|

|

Post by unlawflcombatnt on Feb 7, 2008 17:49:36 GMT -6

Trade Deficit:

Domestic Price Inflation vs. $ Devaluation

With extensive review of US economic statistics, especially GDP, the trade deficit, and home price increases—an unmistakable pattern emerges. Monetary expansion appears to widen the trade deficit. This pattern would seem to run counter to conventional wisdom, since monetary expansion devalues the dollar in relation to foreign currencies. This seeming contradiction occurs because the price of American exports in foreign markets may rise, despite the fall in the value of the U.S. dollar. Below is an explanation of how this occurs.

It has long been assumed that devaluation of the dollar compared to foreign currencies would reduce the trade deficit. This occurs, in theory, because devaluation of a country's currency reduces the price of its goods in relation to prices of the foreign country's goods. For example, if the US dollar could previously buy 1.5 Euros worth of merchandise, and now can only buy 0.75 Euros-worth, it makes Euro-denominated (and Euro-produced) goods more expensive to Americans. Since the price Americans now pay would be twice as high, American demand for Euro goods would decline, and sale to Americans would also decline. Meanwhile, American goods' prices would now be only 1/2 what they had previously been in Euros. The price decline in Euros would then increase Euro demand for American goods. This would, in turn, increase sale of American exports to the Euro zone. The end result should be an increase in American exports to Europe, a decrease in European import sales to Americans, and a decrease in the U.S trade deficit with the Euro zone.

That's the "theory," at least. The theory, however, has not worked out as well as predicted. In fact, the trade deficit has worsened with most foreign countries, despite the decline in the dollar's value vs. foreign currencies. The theory, however, often runs counter to observed reality.

What actually does affect the traded deficit, however, is US monetary policy and monetary expansion. From long-term macro statistics, US monetary expansion DOES seem to increase the trade deficit. (Even if not causative, monetary expansion is almost always paralleled by an increase in the trade deficit.)

This pattern can be seen when reviewing the last 30 years of US macro statistics, especially GDP, trade balance, and price inflation. The trade deficit increased when government or Fed policy caused expansion of the monetary supply—either by Fed injection of money to manipulate interest rates, or by government expansion of the money supply from policy to increase borrowing and loans—as every new loan increases the virtual money supply. (The most important of these policies was that of increasing home ownership.)

This trend became most noteworthy around 1997, when policies were enacted to increase home purchases, such as increasing tax advantages & deductions when buying and selling homes. These policies increased demand for homes, sales of home and prices of homes. As home prices rose, so did our trade deficit. Statistics demonstrate a parallel between the acceleration of home price increases and the increase in our trade deficit.

In fact, the biggest source of increased borrowable money came from the hyperappreciation of home prices.

The increase in home prices increased home equity, which increased the collateralization available to back more new loans. Home price increases thus allowed more people to borrow more money off their home's increasing equity value. More borrowing caused an expansion of the money supply. As more borrowed money became "borrowable" to purchase homes, prices rose still further. Further home price increases made still more money available to borrow. The increase in borrowed money also increased the spending power of American consumers. This increased spending power increased demand for goods and production, thus increasing prices as well.

Though the concocted BEA and BLS inflation measures may show little inflation, most people believe they've understated inflation considerably (and have done so deliberately.) Most Americans know from experience that the purchasing power of the dollar has fallen much more than the government has stated.

The rise in American spending power is the critical issue here. When American spending power drives up prices of domestic goods, it ALSO drives up prices on those same goods when they're exported. Given that 80-90% of domestic production is sold to Americans, 80-90% of demand-induced price pressure is also created by American consumers. Again, this is a key point.

Expansion of the U.S. money supply puts both upward and downward pressure on export prices. Whether export prices rise or fall depends on whether upward or downward price pressures predominate.

Expanding the US money supply devalues the dollar in foreign currencies—putting downward pressure on export prices—making American goods cheaper in foreign markets.

But more importantly, expanding the US money supply also puts upward pressure on domestic prices—which puts upward pressure on export prices as well. As a result, this drives up prices on American exports sold in foreign markets, making American goods more expensive in foreign markets.

In order for American goods to decline in price in foreign currencies, price reductions from dollar devaluation must be more than American consumer-induced price inflation. If American consumers drive prices up more than a devalued dollar lowers prices in foreign markets, the price of American goods to foreigners will rise, not fall.

In this case, the very monetary expansion that devalued the dollar makes American goods MORE expensive to foreigners— despite dollar devaluation—since it increased US price inflation even more.

For example, if the dollar fell -10% against the Euro as a result of US monetary expansion, but the US domestic prices increased +20% (from the same monetary expansion), the price of American goods in Euros would RISE by +10%, despite the -10% decline in the value of the dollar. In this case, price inflation was greater than dollar devaluation.

