation ..." ========================================================== Shanghai flag pattern breaks 20-year support, pulling other markets with it! Posted by Chris Kimble on 07/03/2013  blog.kimblechartingsolutions.com/wp-content/uploads/2013/07/shanghaieemflagbreakdownsjuly31.jpg blog.kimblechartingsolutions.com/wp-content/uploads/2013/07/shanghaieemflagbreakdownsjuly31.jpg Could a slow down in China not only impact other Emerging markets, could it ripple in the U.S.? The above 4-pack reflects that the Shanghai index is breaking support of a multi-year flag pattern, with the bottom of the flag pattern, being a support line that has been in place for 20-years. The 4-pack above reflects that the Hang Seng index is breaking support along with EEM and VWO, two of the six largest ETF's in the U.S.! Don't overlook the potential ripple effects and impact on markets in the U.S. if these flag breakdowns continue to push lower! blog.kimblechartingsolutions.com/2013/07/shanghai-flag-pattern-breaks-20-year-support-pulling-other-markets-with-it/ |

|

|

|

Post by jeffolie on Jul 10, 2013 7:19:07 GMT -6

10 July 2013 China reports weaker than expected trade data Manufacturing and export sectors are key drivers of China's economic growth China has reported an unexpected fall in its exports and imports, adding to concerns of a slowdown in its economy. Exports fell 3.1% in June from a year earlier, indicating weak global demand for Chinese goods. Most analysts had expected a 4% increase in shipments. Imports fell 0.7% from a year ago, showing a subdued domestic demand. China, the world's second-largest economy, has been keen to rebalance its economy, after a decline in global demand hurt its export-led growth. China's economy grew at an annual pace of 7.7% in the January to March quarter, compared with 7.9% in the previous three months. Analysts say second-quarter GDP figures, due to be released on Monday, are likely to show a further slowdown, as demand in key export markets in the US and Europe remains weak. www.bbc.co.uk/news/business-23251089 |

|

|

|

Post by jeffolie on Jul 10, 2013 11:15:53 GMT -6

In this issue by Phoenix Capital Research • China's exports implode at the worst pace since 2009. • So much for the economic miracle. • Is the US next? July 10, 2013 The Economic "Miracle" Has Failed... What's Next For the Markets? China, which the investment world blindly continues to believe will power the global economy to growth, just posted its single worst export data since 2009. All in all, Chinese exports fell 3.1% from a year earlier. Analysts had forecast growth of 3.7%. The reason? They continue to believe China will somehow pull a rabbit out of a hat and grow exports at a time when the global economy is sharply contracting. Let’s look at the facts here. In the last six months, China has pumped roughly $1.6 trillion in new credit (that’s 21% of GDP) into its economy. Despite this incredible monetary expansion, Chinese GDP growth is slowing. Mind you, this slowing growth is occurring even after China massages the heck out of its GDP data. As I recently told my Private Wealth Advisory subscribers, when you look at electrical usage by the People’s Republic, real GDP growth is likely just 2.9%.

This is truly astounding: a country has expanded its credit by 21% of GDP in just six months and is barely able to generate positive GDP growth. Small wonder that the Chinese stock market has taken out its post-2009 trendline.  gainspainscapital.com/wp-content/uploads/2013/07/sc2.png?inf_contact_key=dcc96b607509c922b6eb136963c12e84eefec7a39c1db9cf2fe33fbf55a55716 gainspainscapital.com/wp-content/uploads/2013/07/sc2.png?inf_contact_key=dcc96b607509c922b6eb136963c12e84eefec7a39c1db9cf2fe33fbf55a55716China is giving us a taste of what will be spreading throughout the global economy: a collapse in spite of massive monetary expansion. The entire “recovery” since 2009 has been based Central banks pushing money into the financial system… which did little more than allow corporations to borrow even more debt. Indeed, globally the leverage in the financial system today is as bad if not worse than it was going into the 2008 Crash. Can you imagine what would happen if we suffered another collapse now, when Central Banks are already pumping their brains out trying to push market higher? gainspainscapital.com/2013/07/09/this-has-never-happened-before/ |

|

|

|

Post by unlawflcombatnt on Jul 10, 2013 11:53:21 GMT -6

Pumping credit into an economy to promote capital investment in production is pointless when there is not enough demand for that production.

This is an amazingly simple concept--that the elite either cannot comprehend, or more likely don't want to accept.

All that happens when investors have capital, in excess of demand for productive investment, is the investment in, and subsequent hypervaluation of non-productive fixed assets (think Housing).

