Post by unlawflcombatnt on Dec 28, 2014 22:58:26 GMT -6

Multiple economists--including David Stockman, Michael Hudson, & Paul Craig Roberts--have commented on how the Fed's 0% interest rates have hurt savers, and essentially bailed out banks at taxpayers expense. Though it's not difficult to accept this notion, it was difficult (for me, at least) to see just how big this effect actually is.

The magnitude of the effect of the Fed's 0% interest rate is shocking, and justifies an explanation.

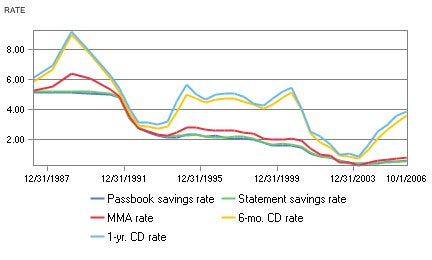

In previous decades, Americans made money off their savings accounts--and considerable amounts at that.

The so-called "magic" of compounded interest, almost comically referred to by George W Bush, is at the heart of the matter.

In the decades prior to the start of the 21st century, Americans put much of their savings in savings accounts.

Back then it earned interest that was compounded--often daily.

But even if compounded annually, the amount of interest earned, and it's addition back into the interest-bearing amount, could increase the total saving amount tremendously.

Many people knew this, but it's doubtful everyone knows how big a difference small interest rates can make.

And I wonder how many have connected the money that they, and other savers, have lost by the Fed's 0% interest rate policy.

I certainly wasn't aware of how much difference it made myself, until a recent '60 Minutes' special on a parallel issue--how much management fees subtract from your ultimate nest egg.

In the 60 Minutes episode it was stated if a person was receiving a 7% return on their investment, and 2% of it went to fees, it would reduce the amount earned over 50 years by a whopping 63%.

In other words, the saver's amount would be only 37% of what it otherwise would have been, had not the 2% management fee been deducted.

That seemed very hard to believe initially.

And then I worked the numbers--over 50 years.

The ultimate amount on an annually compounded 7% interest, would be the initial amount x 1.07 x 1.07 x 1.07.... or 1.0750

[There are compound interest calculators that can be used for this.] www.mathwarehouse.com/calculators/online-compound-interest-calculator.php

The initial amount subjected to 7% interest compounded annually increases 29-fold over 50 years.

Subtracting 2% (for fees, as shown on 60 Minutes), and calculating by 1.0550, gives an 11-fold over 50 years.

Just that 2% decrease subtracts -62% from the total.

If the original amount had been $50,000, at 7% it would have grown to $1,450,00.

But if the original amount was $50,000, at 5% it would have been only $550,000 -- $900K less.

But this example is just the tip of a huge iceberg.

The real problem is that Americans are getting NO compounded interest on Savings accounts, Banking accounts, or anything else.

Making money from compounded interest on anything is now a thing of the past.

Whereas in previous decades Americans might earn 5-6% interest (often compounded daily).

But this is a thing of the past. Savings accounts no earn only fractions of a per cent.

What's really happened here is that, in effect, American savers previously loaned their money to banks--and were paid interest on it. Americans essentially loaned their savings to banks.

American's savings and bank accounts were THE source of funds for bank loans--or at least for the required reserve amounts. Banks borrowed the money from savers, and in turn used it as the collateral to lend out to borrowers.

How much Americans put in their bank & savings accounts limited how much banks could loan out.

But things have changed. Now banks don't need savers' money. They have the Fed. And they have the money they were paid by all the various bailout plans concocted since 2008.

And their reserve/capital requirements have been reduced to almost 0, so they have even less need for savers' money.

And the interest rates reflect this.

Many pension & retirement plans relied on this same policy of compounded interest.

But now the only compounded interest in existence is that which banks charge consumers. The financial industry is now the sole recipient of compounded interest.

The Fed & Treasury have essentially stolen Americans' previous compounded interest income, and handed over to banks.

As the numbers above indicate, this is no small amount.

For example,

If 100 million Americans with $30,000 in savings got 5.5% annually compounded interest per year over the last 20 years,

each would have seen that $30K grow to $87K, for a +$57K increase apiece.

The aggregate amount of earnings by those 100 million people is 100,000,000 x $57,000 = $5.7 Trillion.

And $5.7 trillion would be the amount of money LOST by that same 100 million Americans by getting the ~0% interest they now get.