This, in my opinion, is what's happened over the last 10 years. American goods prices have increased more than the dollar has devalued. This has more than offset the effect of a devaluing dollar. Thus, the very policies that devalued the dollar, have American export prices to increase, instead of decreasing as conventional wisdom predicted.

Yet the theory that devaluation of the dollar, in and of itself, reduces relative prices of exports, is valid. And the theory that relative price changes affect the trade balance is true as well.

But the very factor causing dollar devaluation has an offsetting effect on domestic inflation. In fact, dollar devaluation is often more than offset, causing export prices to rise.

The price decreases from currency devaluation are often less than domestic price increases. Thus, when domestic price rises exceed the fall of the dollar, prices of American exports to foreigners increase. As a result, American export sales decrease, foreign import sales increase, and our trade deficit widens.

If US Price Inflation exceeds US Dollar Devaluation, our trade deficit worsens.

History has born this out.

|

|

|

|

Post by unlawflcombatnt on Feb 8, 2008 18:29:44 GMT -6

The point I was making in the original post is that dollar devaluation may not reduce our trade deficit—because domestic (American) price inflation may increase prices more than dollar devaluation reduces them (in foreign export markets.) In general, this is consistent with increases and declines in the Trade Deficit since 1980, which are shown in GDP statistics during that time. Monetary expansion seems to cause an increase in the trade deficit. Monetary contraction seems to reduce it. One would think that with monetary expansion, and resultant devaluation of the dollar, that this would cause a price decline of American goods in foreign markets. This should reduce the price of American goods to foreigners, thus increasing the sale of American exports in foreign markets. This should reduce the US trade deficit, increasing sale of US exports. This should reduce our trade deficit. It appears, however, that the exact opposite has happened. My explanation is that the same monetary expansion that devalued the dollar, also increased American product price inflation. Moreover, it increased price inflation MORE than it devalued the US dollar. Thus, the net effect was to make American exports MORE expensive in foreign markets, despite devaluation of the US dollar. One of the most striking examples is the trade deficit changes during the Clinton presidency. NAFTA passed in 1994, and made no immediate effect on our trade deficit.The trade deficit was -$79 billion in 1994, -$71 billion in 1995, and -$79 billion in 1996. In 1997, however, the trade deficit began to take off. It was -$104 billion in 1997, -$203 billion in 1998, and almost -$300 billion in 1999. By 2000, it was -$380 billion. The 2001 recession-induced contraction slowed the growth of the trade deficit. It "only" increased to -$399 billion in 2001. But the trade deficit growth re-accelerated after that, thanks to the injection of money into the economy by Fed chief Greedspan, in his efforts to drive down interest rates. By 2002, it had expanded to -$471 billion, followed by -$519 billion in 2003, and -$594 billion in 2004. Paralleling the trade deficit increases were policies that caused monetary expansion. In 1997, government policy was implemented to increase home ownership through a number of changes. As a result, in 1997, home sales began to skyrocket. The increased demand also caused home prices to skyrocket. Prior to 1997, there had been a linear relationship between home prices, and income+inflation. Beginning in 1997, however, this relationship disappeared, with home prices rising much faster than the sum of income+inflation. This facilitated the borrowing of more money to buy homes, which inflated their prices still further. The increased borrowing increased the effective money supply, as loans create money (at least on bank ledgers). As the value of homes increased, so did their assessed equity. As home equity increased, so did the equity available to borrow from. This allowed consumers to borrow more, spend more, increase product demand, and drive consumer goods prices up as a result. Thus, consumers drove prices up, due to the increased purchasing ability from increased borrowing ability. In fact, American consumers drove prices up more than dollar devaluation suppressed them in foreign markets. The end result was that American goods became more expensive in foreign markets. Price inflation on American exports increased more than the increase in purchasing power of foreign currencies (that resulted from dollar devaluation). The price-inflating effect would be even larger in countries who peg their currency to the dollar, such as China, since dollar devaluation has 0 effect on American export prices in China. Thus, the only thing affecting American export prices to China is US price inflation. Thus, dollar devaluation has absolutely 0 effect on the -$230 billion trade deficit with China. And since the Arab oil exporting country trade balance is mainly from oil imports, and is denominated in dollars, dollar devaluation's effect could only worsen our trade deficit with them. The limited effect of dollar devaluation on the U.S. trade deficit is important, because it pales in comparison to the effect of American domestic price inflation. Recent history indicates that US monetary expansion will worsen the trade deficit. Though it devalues the dollar—which puts downward pressure on export prices—it also causes domestic price inflation. Domestic price inflation has had a much greater effect, and more than cancelled out the effect of dollar devaluation. Since 80-90% of American production is sold to American consumers, 80-90% of demand comes from American consumers, and 80-90% of demand-induced price pressure comes from Americans. Monetary expansion increases American consumer spending power—causing 80-90% of price pressure to be upward (i.e., increasing the price). Though monetary expansion devalues the dollar, and puts downward pressure on American goods priced in foreign currencies, this accounts for only 10-20% of the price pressure. American price inflation has over 4-fold greater effect on American export prices, than does devaluation of the dollar. As a result, American domestic price inflation has over a 4-fold greater effect on our trade deficit than dollar devaluation. Monetary expansion is a tried-and-proven way to worsen the trade deficit, and cause even more American jobs to be lost to foreign competition. |