All that the Bernanke monetary expansion has done is foster even more non-productive investment, while diminishing the necessary production demand by monetary expansion and reducing (or limiting) the buying power of consumers who are not recipients of the Fed's monetary largesse.

Claiming there's been no inflation is a false canard. If the buying power of American consumers were to increase via "deflation", with a resultant increase in the buying power of current dollars, it would INCREASE demand, and increase demand for investment of already overabundant capital.

The buying power of consumers needs to be increased, not the investment power of rich investors.

They already have more than enough capital to invest. But there simply isn't any demand for investment due to lack of demand for the products that would be produced.

|

|

|

|

Post by jeffolie on Jul 23, 2013 6:13:28 GMT -6

China moves ... increase investment in railway projectsmy jeffolie view: New leaders recognize the 'China death spiral' resulting in Railroad production which POLITICS MATTERS most likely includes expanding east from the manufacturing and ports concentration into less labor inflation, lower land costs, less POLLUTION

================================================= China moves send world shares higher, dollar softens Jul 23, 2013 LONDON (Reuters) - World shares pushed on towards five-year highs on Tuesday, helped by China's efforts to avoid a hard landing for its slowing economy, while gold took a breather after its biggest one-day gain in more than a year. Local media in China reported the government was looking to increase investment in railway projects to reduce gluts in steel, cement and other materials as it aims to ensure annual economic growth does not sink below 7 percent. The reports lifted stocks across Asia outside Japan by 1.3 percent to their highest since early June and gave an early boost to mining stocks in London, although a lack of detail made some in the markets cautious. "Managing to keep (growth) above 7 percent will certainly be viewed as a positive stance," said IG Markets analyst Alastair McCaig. "But they really have only five months to prove their words are worth their weight."

... although a lack of detail made some in the markets cautious. ...

www.reuters.com/article/2013/07/23/us-markets-global-idUSBRE88901C20130723

|

|

|

|

Post by jeffolie on Jul 23, 2013 6:46:47 GMT -6

China death spiral, April 2013 Oligarchs 2017 RISE OF THE CHINESE OLIGARCHS 2017 I predict China will collapse when America declines into an economic and political bottom period by 2016, follow the USSR path into a 'democratic govt' featuring elections with the wealth ending up in the hands of 'oligarchs' similar to what happened in the sucessor Russia. China has failed to convert to a domestically balanced economy led by the consumer and remains a 'trading, merchantile' empire which the 'rhyme of history' examples show a collapsing event most often happens when its customers fail: already the EU biggest customer continues to enter a death spiral, leaving only America's Walmart led buying...this will decline into 2016 Another source of China's decline continues to grow: higher labor costs and inflation by Phoenix Capital Research In this issue • Could China be posting ZERO growth? • These numbers don't lie. • What would a world with NO growth in China look like? • More! July 23, 2013 The Black Swan No One is Talking About Another “growth story” is dying before our very eyes. As I've warned Private Wealth Advisory subscribers, China is rapidly approaching ZERO growth. This is not less growth, but ZERO growth as in full-scale economic collapse from the days of 12% GDP growth per year. Over 95% of “analysts” are missing this, but it is a fact. If you ignore the ridiculous GDP numbers (which even China’s Premiere has admitted are a joke in the past) and look at more accurate metrics, it’s clear China is collapsing at an alarming rate. Case in point, Electrical consumption rose by just 2.9% in the first quarter of this year. How on earth can you generate GDP growth of 7% when you electrical consumption is rising by just 2.9% is beyond me. And when you consider that China is experiencing this weak growth despite having pumped over $1 trillion into its economy in the same quarter (an amount equal to 14% of China’s total GDP) you begin to understand the scale at which things are imploding in the People’s Republic.

Check out the chart for China’s stock market: we’re about to take out the post-2009 “recovery” trendline. And this is while China is pumping trillions in new credit into its economy!  gainspainscapital.com/wp-content/uploads/2013/07/sc-51.png?inf_contact_key=d04db2b0a82d7646f7cb21d7484c055b96e40d37b12f0ac93070064cbcdb3ec4 gainspainscapital.com/wp-content/uploads/2013/07/sc-51.png?inf_contact_key=d04db2b0a82d7646f7cb21d7484c055b96e40d37b12f0ac93070064cbcdb3ec4This is a Black Swan that few are noticing. If you look around the mainstream financial media in the US, you see talk of Bernanke tapering, discussions of rising interest rates and even the occasional story about how Europe is not fixed. But you won’t find stories about China facing ZERO growth. There’s only one I’ve seen and it was published in the Telegraph, a British newspaper. by Phoenix Capital Research |