Though these aren't exact numbers, they do give a ballpark idea of the difference the Fed's Qunatitative Easing & 0% interest rates have made on consumer finances.

The Fed & the Treasury Dept have essentially stolen Trillions of $$$ in compounded interest from consumers--and given it to banks, financiers, & Wall Street (the latter because Americans have been forced to put their money in the stock market to earn any money at all.)

The magnitude of the effect of the Fed's 0% interest rate is shocking, and justifies an explanation.

In previous decades, Americans made money off their savings accounts--and considerable amounts at that.

The so-called "magic" of compounded interest, almost comically referred to by George W Bush, is at the heart of the matter.

In the decades prior to the start of the 21st century, Americans put much of their savings in savings accounts.

Back then it earned interest that was compounded--often daily.

But even if compounded annually, the amount of interest earned, and it's addition back into the interest-bearing amount, could increase the total saving amount tremendously.

Many people knew this, but it's doubtful everyone knows how big a difference small interest rates can make.

And I wonder how many have connected the money that they, and other savers, have lost by the Fed's 0% interest rate policy.

I certainly wasn't aware of how much difference it made myself, until a recent '60 Minutes' special on a parallel issue--how much management fees subtract from your ultimate nest egg.

In the 60 Minutes episode it was stated if a person was receiving a 7% return on their investment, and 2% of it went to fees, it would reduce the amount earned over 50 years by a whopping 63%.

In other words, the saver's amount would be only 37% of what it otherwise would have been, had not the 2% management fee been deducted.

That seemed very hard to believe initially.

And then I worked the numbers--over 50 years.

The ultimate amount on an annually compounded 7% interest, would be the initial amount x 1.07 x 1.07 x 1.07.... or 1.0750

[There are compound interest calculators that can be used for this.] www.mathwarehouse.com/calculators/online-compound-interest-calculator.php

The initial amount subjected to 7% interest compounded annually increases 29-fold over 50 years.

Subtracting 2% (for fees, as shown on 60 Minutes), and calculating by 1.0550, gives an 11-fold over 50 years.

Just that 2% decrease subtracts -62% from the total.

If the original amount had been $50,000, at 7% it would have grown to $1,450,00.

But if the original amount was $50,000, at 5% it would have been only $550,000 -- $900K less.

But this example is just the tip of a huge iceberg.

The real problem is that Americans are getting NO compounded interest on Savings accounts, Banking accounts, or anything else.

Making money from compounded interest on anything is now a thing of the past.

Whereas in previous decades Americans might earn 5-6% interest (often compounded daily).

But this is a thing of the past. Savings accounts no earn only fractions of a per cent.

What's really happened here is that, in effect, American savers previously loaned their money to banks--and were paid interest on it. Americans essentially loaned their savings to banks.

American's savings and bank accounts were THE source of funds for bank loans--or at least for the required reserve amounts. Banks borrowed the money from savers, and in turn used it as the collateral to lend out to borrowers.

How much Americans put in their bank & savings accounts limited how much banks could loan out.

But things have changed. Now banks don't need savers' money. They have the Fed. And they have the money they were paid by all the various bailout plans concocted since 2008.

And their reserve/capital requirements have been reduced to almost 0, so they have even less need for savers' money.

And the interest rates reflect this.

Many pension & retirement plans relied on this same policy of compounded interest.

But now the only compounded interest in existence is that which banks charge consumers. The financial industry is now the sole recipient of compounded interest.

The Fed & Treasury have essentially stolen Americans' previous compounded interest income, and handed over to banks.

As the numbers above indicate, this is no small amount.

For example,

If 100 million Americans with $30,000 in savings got 5.5% annually compounded interest per year over the last 20 years,

each would have seen that $30K grow to $87K, for a +$57K increase apiece.

The aggregate amount of earnings by those 100 million people is 100,000,000 x $57,000 = $5.7 Trillion.

And $5.7 trillion would be the amount of money LOST by that same 100 million Americans by getting the ~0% interest they now get.

Though these aren't exact numbers, they do give a ballpark idea of the difference the Fed's Qunatitative Easing & 0% interest rates have made on consumer finances.

The Fed & the Treasury Dept have essentially stolen Trillions of $$$ in compounded interest from consumers--and given it to banks, financiers, & Wall Street (the latter because Americans have been forced to put their money in the stock market to earn any money at all.)