|

|

|

Post by unlawflcombatnt on Feb 10, 2008 2:43:07 GMT -6

Below are several graphs showing the connection between the increase in the trade deficit, and the non-trend increases in both Los Angeles home prices and the M3 money supply. Note that the most striking deviations from the previous trend occure in 1997, in all 3 graphs. TRADE DEFICIT:  www.citizenstrade.org/images/fast-track-trade-balance.jpgM3 MONEY SUPPLY www.citizenstrade.org/images/fast-track-trade-balance.jpgM3 MONEY SUPPLY:  HOME PRICES--LOS ANGELES HOME PRICES--LOS ANGELES As an aside, it's also interesting to notice how the Consumer Price Index began increasing at a slower rate than the M3 money supply, starting in 1997. |

|

|

|

Post by unlawflcombatnt on Mar 9, 2008 18:17:22 GMT -6

Below are graphics of both Current Dollar GDP and Current Dollar Trade Balance.  The above statistics can be found at the Bureau of Economic Analysis (BEA) . www.bea.gov/bea/dn/nipaweb/TableView.asp?SelectedTable=5&FirstYear=2005&LastYear=2007&Freq=QtrBelow is a modified copy of the Trade Balance from the " International Accounts" section at the BEA site.  Several more points can be drawn from the tables above. Our trade deficit shrinks with recessions and economic slowdowns. The fall of the Iron Curtain, and the "flooding of the labor market" with workers from Eastern block nations did not worsen our trade deficit. Our trade deficit peaked at 3.1% of our GDP in 1987 (under Reagan). It began falling in 1988, reaching a low of -0.5% in 1992. It had almost tripled as a % of our GDP by 1994 (under Clinton), but remained at that level through 1997. In 1997 it began to take off. NAFTA passed in November of 1993, and appears to have had little immediate effect on the trade deficit. PNTR with China didn't pass until late 2000. US entry into the WTO occurred in late 1994. Again, the trade deficit remained in the -1.2 to -1.3% range through 1997. From 1998 through 2000, however, the trade deficit exploded. It nearly quadrupled from -$101 billion in 1997 (1.2% of GDP) to -$379 billion in 2000 (3.9% of GDP). Again, the only event that parallels this is the beginning of the housing bubble, and the rapid increase in home prices. At some point (or points) during this period, Greedspan dropped interest rates to stave off a stock market decline--to make sure no rich investors became less rich. In 1997, tax laws were changed to encourage homeownership. |

|

|

|

Post by unlawflcombatnt on Apr 12, 2008 20:02:12 GMT -6

A worsening trade deficit in combination with a declining dollar is a true conundrum for many analysts.

I've read a number of papers attempting to explain this paradox, but none provide plausible explanations.

The problem in understanding this conundrum, however, stems from the starting point being used. Analysts start with currency devaluation, then try to explain why it doesn't have the predicted effect on trade balance. This is the wrong place to start.

It is the export prices themselves that mediate the effects on trade, not the currency devaluation itself. If prices rise, it reduces the quantity demanded. If export prices rise, it reduces the quantity of exports demanded. The 1st consideration, therefore, should be whether prices actually decline or not. This is an important distinction.

If the export price does not change as predicted, then other factors need to be considered. If export prices go in the opposite direction of what's predicted, then other factors are probably at work.

Export prices are determined largely by 2 factors.

1) The good's price in American dollars.

2) Foreign currency exchange rate with US dollars. ($ devaluation.)

Export prices are then affected as follows:

1)An increased US $ price increases the Export price.

2)Decreased $ valuation decreases the exchange-rate Export price in the foreign currency.

X) The net affect of these 2 factors is the major determinant of export prices of US goods. (The effects of tariffs & VAT manipulations are excluded for the sake of discussion.)

An increased US $ price is roughly the equivalent of consumer price inflation.

If US price inflation exceeds US dollar devaluation, export prices will rise (or at least there will be upward pressure on prices).

But if dollar devaluation exceeds US price inflation, export prices decline (or at least there will be downward pressure on prices).