|

|

|

Post by jeffolie on Jul 23, 2013 7:33:39 GMT -6

EDITORS: PLEASE ELIMINATE THIS PHOTO. THIS PHOTO IS NOT PERMITTED TO BE USED IN CHINA - In this Friday April 6, 2007 China bans construction of government buildings BEIJING (AP) -- China's leaders have banned the construction of government buildings for five years as another step in a frugality drive that aims to address public anger at corruption. The general offices of the Communist Party's central committee and the State Council — China's Cabinet — jointly issued the directive Tuesday, according to the official Xinhua News Agency. No directive was immediately available online. Across China, grand government buildings with oversized offices and fancy lighting including chandeliers have mushroomed in many cities. They are often among the most impressive buildings in their own towns, drawing disapproval from the public. President Xi Jinping has spearheaded a campaign to cut through pomp, formality and waste among senior officials that have alienated many ordinary citizens. This year, high-end restaurants have reported a downturn in business as government departments and state-owned companies canceled banquets.

Xinhua reported that the directive orders an "across-the-board halt" to construction of official buildings, and "glitzy" structures built as training centers, hotels or government motels. Some government agencies have built such buildings in seaside resorts and other scenic spots as a perk for their officials and employees who can stay for free or at deeply discounted prices. They sometimes open to the public as profit-making ventures. "Some office buildings use up a lot of money, there are operating costs and a lot of money is spent on people eating and drinking which all comes from government funds, so it's a kind of corruption," said Liu Shanying, a politics researcher at the Chinese Academy of Social Sciences in Beijing. The five-year construction ban is a significant move to fight corruption, he said. The directive forbids luxury interior design and the expansion of office compounds that is done under the guise of repair work, according to Xinhua. It also says that officials with more than one post should have only one office while the offices of those who have retired or taken leave should be returned in time. Xinhua said the directive noted that some departments and localities have built government office compounds in violation of regulations, which has tainted the image of the Communist Party and the government and stirred vehement public disapproval. It added that the directive calls on party and government bodies to be frugal and ensure that government spending goes toward developing the economy and boosting living standards.

There have been restrictions on constructing new government buildings in the past, but they have not always been implemented well at local levels, said Liu. Even the offices of some heads of rural counties are sometimes up to 200 square meters (2,150 square feet) in size, "maybe even bigger than the U.S. president's office," said Liu. news.yahoo.com/china-bans-construction-government-buildings-113527094.html |

|

|

|

Post by jeffolie on Jul 24, 2013 6:48:22 GMT -6

China Coal Fired Economy water war So many issues present in this piece: China's dependency on coal China's ignoring pollution ... economy over health China's POLITICS MATTERS dominating the decisions " ... A shortage of coal because of the lack of water to mine and process the fuel may force China to increase imports, pushing up world prices, ... Among the biggest losers are farmers, who have to dig deeper and deeper wells to find clean water, or are forced out by local governments who see bigger economic gains from mining. ... Caps introduced in January limit the annual increase of water used by the four biggest coal-producing regions to 2.9 percent annually until 2015, while their combined coal output is set to increase almost 5 percent a year, according to CLSA. ... they “don’t dare to really monitor” pollution because it would affect growth, Zhang said at a forum. The officials said when “economic growth conflicts, environmental targets always give way,” .... coal is refined at a coal washing facility in Shanxi province. Coal mining and power stations use as much as 17 percent of China’s water, and almost all of the collieries are in the vast energy basin in the north that is also one of the country’s driest regions. ... “Water shortages will severely limit thermal power capacity additions,” ... Water shortages mean “industrial plants are more and more under pressure,” said Guillaume Dourdin, Beijing-based head of the North-West China region for France’s Veolia Water, which treated 1.2 billion tons of waste water in China last year. “In some places we can see it is a constraint for industry. We don’t see a water war in China but obviously there are some tensions on the resource in some parts.” Veolia Water, a unit of Veolia Environnement SA (VIE), Europe’s biggest water company, has more than 13,000 employees in China. ...

===============================================

China Coal Fired Economy Dying of Thirst as Mines Lack Water

By Bloomberg News Jul 24, 2013

At first glance, Daliuta in northern China appears to have a river running through it. A closer look reveals the stretch of water in the center is a pond, dammed at both ends. Beyond the barriers, the Wulanmulun’s bed is dry.