Again, export price increases have the following effects:

If export prices increase, the quantity demanded declines.

If each export item sold has a given US$ value to its exporter, then the decreased quantity sold also reduces the total $ amount of sales.

Thus, if US price inflation is more than dollar devaluation, it reduces the $ value of exports.

Dollar devaluation must be more than US price inflation, in order to reduce exports.

It is the US price Inflation - to - $ devaluation ratio that counts, not just $-devaluation.

There are certainly other factors. The effect of US price inflation, however, is the major missing link in the trade-deficit/dollar-devaluation conundrum.

|

|

|

|

Post by unlawflcombatnt on May 8, 2008 18:55:23 GMT -6

It has long been thought that US dollar devaluation would reduce the US trade deficit. Statistics from the last 5 years, however, contradict that assertion. While the dollar has devalued in most currencies, the US trade deficit has not declined. In fact, it has increased significantly with almost all of our major trading partners. Over the last 5 years, our trade deficit has worsened with 5 of our 6 biggest trading partners, despite dollar devaluation (the Mexican Peso is the only currency the dollar has strengthened in.) Only with the United Kingdom has our trade deficit declined in tandem with dollar devaluation. Our trade deficit has worsened, however, with the European Union, Japan, China, Canada, and Mexico. With the exception of Mexico, the US $ decline has been in double digits. Below is a composite graph showing the US trade deficit (in goods) with all 6 countries in both 2003 and 2007. The bottom half of the chart shows the relative change in value of the 6 currencies over the last 5 years.  Not surprisingly, our trade deficit has expanded the most with China, increasing by 107%, despite an -18% decline in the value of the dollar. Despite the -40% decline in the value of the dollar in Euros & Canadian currency, our trade deficits increased by 14% and 18% respectively. With Japan, our trade deficit expanded by 25%, despite the dollar declining -14% in relationship to the Yen. With Mexico, our trade deficit worsened by a whopping 83%, despite the Peso falling only -3% against the US $. |

|

|

|

Post by unlawflcombatnt on May 21, 2008 21:04:53 GMT -6

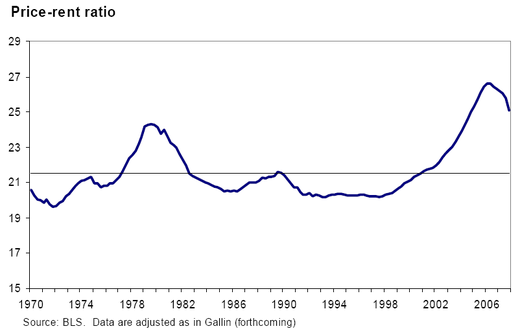

Below is another graphic of the Housing Bubble, showing the home price-to-rent ratio.  Once again, this graphic shows that the up-shoot started in 1997-98. Unlike some of the graphs above, this one shows the beginning of a price decline starting in 2006. It's interesting to note that our trade deficit also declined slightly since the end of 2006, somewhat paralleling the decline in home price-to-rent ratio. |

|

|

|

Post by unlawflcombatnt on Jun 4, 2008 21:28:11 GMT -6

It might be helpful to see some of the graphs in the same post, to see how it all fits together. The top one comes from Bonddad.  It seems like the rising dollar might have worsened the trade deficit, up through 2001. But it doesn't appear that a falling dollar reduced our trade deficit any after 2001. In fact, the trade deficit has worsened as the dollar has fallen since 2001. It does appear that the trade deficit worsening has paralleled a rise in the M3 money supply. (It also looks like the government has been fudging the CPI calculation since about 1997, as the money supply increase has diverged from the CPI increase. Once again, it looks like the sharp up-shoot in housing prices, the trade deficit, and the M3 money supply, began around 1997. It's impossible not to surmise that there is some connection. If CPI-measured inflation began to be understated in 1997, as has been suggested by many, then true CPI-measured inflation should have risen at a rate approaching that of the M3 money supply. If CPI had measured the true rate of inflation, then the trade deficit, home prices, M3, and CPI would have accelerated at the same time. And dollar appreciation would have matched the other 4 measures, from 1997 through 2001. After that, dollar devaluation went in the opposite direction. It still appears as though US price inflation and monetary expansion has greatly added to our trade deficit. And it appears much of this price inflation & monetary expansion paralleled the up-shoot in home prices, beginning in 1997. It seems reasonable to conclude that the policies that created the housing bubble (easy credit and tax changes that encouraged home purchases and speculation), also were major contributors to our trade deficit. It may also be that Bush's reverse Robin Hood tax cuts caused enough additional inflation to offset the effect the dollar's decline that began in 2002. |

|

|

|

Post by unlawflcombatnt on Jul 1, 2008 19:07:30 GMT -6

Here's another graph on oil prices that follows exactly the same pattern as housing prices, the trade deficit, and M3 money supply.  Once again, it appears that monetary expansion & consumer price inflation, which usually accompany dollar devaluation, are not having the predicted effect of decreasing the trade deficit. In fact, the exact opposite has occurred since 1997. Though the dollar has devalued in relation to foreign currencies, the trade deficit has still worsened. Again, it appears that consumer price inflation in the US overwhelms the benefits of a falling dollar, making the trade deficit even worse. It appears that US domestic price inflation offsets any price declines that would have occurred in foreign currencies from dollar devaluation. Undoubtedly, VATs and unfair trade practices are also contributing to the paradoxical increase in the US trade deficit. |

|

|

|

Post by agito on Jul 2, 2008 0:43:26 GMT -6

hey UnLC, i was just thinking about the number of currencies that are pegging their dollar to ours, and the effect that has as well.

For instance, if we are suffering 8%inflation, but that should give us an %8 export advantage, but another country, by virtue of tieing their currency to ours, is now suffering 12% inflation (giving them a 12% advantage)... anyway to isolate trade numbers with just countries that have fixed currencies versus others that don't?

|

|

|

|

Post by unlawflcombatnt on Jul 3, 2008 3:16:16 GMT -6

hey UnLC, i was just thinking about the number of currencies that are pegging their dollar to ours, and the effect that has as well. That's an excellent point about pegging to the dollar. And since China pegs to the US dollar, we have to eliminate them from the picture, when it comes to associating dollar devaluation to trade deficit. It is only with the Eurozone, Britain, Canada, and Mexico, that we can even try to make a connection. But with those 4 countries/areas, our trade deficit has increased while our dollar was devaluing. Yes, I think that can be done. We can look at the individual countries/zones, compare dollar devaluation in those specific currencies, and get an idea of how dollar devaluation compares with the change in our trade deficit. As I mention above, the trade deficit has increased with all of them, despite export-favoring dollar devaluation. Below is a copy of the 4 year change in dollar valuation with 6 other currencies. There was a 40% decline in the value of the dollar versus the Euro, which should have  'd our trade deficit by an equivalent amount. Instead, our trade deficit  'd by 14%. Despite a 15%  in the US Dollar versus the Yen, which should have 'd America's trade deficit with Japan, our trade deficit 'd 25%. There was also a 40% in dollar against the Canadian dollar, which should have 'd our trade deficit with Canada. But the trade deficit with Canada still 'd 25%. The US$ has actually slightly against the Mexican Peso (~ +5-10%), which would be expected to slightly our trade deficit with Mexico. But there was nothing "slight" about it. Our trade deficit with Mexico increased a whopping 83% over that time. Our trade deficit with Mexico, however, has additional contributory factors. Unlike Japan, Europe, and Canada, whose workers are paid wages similar to American wages, Mexican labor is much, much cheaper than US labor. Thus, the biggest part of our Mexican trade deficit is due to cheap labor, not US inflation or dollar valuation. I want to go back to this comment: This comment actually highlights my main focus. If the US is suffering 8% inflation, it means that it raises American consumer prices. Thus, in and of itself, inflation would also the price of American exports in foreign markets as well, since the biggest determinant of prices for American-produced goods is American demand. Since Americans purchase 80-90% of their own goods, their demand is 80-90% of the price determinant. Foreign consumers must compete with American consumers for American-produced goods. Thus, they must usually pay the same exchange-rate price as Americans. (There are exceptions. Some prices are set lower in foreign markets, such as pharmaceuticals. But again, these are the exceptions, not the rule.) Increased American inflation alone will worsen our trade deficit. On average, American demand is 80-90% of the price determinant of those goods, even when sold in foreign markets. But American consumer price inflation does not occur in a vacuum. It usually occurs along with dollar devaluation. So again, the issue becomes whether dollar devaluation offsets American consumer price inflation. For example, if American consumer prices went up 30%, but the dollar devalued by only 20%, the net effect would be an in export prices — proportional to a +10% price increase. Thus, the overall effect would still be to increase our trade deficit. The point here is that US price inflation has a significant effect on our trade deficit. This effect may explain part of the "conundrum" of an 'ing trade deficit, despite a 'ing dollar. Cheap foreign labor and pegged currencies also worsen our trade deficit. All that being said, the only solution to our trade deficit is tariffs. We cannot control what other countries do to their currency, or how they treat their workers. We cannot control whether they subsidize their exports — either directly, or thru VATs. But we can control what comes in to this country. And we can make foreign goods more expensive. And we can make it unprofitable for American companies to move production overseas, fire their American workers, and replace them with cheaper foreign workers. And we can do all of this with tariffs. Is this "protectionism"? You bet your sweet bippy it is. "Protection" is exactly what a government is supposed to provide its citizens. It's why we have a government to begin with. And this protection includes all citizens, not just the richest ones. |