Daliuta in Shaanxi province sits on top of the world’s biggest underground coal mine, which requires millions of liters of water a day for extracting, washing and processing the fuel. The town is the epicenter of a looming collision between China’s increasingly scarce supplies of water and its plan to power economic growth with coal.

Coal is refined at a coal washing facility in Shanxi province. Coal mining and power stations use as much as 17 percent of China’s water, and almost all of the collieries are in the vast energy basin in the north that is also one of the country’s driest regions.

July 18 (Bloomberg) -- Markus Rodlauer, the International Monetary Fund’s mission chief for China and deputy Asia-Pacific director in Washington, talks about the outlook for China's economy. The IMF said risks are increasing that China’s economic growth this year will fall short of the lender’s forecast as it urged the nation to ...

Laborers work to load a construction beam at the site of South-to-North Water Diversion Project in Shijiazhuang, Hebei province. To alleviate the water shortage in the north, the central government in 2002 approved the 500 billion yuan project, the largest irrigation project in the world.

.

“Water shortages will severely limit thermal power capacity additions,” said Charles Yonts, head of sustainable research at brokerage CLSA Asia-Pacific Markets in Hong Kong. “You can’t reconcile targets for coal production in, say, Shanxi province and Inner Mongolia with their water targets.”

Coal industries and power stations use as much as 17 percent of China’s water, and almost all of the collieries are in the vast energy basin in the north that is also one of the country’s driest regions. By 2020 the government plans to boost coal-fired power by twice the total generating capacity of India.

About half of China’s rivers have dried up since 1990 and those that remain are mostly contaminated. Without enough water, coal can’t be mined, new power stations can’t run and the economy can’t grow. At least 80 percent of the nation’s coal comes from regions where the United Nations says water supplies are either “stressed” or in “absolute scarcity.”

Desert State

China has about 1,730 cubic meters of fresh water per person, close to the 1,700 cubic meter-level the UN deems “stressed.” The situation is worse in the north, where half China’s people, most of its coal and only 20 percent of its water are located.

Shanxi -- the nation’s biggest coal base, with about 28 percent of production -- has per capita water resources of 347 cubic meters, less than the Middle Eastern nation of Oman. Inner Mongolia and Shaanxi, which together contribute 40 percent of coal output, have less than 1,700 cubic meters per person.

A government plan to boost the coal industry and build more power plants near mines will lift industrial demand for water in Inner Mongolia 141 percent by 2015 from 2010, causing aquifers to dry up and deserts to expand, according to Greenpeace and the Chinese Academy of Sciences’ Institute of Geographical Sciences and Natural Resources. About 28,000 rivers have vanished since 1990, according to the Ministry of Water Resources and National Bureau of Statistics.

Ordos Wells

“After five years there won’t be enough water in Ordos in Inner Mongolia,” said Sun Qingwei, director of the climate and energy campaign at Greenpeace in Beijing. “The mines are stealing ground water from agriculture. Local governments want their economies to boom.”

Wells drilled near Haolebaoji near Ordos by Shenhua Group, the world’s biggest coal producer, have caused groundwater levels to drop to a depth of as much as 100 meters, drying out the region’s artesian wells, Greenpeace said in a report yesterday. Two calls to Shenhua weren’t answered.

The water that does exist is mostly polluted. A government survey published in February shows that only about a quarter of the groundwater in the North China Plain -- an area that’s bigger than Greece and includes Beijing and Tianjin, the province of Hebei and parts of Henan and Shandong -- is fit for human consumption.

Severe Pollution

Severe water pollution affects 75 percent of China’s rivers and lakes and 28 percent are unsuitable even for agricultural use, according to the 2012 book “China’s Environmental Challenges,” by Judith Shapiro, director of the Masters program in Natural Resources and Sustainable Development at the School of International Service at American University in Washington.

Geneva-based Pictet Asset Management’s $3.17 billion global water fund doubled its exposure to stocks offering water services in China to 10 percent since 2007. For Zurich-based RobecoSAM’s 611 million-euro Sustainable Water fund, “emerging markets offers the best opportunities in the world for water investments and China is the standout.”

Water-treatment companies Beijing Enterprises Water Group Ltd. (371) and China Everbright (165) International Ltd., which Pictet invested in in 2009, are among its best performers this year, partly on prospects for stricter environmental regulation in China, said Geneva-based portfolio manager Arnaud Bisschop.