|

|

|

Post by unlawflcombatnt on Nov 29, 2008 13:23:12 GMT -6

I've finally found another source that attempts to calculate the number of jobs lost per $$ of trade deficit. The graphic below puts the number of jobs lost at -20,000 jobs = -$1 billion of Trade Deficit(The above was for 2006, so one would assume that with inflation, the job losses per $$ of Trade deficit would be somewhat lower today.) More recent statistics on the trade deficit with China — from the Economic Policy Institute (Table 1, page 3) — put the job losses $ of Trade deficit somewhat lower--at approximately 1 job/$77,560 of trade deficit (i.e., -1 job = -$77,560), or -12,893 jobs = -$1 billion of Trade Deficit This number was calculated from the change in the 2001-2007 Trade Deficit with China of -$178 billion, divided by the assumed China trade related job losses of -2.295 million. $178,000,000,000 ÷ 2,295,000 jobs = $77,560/job

$1,000,000,000 ÷ $77,560/job = 12,893 jobs/$1 billion of Trade DeficitOur 2007 Trade Deficit was -$711 billion. Our 2007 Oil "Deficit" was -237 billion. -$711 billion - (-$237 billion) = -$474 billion. -$474 billion ÷ 12,893 jobs/$1 billion = -6.1 million jobs From these numbers, the non-oil trade deficit has cost Americans -6.1 million jobs |

|

|

|

Post by fredorbob on Dec 18, 2009 5:16:29 GMT -6

What actually does affect the traded deficit, however, is US monetary policy and monetary expansion. From long-term macro statistics, US monetary expansion DOES seem to increase the trade deficit. (Even if not causative, monetary expansion is almost always paralleled by an increase in the trade deficit.) This pattern can be seen when reviewing the last 30 years of US macro statistics, especially GDP, trade balance, and price inflation. The trade deficit increased when government or Fed policy caused expansion of the monetary supply—either by Fed injection of money to manipulate interest rates, or by government expansion of the money supply from policy to increase borrowing and loans—as every new loan increases the virtual money supply. (The most important of these policies was that of increasing home ownership.) Sounds like you're blaming the Federal Reserve and not free trade with cheap foreign labor countries.  When an American purchases a Chinese product, a Chinaman gets DOLLARS for the transaction. The US trade deficit is 700 billion dollars a year, that means 700 Billion DOLLARS literally leaves the country every year. We only have a trillion in currency, so if the federal reserve does not print more money then WE WOULD BE OUT OF DOLLARS IN 2 YEARS, we would have to BARTER or use FOREIGN CURRENCIES like the PESO or EURO. The Federal Reserve is tasked with maintaining the US paper money supply, that is ALL they are doing. If you get rid of the Federal Reserve, then Congress controlling the money supply would do the exact same thing, in addition to printing more money to run federal programs. It would be real inflation with Democrats controlling Congress. If you get rid of the Federal Reserve and went Full Ronulan and go on the gold standard, then Fort Knox would be drained in less then 6 months. We would be out of paper, out of gold, and we'd be using Euros and Pesos to barter with. It would be total anarchy; what is the IRS going to tax people with, Pesos? The trade deficit FORCES the Fed to print money, the Federal Reserve does not force the trade deficit. |

|

|

|

Post by fredorbob on Dec 18, 2009 5:21:30 GMT -6

yay double post

|

|

|

|

Post by fredorbob on Dec 18, 2009 5:29:37 GMT -6

NAFTA passed in November of 1993, and appears to have had little immediate effect on the trade deficit. PNTR with China didn't pass until late 2000. US entry into the WTO occurred in late 1994. Again, the trade deficit remained in the -1.2 to -1.3% range through 1997. It takes time to build a factory somewhere else, and to destroy jobs here, it won't be instantaneous but gradual. |

|

|

|

Post by fredorbob on Dec 18, 2009 5:55:32 GMT -6

The devalue dollar theory still holds, it's just that so many countries have pegged their currency to the dollar and/or actively devalue their currency and/or have politically unstable countries and/or cheap foreign labor still makes profits for the slavers: import-export.suite101.com/article.cfm/us_global_trade_debt_by_country____________________________________ Fastest Increasing Deficits Below are the nine countries that grew the American deficit the fastest last year. 1. Mexico … US $74 billion (up 15.4% from 2006, up 64.4% from 2004) The Peso is devaluing FASTER then the dollar is devaluing 2. Nigeria … $28.9 billion (up 12.5%, up 97.3%) The niara is all over the place, it's Nigeria what do you expect. The greed and drive to find the cheapest labor is pathetic. 3. France … $14.5 billion (up 12.5%, down 36.9%) Euro 4. China … $259.1 billion (up 11.4%, up 59.9%) pegs currency to Dollar so doesn't matter how devalued the dollar gets 5. Ireland … $21.6 billion (up 7.5%, up 12.5%) Euro 6. Italy … $20.9 billion (up 3.7%, 20.4%) Euro 7. South Korea … $13.6 billion (up 2.5%, down 31.5%) Either pegged to the dollar or vigorously devalued 8. Saudi Arabia … $24.5 billion (up 1.8%, up 57.3%) Saudi Riyal, like China is pegged on the dollar 9. Venezuela … $28.4 billion (up 0.6%, up 40.4%), The Venezuelan Bolivar is also pegged on the dollar, and it's got a raving socialist as dictator*Euro. The dollar is starting to climb against the Euro. Maybe investors are noticing how Europe is falling into Green-Communism, so faith in the Euro is falling_____________________ Fastest Decreasing Deficits Below are the six countries that shrunk the American deficit in 2007 when compared to prior year. 1. United Kingdom … $6.7 billion (down 16.8%, down 36%). 2. Taiwan … $12.7 billion (down 16.7%, down 1.9%) 3. Malaysia … $20.8 billion (down 13.2%, up 20.4%) 4. Canada … $65.0 billion (down 10.7%, down 1%) 5. Germany … $44.5 billion (down 6.9%, down 2.8%) 6. Japan … $83.1 billion (down 6.1%, up 10.5%), _______________________________ Top Ten Countries with which the U.S. has a Trade Surplus (in millions) www.census.gov/foreign-trade/top/dst/current/surplus.html Hong Kong 14,140.12 barely moving against US dollar Australia 9,420.76 Australian dollar getting stronger Netherlands 13,623.32 AnomolyUnited Arab Emirates 8,622.25 Shrugs Brazil 4,973.02 Quitting Singapore 5,131.52 Belgium 7,313.38 Greece 1,340.97 Panama 3,226.88 Turkey 399.99 2,753.04 ______________________________________ Tariffs need to be primarily based on trading partners not products. Countries not products, since it is countries practicing trade nationalism against the US, not companies within countries although no doubt they lobby their own leaders. |

|

|

|

Post by fredorbob on Dec 18, 2009 6:26:41 GMT -6

Despite a 15% in the US Dollar versus the Yen, which should have 'd America's trade deficit with Japan, our trade deficit 'd 25%. The trade deficit with Japan drastically dropped in 2008 which coincides with the weakening dollar against Japanese Yen on your graph in 2008. It didn't completely turn into a surplus because Japan protects their markets like any normal country with any sense of nationalism would do. |

|

|

|

Post by fredorbob on Dec 18, 2009 6:33:32 GMT -6

There was also a 40% in dollar against the Canadian dollar, which should have 'd our trade deficit with Canada. But the trade deficit with Canada still 'd 25%. Your graph looks like Canada unpegged their currency with the dollar in January 2005 (shrugs) www.census.gov/foreign-trade/balance/c1220.htmlThe US trade deficit with Canada has dropped since 2005, which mirrors what your graph shows that the value of the dollar started dropping against the Canadian dollar in mid 2005. |

|

|

|

Post by fredorbob on Dec 18, 2009 6:38:15 GMT -6

. . . All that being said, the only solution to our trade deficit is tariffs. We cannot control what other countries do to their currency, or how they treat their workers. We cannot control whether they subsidize their exports — either directly, or thru VATs. But we can control what comes in to this country. And we can make foreign goods more expensive. And we can make it unprofitable for American companies to move production overseas, fire their American workers, and replace them with cheaper foreign workers. . . . What's with all the negativity attached to tariffs: "We can make foreign goods more expensive"? The federal government is run on money, it's either going to tax American wages or tax foreigners. I'd think it'd be a tad bit better to tax foreigners, especially ones that practice trade nationalism against my country. The goal of taxation isn't to make things more expensive, it's to collect revenue. The IRS motto isn't, "To make life more miserable for Americans home and abroad," although it should be. |

|

|

|

Post by unlawflcombatnt on Dec 18, 2009 19:22:16 GMT -6

The federal government is run on money, it's either going to tax American wages or tax foreigners. I'd think it'd be a tad bit better to tax foreigners, especially ones that practice trade nationalism against my country. I completely agree. And so did our forefathers. One of the biggest sources of revenue had always been Tariffs. My earlier point was not that dollar devaluation had no effect. It was just that the effect had been overwhelmed by other factors, like cheap foreign labor, foreign protectionism, and US price inflation. |

|

|

|

Post by jeffolie on Dec 18, 2009 20:10:01 GMT -6

Exporting countries to America do not seem to care what the value of the Dollar is because they must keep their populations politically passive and employed.