Beijing Enterprises has risen 55 percent this year to HK$3.10 and Deutsche Bank sees it reaching HK$3.20 within a year. China Everbright is up 83 percent to HK$7.18 and JPMorgan Chase & Co. estimates it will reach HK$7.60 by mid-October.

‘Utmost Urgency’

“The best opportunity is in industrial water re-use, and for the mining industry, it is of the utmost urgency,” said Junwei Hafner-Cai, a manager of RobecoSAM’s Sustainable Water fund. “Water that has been released from the coal mines and from petrochemical plants has resulted in severe pollution on top of the water scarcity.”

A shortage of coal because of the lack of water to mine and process the fuel may force China to increase imports, pushing up world prices, according to Debra Tan, director at research firm China Water Risk in Hong Kong. China, which mines 45 percent of the world’s coal, may adopt an aggressive “coal-mine grab” to secure supplies, said Tan.

Chinese demand will account for 25 percent of global coal imports by 2015, London-based shipbroker ACM Shipping Group Plc said in a report in April. Indonesia is the largest overseas supplier of power-station coal to China, which buys as much as 45 percent of the Southeast Asian nation’s exports of the fuel.

China is responding with harsher limits on water usage, a new tariff structure that allows for steep price gains, and plans to spend 4 trillion yuan ($652 billion) by 2020 to boost water infrastructure and resources.

Water Caps

Caps introduced in January limit the annual increase of water used by the four biggest coal-producing regions to 2.9 percent annually until 2015, while their combined coal output is set to increase almost 5 percent a year, according to CLSA.

Water shortages mean “industrial plants are more and more under pressure,” said Guillaume Dourdin, Beijing-based head of the North-West China region for France’s Veolia Water, which treated 1.2 billion tons of waste water in China last year. “In some places we can see it is a constraint for industry. We don’t see a water war in China but obviously there are some tensions on the resource in some parts.” Veolia Water, a unit of Veolia Environnement SA (VIE), Europe’s biggest water company, has more than 13,000 employees in China.

Truck Queue

In Daliuta, the mine is “sucking up the groundwater,” said Sun at Greenpeace. Trains hundreds of cars long rumble along elevated tracks through the town center, hauling coal. On the highway to Yulin, trucks carrying the fuel queue nose-to-tail for more than five kilometers to pass through toll booths.

Daliuta’s coal output surged 26 percent last year to 29.4 billion tons, according to owner China Shenhua Energy Co. (1088), the nation’s biggest coal producer.

The town’s river-turned-pond was dammed about six years ago to beautify the area for new apartment blocks along the banks, said Zhe Mancang, who owns a liquor store nearby. The artificial lake is now contaminated with waste water from the mines.

“I worry about the water,” said Zhe, 58. “But I’ve no choice. My family’s here and my customers are from the mines.”

The effect of water shortages extends beyond the north. New rules this year require the manufacturing hubs of Jiangsu and Guangdong provinces and Shanghai to reduce water use every year even as their economies expand. Nationwide growth in usage is capped at 1 percent annually.

Water Prices

In the city of Guangzhou water prices rose 50 percent for residents and 89 percent for industrial users in May 2012 to help pay for improvements to quality and supply, according to an April report by Goldman Sachs Group Inc.

Stricter controls will raise the risk of investment in water-intensive industries and heavy polluters including coal, metals and paper production, especially in the north, said Tan.

“In an absolute worst case you’d see a large-scale shift in economic activity and population further south for lack of water, and manufacturing increasingly moving abroad,” said Scott Moore, a research fellow at the Harvard Kennedy School’s Sustainability Science Program in Cambridge, Massachusetts.

To alleviate the shortage in the north, the central government in 2002 approved the 500 billion yuan South-to-North water diversion project, the largest irrigation project in the world. The plan is to carry 44.8 billion cubic meters of water from the Yangtze river along three routes.

Tianjin Canal

The 1,467-kilometer-long eastern canal to Tianjin is scheduled for completion at the end of this year. The central route to Beijing, more than 1,270 kilometers, is slated to open next year. The western route is still being planned.

Even this massive program may not be enough. The Asian Development Bank said in a report last year that China’s demand for water may exceed supply by as much as 200 billion cubic meters by 2030, according to some estimates, unless “major capital investments to strengthen water supplies are made beyond those presently planned.”

More efficient use would help. Chinese industry uses four to 10 times more water per unit of production than the average in developed countries, Tan wrote in a February report. Only 40 percent of industrial water is recycled, compared with 75 percent to 85 percent in developed countries, the World Bank says.

Yellow River