A declining Dollar has not yet resulted in inflation from imported goods because the exporters are not rising their prices inorder to remain in control of the American consumers purchases.

Devalued Dollars continue to pile up in the coffers of exporting countries that accept them despite the Dollars long term gradual decline.

China recently said that it was not getting enough Dollars resulting in their difficulties in purchasing more Treasuries. This would make sense if Americans were buying less Chinese goods because of their need to be frugal and as Americans without jobs simply can not buy very much.

|

|

|

|

Post by fredorbob on Dec 21, 2009 10:21:09 GMT -6

If an audit on the Federal Reserve can get the Chariman of the Fed to admit on television that they had no choice to print 700 billion dollars last year because 700 billion dollars left the country last year so therefore all these economic woes originate from free trade, then heck i'm all for it.

Otherwise what exactly does Ron Paul expect to find from an audit? He won't find anything, how can he find something if he doesn't know what he's looking for. What exactly are the "audit the fed" people looking for anyways?

|

|

|

|

Post by unlawflcombatnt on Dec 21, 2009 12:33:06 GMT -6

What exactly are the "audit the fed" people looking for anyways? We need to know with more certainty how much money the Fed has given away both directly and indirectly (i.e., through overpayment to purchase toxic assets), and we need to know to whom these handouts went. I don't think anyone knows how much money has gone to Government Sachs, either by known documented transfer, or by secretive addition of 0's onto their account ledgers. In fact, there are a lot of other firms that have gotten funds from the Fed. Some foreign banks probably received US taxpayer money as well. And if this doesn't convince you, just look at how hard Bernanke is working to block any such audit. There appears to be a lot of financial chicanery that Uncle Ben and Terrible Timmy don't want the public to know about. |

|

|

|

Post by fredorbob on Dec 22, 2009 1:20:59 GMT -6

What exactly are the "audit the fed" people looking for anyways? We need to know with more certainty how much money the Fed has given away both directly and indirectly (i.e., through overpayment to purchase toxic assets), and we need to know to whom these handouts went. I don't think anyone knows how much money has gone to Government Sachs, either by known documented transfer, or by secretive addition of 0's onto their account ledgers. In fact, there are a lot of other firms that have gotten funds from the Fed. Some foreign banks probably received US taxpayer money as well. And if you this doesn't convince you, just look at how hard Bernanke is working to block any such audit. There appears to be a lot of financial chicanery that Uncle Ben and Terrible Timmy don't want the public to know about. 14 billion, isn't that what Goldman Sachs received? Hehe, check out this free traitor article, read it then look at the date it was published: www.realclearmarkets.com/articles/2008/03/cheap_labor_is_very_expensive.htmlThen if you don't get it, look at the comments. |

|

|

|

Post by agito on Dec 22, 2009 20:08:47 GMT -6

|

|

|

|

Post by fredorbob on Mar 27, 2010 5:53:34 GMT -6

|

|

|

|

Post by agito on Mar 27, 2010 12:44:49 GMT -6

yeah- i think they removed it. maybe they couldn't live with the comments being more informative than the articles they chose to link to.

|

|

|

|

Post by unlawflcombatnt on Mar 27, 2010 12:51:22 GMT -6

He sure is. He's spews the same pseudo-supply side babble that was barfed up when Clinton was pushing NAFTA. Tamny completely ignores the demand side of the equation--that there has to be a market for sales--which requires workers that earn enough to purchase goods. And he further implies, as many have, that the cheaper prices on foreign-produced goods will offset the wage loss of Americans--which is stupidity in the extreme. If price reductions on foreign produced goods completely offset the aggregate wage losses of Americans, then free-traitors would get no benefit from outsourcing. There'd be no increase in profits if they passed on 100% of their labor cost savings to American consumers. Obviously they're not doing that. And all of that "capital accumulation" obtained by cutting labor costs is not going to get invested in capital equipment or production, because the jobs lost to outsourcing reduce worker-consumer incomes--causing less spending power, less demand for production, and thus LESS demand for capital investment. No sustainable job growth has ever occurred without growth in demand for the goods that employed workers would produce. And with less aggregate income (from outsourcing-induced wage suppression and job loss), there will be job losses. Capital does not create jobs. Demand does. |

|

|

|

Post by StephensTabitha on Apr 13, 2010 18:25:05 GMT -6

I had a desire to make my organization, but I didn't earn enough amount of money to do that. Thank goodness my fellow proposed to utilize the <a href="http://lowest-rate-loans.com">loan</a>. So I received the college loan and realized my old dream.

|

|